By Bjoern Maul and Bruce Spear

This article first appeared in Forbes on October 30, 2018.

More than a year ago, the European airline sector began to see early signs of impending turbulence. First, it was the bankruptcies of Air Berlin, Alitalia, and Monarch. Then, this year in quick succession, SkyWork, VLM, Cobalt Air, Small Planet Airlines Germany, and Primera Air went out of business. Most recently, Ryanair CEO Michael O’Leary — echoing the sentiment of a growing number of experts — predicted “more and larger failures this winter” because of rising fuel prices and wages.

While the situation is nowhere near the crisis that enveloped carriers in the United States a decade ago when they underwent a major consolidation, the option to consolidate for European airlines today has become not only necessary but also inevitable. Facing rising operating costs and labor shortages for pilots and mechanics, European carriers — including some of the larger ones — find themselves unable to generate sufficient profitability to invest, innovate, and grow at a rate that keeps pace with international rivals.

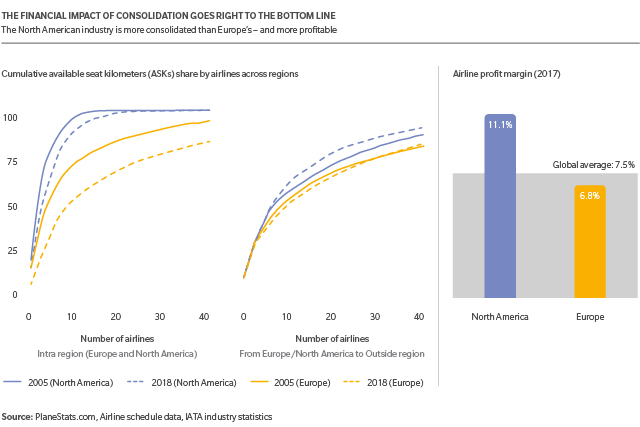

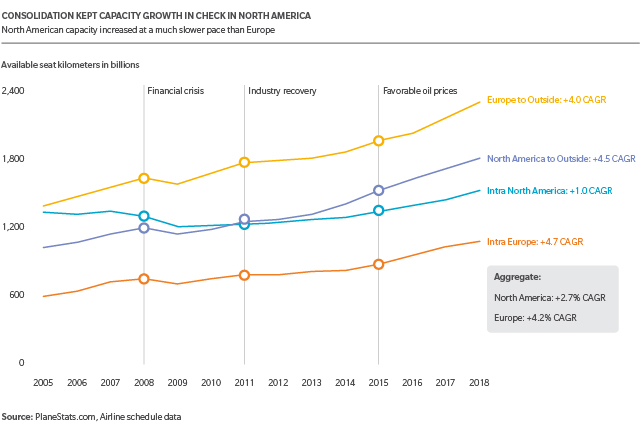

Compared to North American airlines today, the European aviation sector is more fragmented and less profitable and shows insufficient capacity discipline. Carriers that have been attempting to consolidate the market are still unable to match the scale that the biggest U.S. airlines have achieved. Today, the top five intra-North American carriers command a 77% market share versus a 51% market share for the top five intra-European airlines. That difference, plus stricter capacity discipline, explain why the U.S. industry has enjoyed stronger profitability than Europe.

To read the entire article, please click here.