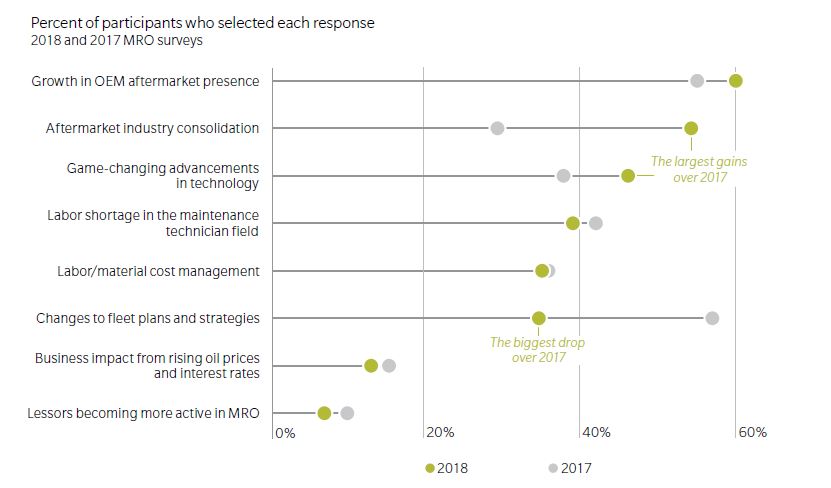

While last year’s survey participants were equally preoccupied by the rapid expansion of the global airline fleet, this year OEMs were respondents’ number one disruptor (60%), followed closely by aftermarket industry consolidation (55%) – which in part is a result of heightened competition from OEMs. That category moved up 26 percentage points from last year – the most of any. Another category on the move is the impact of game-changing technology – up nine percentage points; fleet expansion dropped 22 percentage points to sixth place.

Survey respondents also revealed more apprehension about the control some OEMs – particularly engine and component manufacturers – are exerting over intellectual property (IP) and the expectation that OEMs will leverage it to gain more market share. The marketplace is experiencing a rise in material costs connected in part to IP-ownership concentration, and survey respondents anticipate seeing even higher prices and more IP-propelled OEM market expansion in the near future. Seventy-eight percent of respondents expect OEMs to become the most dominant players in the MRO industry over the next three years, and they also are convinced aircraft manufacturers will meet or approach their aggressive growth targets for aftermarket revenue within the next decade.

Managing materials and labor costs in the face of tightening supply also persists as a challenge for all players. As last year’s survey revealed, respondents believe the labor shortage among mechanics poses a serious risk to the industry and serves as the primary driver of labor cost pressures – twice as significant as any other factor. The retirement of maintenance technicians and a dearth of newly created ones to take their place are squeezing both ends of the workforce spectrum across the globe.

CYBER THREAT GROWS

Following several high-profile cyberattacks against large transportation and logistics companies, Oliver Wyman questioned industry players about their readiness to fend off hackers. In our MRO Cybersecurity Special Report, we review survey findings that suggest a certain level of complacency, with many respondents unaware of efforts and investments by their companies in cybersecurity. The risk of breaches is real – as we’ve witnessed for more than a decade in industries from banking, to healthcare, to retail – and the threat is growing for the MRO industry as it strives to digitize. On March 15, the Department of Homeland Security sent out an alert that revealed Russian hackers have been conducting systematic attacks since 2016 on the US electric grid and various infrastructure industries, including aviation, for the purpose of collecting data on network design and control systems.

Any breach in global, interconnected industries like transportation and MRO can spread worldwide in a matter of hours. For this reason, it is imperative for the MRO industry as a whole to work together to strengthen its cybersecurity and risk management practices around digital operations. With the DHS announcement, cyberattacks on aviation have moved from a possibility to a reality.

Live From MRO Americas 2018

Oliver Wyman Partner Brian Prentice presents the Annual Industry Analysis and Forecast.

Live from MRO Europe 2018

ABOUT THE SURVEY

In its second decade, the Oliver Wyman annual MRO survey is an industry standard that samples the attitudes and strategies of executives from across aviation as they address key trends and emerging issues in the maintenance, repair, and overhaul (MRO) sector. Nearly 100 aviation professionals responded to the 2018 survey, with a mix across airline operators, captive airline MROs, independent MROs, and original equipment manufacturers (OEMs). Representatives from leasing organizations, financiers, parts distributors, and advisors rounded out the ecosystem of respondents. This year, 52 percent of respondents to the annual survey were senior executives – either in C-suite posts, vice presidents, or above; 78 percent were director level or above. The sample reflects views across major geographic markets, with North America representing 57 percent of inputs, Europe 25 percent, and Asia 11 percent. The balance came from Latin America, the Middle East, and Africa.

Authors