Three trends are impacting the global energy sector at an unprecedented pace: decarbonization, digitization, and decentralization.

Energy policy and regulations have to adopt quickly to respond to these technology-driven trends that are enabling empowered energy consumers and transforming demand and supply.

Get the policy framework right and distributed generation offers new opportunities for countries to provide secure, affordable, and environmentally sustainable energy. Policy frameworks that do not integrate distributed energy resources will face investment challenges and may slip down the Energy Trilemma Index.

The World Energy Trilemma 2017: ‘Changing dynamics - Using distributed energy resources to meet the Trilemma challenge’, tapped into the global insights of leaders across the evolving energy sector. Through interviews and surveys with utilities, transmission companies, energy entrepreneurs, storage providers, and e-vehicle developers, we identified three key focus areas for policymakers and industry leaders to balance the energy trilemma and meet evolving consumer demands.

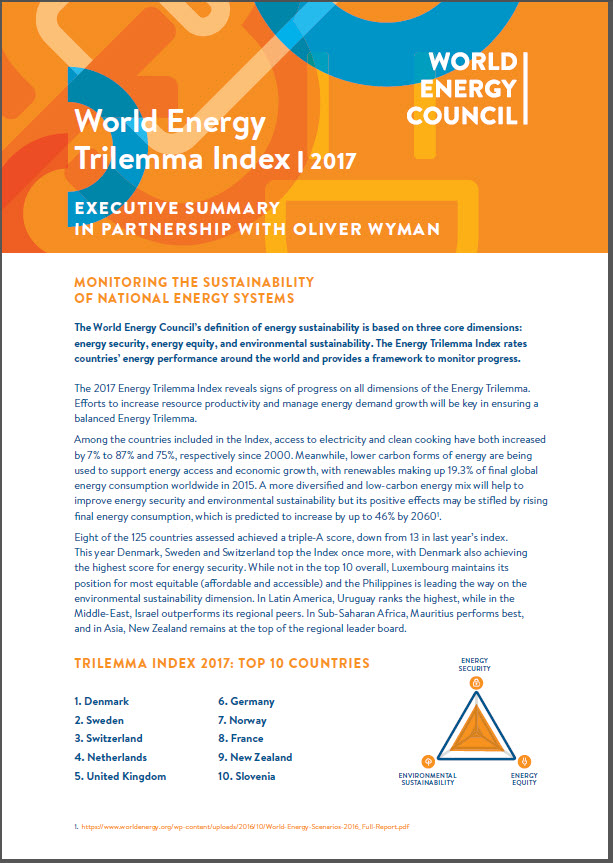

The annual Energy Trilemma Index ranks country energy performance in providing secure, affordable, and environmentally sustainable energy. Explore the Index to identify the top overall performing countries, individual country profiles and regional overviews.

Voices From The Energy Sector

next ›

Featured Interview: Alison Andrew, CEO, Transmission Company

“Our role could evolve from providing 24/7 reliability and real-time balancing to providing a resilient battery-charging service.”

Consumers have new options for making, storing, and controlling electricity, and their impact on the energy outlook is a challenging factor to accommodate. For example, by the 2020s, we expect there will be more battery storage in the system. Looking beyond that, we are asking questions around how energy will be used, such as will people still demand electricity as they do now, in what form, and what role will the grid play, etc.?

Looking forward, we expect to see more behind-the-meter technology such as interconnected appliances, behind the grid storage and consumers using batteries for their e-vehicles. Taken as a whole, this creates challenges such as managing seven-way power flows and growing cybersecurity concerns. As distributed storage becomes extensive, our role could evolve from providing 24/7 reliability and real-time balancing to providing a resilient battery-charging service.

It is an exciting future and some form of interconnection is key to providing reliable energy. Policy regulation will have to adapt, and be prepared to change fast. Often regulation is developed after a technological or market shift, however it is important for regulators to keep up-to-date with how the market is progressing.

next ›

Featured Interview: Leo Birnbaum, Chief Operating Officer - Networks & Renewables, Utility

“The future energy system will be much more influenced by customers than in the past.”

The largest consumers - companies - are creating long term climate plans for the future and they will not care what the market is like since they will do whatever it takes to achieve these commitments. Therefore we could see investment based on long-term arrangements on the customer side, meaning that market design just becomes an optimisation signal for whatever asset base they have built around the customer business.

The key players that can take responsibility for system stability are the TSOs and Distributed System Operators (DSOs), and in a complex world with lots of prosumers it should primarily be the DSOs. If you decentralise everything, then you have local actors so this should be the area to optimise first. Also sector coupling can only really be done on a local level. This can't be done with a central, master plan.

We actually might get into a world where the wholesale market is only a dispatch signal, and actually somehow we get the investment signals by other means, such as large customer groups.

next ›

Featured Interview: Norbert Nusterer, President, Power Systems Business, Cummins

“The model will change quickly as a growing number of stakeholders influence the regulatory framework.”

The technology mix of generation with storage will be quite disruptive. Storage, along with the growth of distributed generation and prosumers, are creating new opportunities to deploy assets as balancing forces in the grid. The more volatile the standard grid becomes, the more economic opportunity to be the balancing force in that.

The intensity and speed of the growth of prosumers depends heavily on the regulatory framework and who is allowed to be an active player in the market. Currently, due to regulation, there is considerable under-utilization of assets and the model will change quickly as a growing number of stakeholders influence the regulatory framework. There are also a lot of details to determine. For example, utilizing evehicles as grid assets, (e.g., peak shaving.) The technology exists but there are many issues to address, such as how to bill for this use, how to account for it, and how to set the market price for the power drawn out of the battery?

next ›

Featured Interview: Marty Sedler, Director of Global Utilities and Infrastructure, Intel

“Regulatory structure and utilities are simply not evolving fast enough or prudent enough to meet the needs of the changing power system.”

Managing operating costs and potential cost volatility, while maintaining reliability and quality of supply, is crucial in our highly competitive industry. A greater use of renewable power is part of that process for us, along with a focus on energy efficiency, and it is one of the reasons that we have become the largest voluntary corporate purchaser of green power in the U.S (per the EPA Green Power Program rankings).

When selecting or growing sites, we consider the future development of the energy supplier and grid, with a consideration of how they align to our strategy, including cost and sustainability goals. In many locations, regulatory structures and utilities are simply not evolving fast enough to meet our needs. This includes potential use of on-site greener generation and use of renewable energy as rather than just the grid, VPPA or PPAs. All options are part of a portfolio to optimize supply solutions in the future.

Evolving the energy system to meet the constant changing needs for all stakeholders is certainly challenging, but policymakers can focus on a few areas to help the process. First, we need greater consistency in regulation and rules around distributive generation and renewable energy at a country, regional and state level. Currently, we are faced with wide variations in processes, standards and rules even between states in the USA, complicating efficient supply management. Second, the grid and power generation need to be updated and become smarter, allowing the whole system to become more efficient and reliable. Technology advancements in making data available with analysis, needs to be implemented to secure the cost and reliability of the grid. The fast growing implementation of distributed generation, much of it renewable and intermittent, makes better data management and controls essential to effectively operate the power systems.

Policymakers can step in to help drive progress on that front by bringing all parties to the table to create a roadmap which includes stakeholders, including consumers and suppliers for optimizing the energy system in the future.

next ›

Featured Interview: Andreas Spiess, CEO, Solar Kiosk

“The central grid can be like shooting cannons at birds - bringing an oversized solution to rural challenges.”

In a large part of Africa, grid extension will presumably never break even given the buying power and geography constraints of Africa. In sparsely populated areas, central grid extension only makes sense to a certain extent. In this circumstance, the grid can be like shooting cannons at birds - bringing an oversized and outdated solution to specific rural challenges which need a more flexible and decentralised cost-effective approach. In our view, utilities should focus on industrialisation. Entrepreneurial options using new technologies, especially solar, that leverage distributed generation can focus on issuing “right-sized” efficient and cost-effective energy solutions to predominately private households and Small Medium Enterprises (SMEs) in rural areas.

However, energy entrepreneurs providing decentralised distribution generation (DG) face a number of challenges in many countries. Regulation is often premature, unsophisticated, and sometimes seemingly random. For example, DG operators need clarity in future central grid developments and whether DG will be able to feed into the grid if it is developed to their respective sites. Lack of clear regulations deters investors. We also need assurances that our land use and equipment will have regulatory protections. Subsidies need to be given on an equally fair basis to on-grid and off-grid developers. Currency risks have to be hedged at a fair price.

It is also really important that all players focused on driving energy access are working together. For example, random donations can be counter-productive for the private sector since they give no incentive for locals in rural villages to purchase solar appliances if they think they may get offered one for free in the future. Unorganised actions, although well-meaning, can be to the detriment of the private sector.

next ›

Featured Interview: Rob Threlkeld, Global Manager of Renewable Energy, General Motors

“We need a mind-shift on grid operation.”

Our company has a four-pronged approach to energy use and management: energy efficiency, sourcing renewable energy from both on-site and off-site production, battery storage to address intermittency, and active policy engagement. Countries and even specific utilities have different levels of sophistication in regards to the elements of our four-pronged approach to energy use and that results in a patchwork of processes across geographies that we and other companies have to manage to achieve our energy targets.

Going forward, there are two key areas for the energy sector, including prosumers, to focus on – the digital transformation of transmission and distribution, and storage.

We need a mind-shift on grid operation. Grid operation is becoming increasingly crucial for both the reliability and cost management of energy. Focusing on the digital transformation of the grid would enable real time pricing and facilitate collaboration and optimization by all players in the system. Increased digitization, increased information flow, increased data processing power, plus improved weather data – will allow for improved grid management.

Storage is fundamental to increase efficiency and to guarantee constant flow on the grid and price stability. Energy storage will become a key part of the grid and we expect the pace of change in storage could be similar to the pace of change in solar technology over past 4-5 years.

next ›

Featured Interview: Michael Tinskey, Global Director of Vehicle Electrification & Infrastructure, Ford Motor Company

“The pace of innovation on batteries and re-charging has increased at a faster pace than expected.”

Policymakers should look to integrate energy and transportation policies to couple electric vehicles with the projected growth in renewables. E-vehicles, effectively integrated as distributed energy resources, can help manage the “duck curve” challenge associated with the increase of solar PV.

The pace of innovation on batteries and re-charging has increased at a faster pace than expected. However, the wide-spread adoption and embrace of e-vehicles by customers will require a rethinking of grid governance to manage energy demands. Customers need a consistent, homogenous, inter-operable charging network. For example, in the USA, states and utilities are implementing e-mobility policies and rates independently.

This approach will not meet the needs of customers. In order for EVs to work at a systems level, the infrastructure development needs to be coordinated, for example, strategically spaced out charging stations. Automakers have a role and shared goal in pushing the focus on customer needs. In Europe, automotive producers are working together to install charging infrastructure and are collaborating with utilities (link).

The role of the utilities, automotive producers, or even third parties in developing the charging infrastructure can depend on the rate systems of and revenue drivers for utilities - in particular how demand charges factor as a component of utility revenue. Demand charges are higher in USA compared to Europe and this can influence the utilities desired role in e-mobility.

*Please be advised: new methodology introduced in 2019 means it is not possible to directly compare a country’s Trilemma performance in 2019 with its performance in earlier publications. To view the 2019 Index - which incorporates the new methodology that has been applied retroactively to historical performance - please click here.