Looking ahead a decade, air travel demand is anticipated to be equally robust, with an additional 200 million people expected to enter the middle class across the planet. Growth in revenue passenger kilometers (RPK) will regularly exceed the annual expansion of gross domestic product (GDP) in most economies—particularly in high-growth areas like China and India. Even amid global trade tensions, the projections for commercial air travel remain optimistic across all regions of the world.

Record Fleet Growth

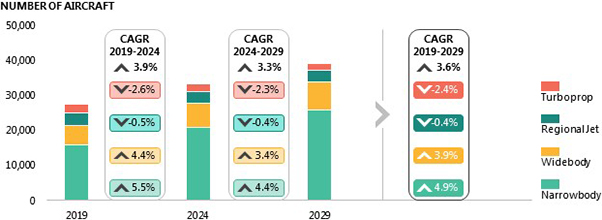

Consequently, the persistent demand is spawning record growth in the global fleet. For the beginning of 2029, our forecast projects a total fleet of 39,175 aircraft, up more than 11,600 from the 2019 total of 27,492. Between 2019 and the beginning of 2024, we anticipate the in-service fleet will grow annually at 3.9 percent—a pace that will slow to 3.3 percent for the next five years.

The order book and the corresponding delivery schedule associated with this expansion are translating into significant business for the world’s leading airframe manufacturers, Boeing and Airbus. The bulk of the fleet expansion will be narrowbody jets, such as Boeing’s 737 MAX and Airbus’ A320neo. By 2029, nearly 13,800 737 MAX and A320neo aircraft will have been delivered, at which time narrowbodies will represent over two-thirds of the entire global fleet.

Global Fleet Forecast By Aircraft Class, 2019-2029

Source: Oliver Wyman

Trickle Down Expansion of the Maintenance, Repair, and Overhaul Market

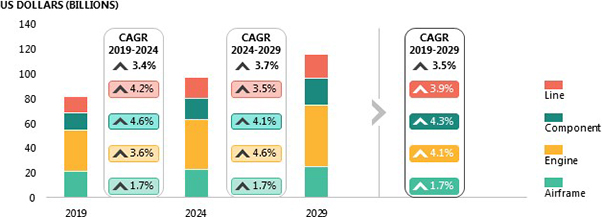

With the expansion of business in the commercial aviation industry, the maintenance, repair, and overhaul (MRO) market that supports it is also expected to grow. Total MRO spend is expected to rise to $116 billion by 2029, up from $81.9 billion in 2019. Aside from the growth in the fleet, the increase will be driven by more expensive maintenance visits and technology enhancements.

The annual average growth rate for the MRO market will be 3.5 percent over the decade. More of this growth will take place between 2024 and 2029, when MRO spend will grow $19 billion versus $15 billion between 2019 and the start of 2024. The slower initial five years will be driven by the escalating number of newer-generation aircraft that enter the fleet. These aircraft have longer maintenance intervals and replacement thresholds for such things as life-limited parts than older jets.

Growth in aviation will be more concentrated in Asia and the developing world, particularly China and India. By 2035, the Civil Aviation Administration of China projects, the number of airports in the nation will almost double, reflecting this spike in demand and the government’s big push to fund the necessary infrastructure. By the end of the decade, China will become the biggest global market for air travel and Asia will be the new center of global aviation activity.

Growth of MRO Spend, 2019-2029

Source: Oliver Wyman

The Evolution of the Global Fleet

Explore how the various aircraft fleets will change from 2019 through 2029 across the world's regions.

About the Forecast

Oliver Wyman’s Global Fleet & MRO Market Forecast Commentary 2019–2029 marks our firm’s 19th assessment of the 10-year outlook for the commercial airline transport fleet and the associated maintenance, repair, and overhaul (MRO) market. We’re proud that this annually produced research, along with our Airline Economic Analysis (AEA), has become a staple resource of aviation executives—whether in companies that build aircraft, fly them, or work in the aftermarket, as well as for those with financial interests in the sector through private equity firms and investment banks.

This research focuses on airline fleet growth and related trends affecting aftermarket demand, maintenance costs, technology, and labor supply. The outlook reveals significant changes that are important to understand when making business decisions and developing long-term plans.

Analytical topics covered include:

- Economic GDP and traffic data (measured in revenue passenger kilometers or RPKs) by geographic region and specific countries

- Historical financial performance (load factors vs return on invested capital, jet fuel spot prices, industry profitability)

- Passenger and cargo traffic, and airport infrastructure growth in select markets

- In-service fleet, retirements, orders, conversions by aircraft class (wide-body, narrow-body, regional jet, and turboprop)

- Global aircraft fleet forecast and regional fleet growth rates

- MRO market forecast by segment (line, component, engine, airframe) and aircraft platform spend

- Forecast sensitivity analysis based on economic health, traffic, fuel prices, and interest rates