Supplier — many of whom are already in full crisis mode — will need to manage the drawdown of declining product lines while simultaneously creating their future core offerings. Maintaining “old tech” solutions while rapidly venturing into “new tech” can result in overly complex product portfolios and inflated R&D budgets, potentially putting a company’s survival at risk. (See the High portfolio complexity negatively impacts profitability independent of the company’s size Exhibit below.)

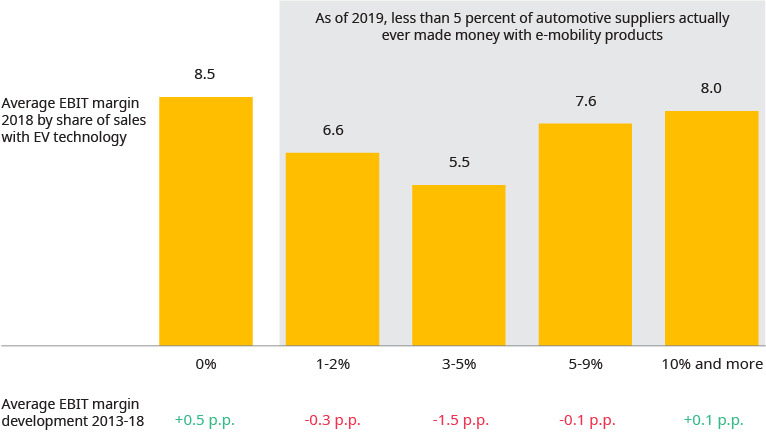

How players approach this challenge will influence their chances of success. For example, business unit leaders, driven by current performance expectations, often try to maintain control and influence over both “growth” and “cash cow” offerings — even when those would mesh better with other parts of the company. While some suppliers may dedicate the responsibilities for electric and autonomous vehicle solutions to a specific business unit, leaders of more traditional product segments may try to secure their own slice of the pie by introducing related products outside the business unit’s actual core. Such actions can put the overall company in an uncompetitive position. Another hurdle: Suppliers often accept long-term negative returns on new product areas like e-mobility, without any roadmap for reaching profitability. (See the Performance assessment e-mobility business Exhibit below.)

CAPITAL LOVES SIMPLICITY

Complexity not only kills profits, it also reduces a company’s potential to adapt dynamically to disruptive changes in markets and technology. Capital markets penalize complexity, too: Investors overwhelmingly view simple stories as winning ones. Since the last crisis in 2009, well-defined automotive supplier brands have outperformed their peers by a factor of three. But simplifying product portfolios and streamlining underlying structures remain stumbling blocks for many automotive suppliers. These companies often do not recognize that growth is not a one-way street.

For instance, one large US-based tier-1 supplier significantly simplified its offerings through major divestments of its climate and lighting business. It now purely focuses on cockpit electronics, from displays and instrument panels to telematics and infotainment solutions. As a spokesman put it: “We have become laser-focused on what we do best, and we are a very different company than we were even a few years ago. You can just be a supplier of many auto parts, but there are 25 other companies doing that. It is a race to the bottom.”

Performance assessment e-mobility business (of top 100 automotive suppliers)

Only a limited number of suppliers active in e-mobility actually make money from it — especially the “stuck in the middle players” experienced heavy profitability decline

Source: Oliver Wyman Supplier Financial Benchmarking 2020

Complex product portfolios with hundreds or even thousands of products are not uncommon in the industry. The resulting miscellany makes it difficult for investors to understand the company’s true core value proposition — its DNA. This fragmentation often results in sub-optimal manufacturing slot allocation, lack of differentiation, and declining profitability.

What is more, trendy portfolio diversification strategies can quickly lead companies off course. Investors recognize that as a company ventures into new territory where the chances of success are limited, it will find itself competing with players with superior brand recognition and economics in the new product segments.

CREATING A FUTURE-FOCUSED PORTFOLIO

Suppliers have several options for reducing product complexity and building a profitable technology portfolio.

Review, prune, streamline

To survive the technology transition, automotive suppliers must adapt and rebuild their sweet spots. This means a complete assessment of the portfolio, starting with the company’s strategy and including its competencies and capabilities, financial stability, global footprint, and workforce skills. It should evaluate the overall profitability and margins of each business unit and identify synergies and dependencies. Finally, a product group assessment should look at size, market share, margins, sustainability, value-added, and capital intensity.

A systematic review typically reveals that supporting the status quo is the wrong strategy. Companies often need to search for strategic partners or make tough divestment decisions. They often must cut back on products and complete business units as they redefine and streamline their business models. While commoditized products with limited tech differentiation or low cost-cutting potential would seem obvious candidates for selling, some companies have also revised their recent portfolio investment aspirations despite entering booming segments with large growth potential. Why? Leaders realized they would have to incur high ongoing R&D expenses to gain a meaningful share in markets characterized by increasing price competition.

Generate cash and focus resources

Once a company develops a new business model, it needs to finance it and focus resources on the right topics. A variety of options exist to generate cash, such as introducing operational improvements like lean or agile practices to boost the bottom line, or efforts to simulate topline performance.

Another option involves entering the right partnerships to pool complementary capabilities, divide costs, and share risks. For instance, four large Japanese automotive suppliers joined forces to accelerate the development of their next-generation vehicle technologies and cut product and research & development (R&D)-related costs. The companies merged to create a more robust entity with the strength to become a major player in autonomous vehicle and electric vehicle (EV) technologies.

Develop an investor story and become a credible partner

To overcome the market’s hesitation to take part in the incumbent automotive industry, suppliers need to craft a compelling investor story. At the same time, they need to become a credible partner on profitable growth products that align with their DNA. In one cautionary example, a European supplier invested in a variety of e-mobility opportunities that had little to do with its core value proposition and has since struggled with this strategy. Series production ramp-up has remained far below expectations, as some products remain technically inferior and other players enjoy higher credibility with end customers.

Use strong key performance indicators (KPIs) and governance policies

Suppliers need to manage their selected new technologies actively, requiring new KPIs and strong governance structures to ensure projects stay on track. Consider installing a separate roadmap and KPI base for growth businesses to protect them from the core organization, without compromising the ability to steer them. Some larger supplier organizations even develop separate access to capital markets for traditional and new technologies and business units, a move usually rewarded by shareholders.

SETTING A FOUNDATION

The decade ahead will be an extraordinarily turbulent one for automotive suppliers. Incumbent suppliers need to set a foundation capable of supporting the new business models required to ensure their survival. This process must start now, with a frank assessment of the company’s aspirations, capabilities, and future value proposition. Only by doing that can industry players hope to catch the market’s eye and win in tomorrow’s automotive industry.