This article was first published on June 16, 2020.

Last month, Oliver Wyman published initial results from the COVID-19 US Shopping Outlook Survey. Americans displayed limited confidence across multiple fronts: many faced shelter-in-place restrictions and were nervous about going back out, propensity to purchase non-necessities was low, and many were planning to save instead of spend post-pandemic.

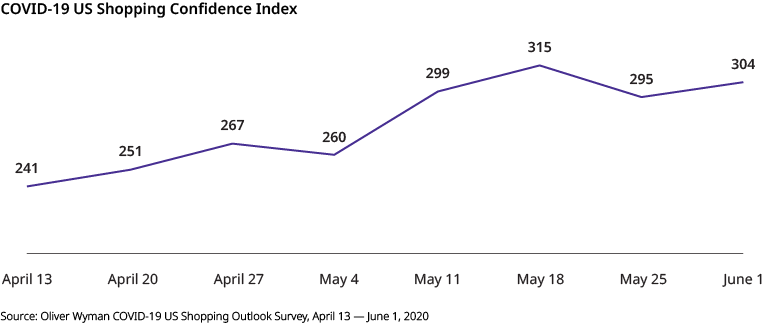

One month later, a number of green shoots are starting to emerge. Our COVID-19 US Shopping Confidence Index (SCI), a proprietary measure of consumer shopping propensity based on purchase plans and overall financial confidence, has been rising, and now sits at 304 as of early June. Although there is still a long way to go — we estimate the SCI to be ~700 in a normal environment — confidence has risen 25 percent since mid-April.

As we track this uptick in consumer sentiment, we’ve been keeping a close eye on responses related to financial confidence (ability and potential willingness to spend), comfort in going out in public (and, therefore, having places in which to spend), and purchasing intentions (specific plans to spend), as these themes provide signposts for a sustained recovery. As we explain below, we have seen notable improvement across some, but not all, of these indicators.

SURPRISING CONFIDENCE

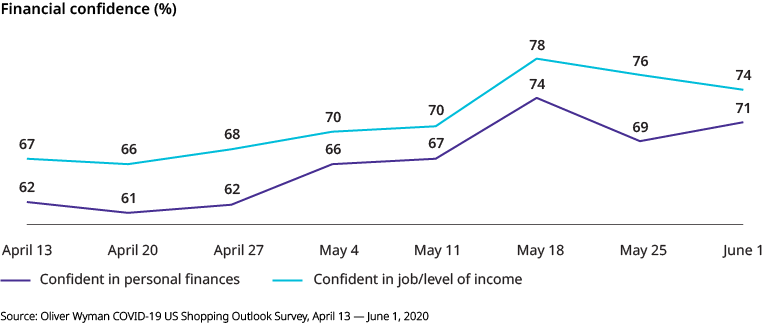

Financial confidence has remained relatively high — surprisingly — throughout the pandemic and, in addition, has improved in the last month. Confidence in personal finances has remained highly correlated with confidence in job/level of income.

VENTURING OUT

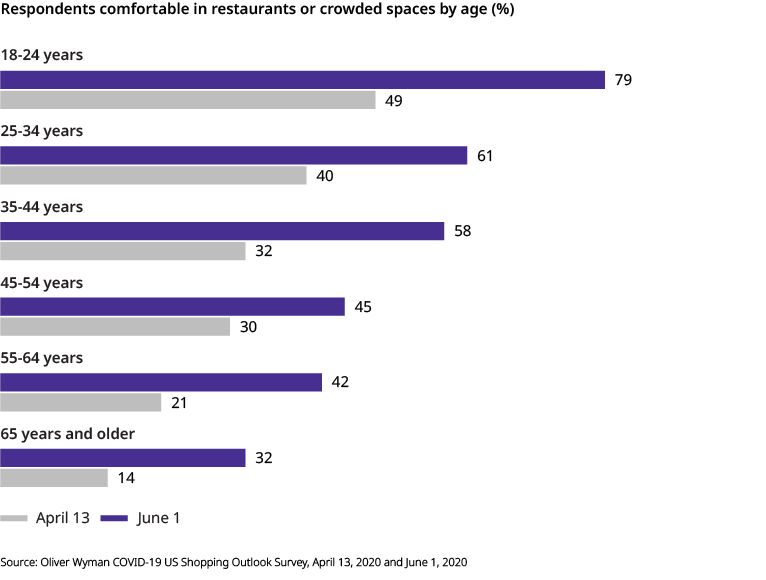

With shelter-in-place restrictions now being relaxed nationwide and businesses re-opening in a phased manner, respondents are showing a willingness to return to restaurants and other public spaces where people may congregate. Although comfort in venturing out is highly correlated with age, we’ve noticed a significant uptick among all age groups.

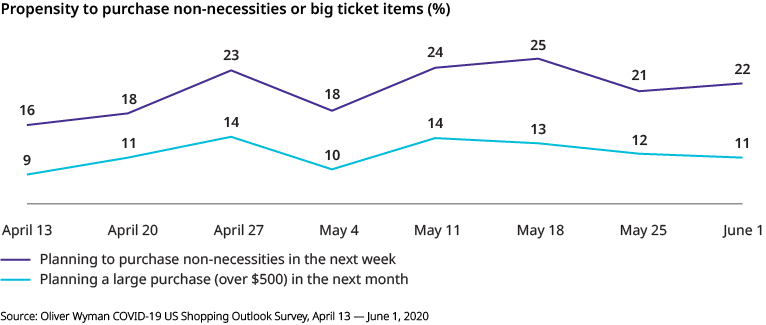

CLOSED WALLETS

Although many respondents indicate strong financial confidence and are now more comfortable with going out in public, willingness to spend has shown only slight improvements in the past month. Few respondents are planning discretionary or big-ticket purchases, as uncertainty regarding the pandemic looms over everyday life. We will continue to track these indicators for signs of progress as the pandemic evolves.

For more on the Shopping Outlook Survey, listen to our June 2020 webinar, COVID-19 and Impact on the US Financial System: Payments, check out our May 2020 article introducing the survey, and please stay tuned for further updates. If you have questions, please reach out to us at payments@oliverwyman.com.