This article first appeared in Forbes Middle East.

The way we conduct financial activities is rapidly evolving, driven first by the global financial crisis and now by digital disruption. This has resulted in a massive change in the demands placed on financial regulators, especially across the Gulf Cooperation Council countries, and in turn has posed a significant challenge for financial supervision in the region.

The traditional approach based on entity type is no longer sufficient and as such regulators must embrace activity-based regulation. The complex combination of risks in the financial system is shifting in ways that require new technology and new skills for risk identification and mitigation.

CONSEQUENCES OF A CHANGING FINANCIAL INDUSTRY

In an industry that is rapidly transforming, two fundamental changes pose major consequences for financial supervision.

First, correlations between financial activities and types of institution are breaking down. Payments, for example, which were once the preserve of banks and credit card companies, are now shifting outside the “regulatory perimeter,” where the light of financial supervisors does not shine — a change effected by the number of fintechs and online retailers entering the market. The same is happening with lending, as the number of non-bank platforms increases. Open banking will accelerate this trend.

Second, operational risk is moving outside of supervised entities into the firms to which they outsource critical functions, such as data storage, reporting, and transaction processing. Outsourcing critical functions does not reduce the disruption that their failure would cause to the financial system and its customers. But it does remove them from the direct purview of supervisors.

Keeping up with these developments will require corresponding changes within supervisory agencies. It will require a colossal effort to develop the necessary regulations, rules, and guidelines, as well as to ensure that the regulatory skill sets are in place to effectively supervise it.

MOVING TOWARD ACTIVITY-BASED SUPERVISION

Although entities central to the financial system will still need to be covered, attention must shift toward types of activity, such as lending, payments, and data storage. The modularization of financial services will require financial supervisors to move the focus towards activity-based supervision.

Advanced analytics, big data, and AI can help GCC supervisors leapfrog regulation with risk- pattern recognition, early-warning sign als, risk identification crowd-sourcing, and social listening, as well as support economically critical functions to endure shocks regardless of what type of firm performs them.

With some of these activities now performed by firms falling outside traditional industry oversight, this may require some extension of supervisors’ legal authority in the region. It will also require changes in the way they organize themselves internally, complementing teams that cover institutions with teams covering activities.

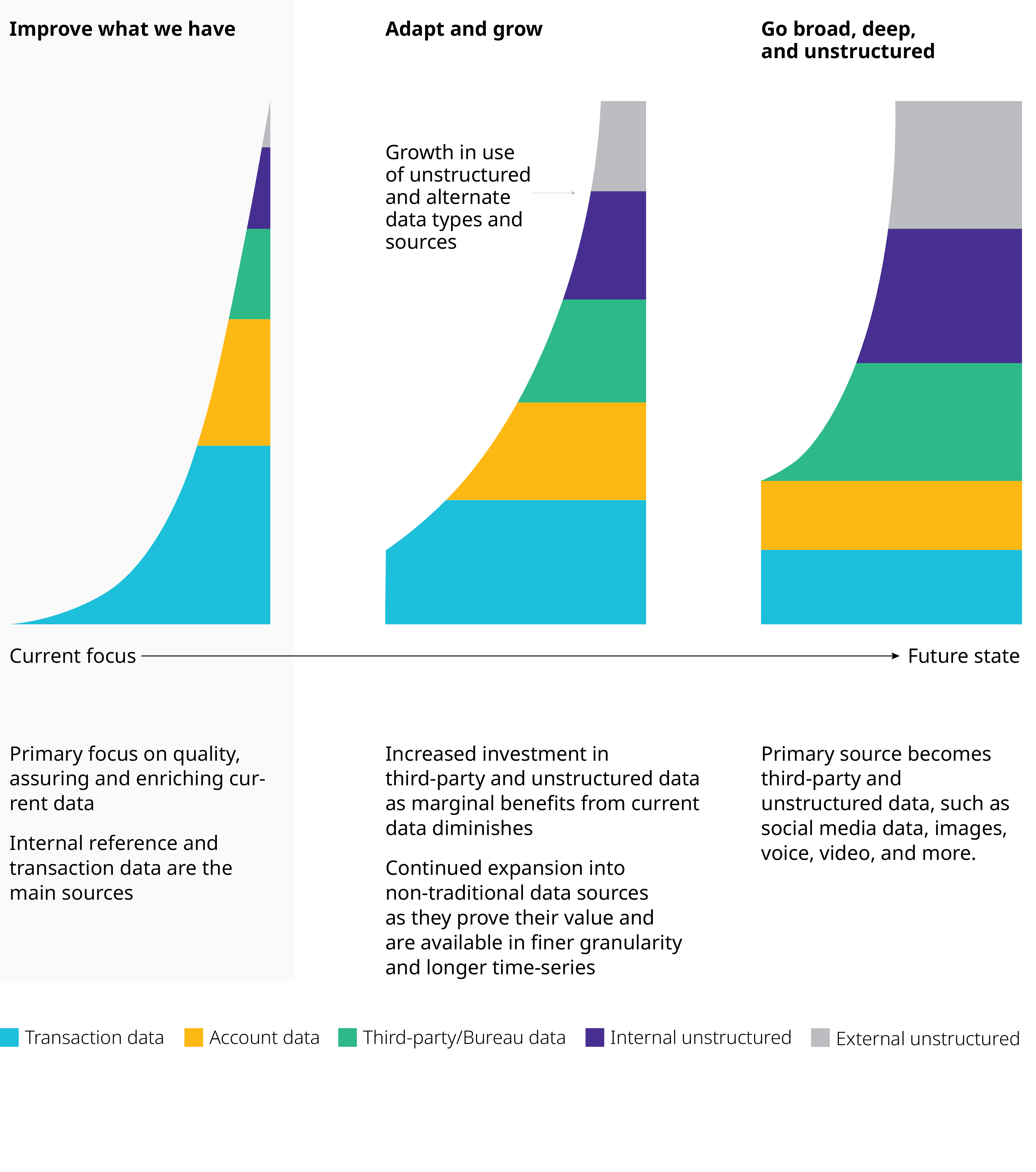

How to improve early warning systems through the use of new data sets

Area represents universe of potential data while curved line represents frontier of data to be utilized

Source: Oliver Wyman Data Analytics Capabilities Survey, Oliver Wyman analysis

SUPERVISORY “BLIND SPOTS”

As business models rapidly transform, the chance of supervisory “blind spots” increases. Supervisors are, by nature, outward looking. But they will need to be become more “outward working,” engaging with industry participants to make sure they understand the nature and location of risks in the system.

Financial supervisors in the GCC have begun to embrace fintech, but currently lack a full- fledged regulatory environment, hence piloting in sandbox formats. It will require a colossal effort to develop the necessary regulations, rules, and guidelines, as well as the regulatory talent to effectively supervise and eradicate such blind spots.

Supervisors will also need to make better use of the same advances in information technology that are transforming the operations of financial firms — cheaper data storage and communication, digital automation of previously laborious processes, and data science. As with the firms they supervise, this technology can help them do their job better while cutting their operating costs.

For example, risk assessments now rely on data samples supplied by regulated firms and on expert evaluation of their processes and methodologies. This could soon be replaced by analysis of comprehensive data regarding the entire population of transactions, assets, or customers, observing the results of the methodologies applied rather than their apparent logic.

Advanced analytics, big data, and AI can help GCC supervisors leapfrog regulation.

EARLY INTERVENTION

With financial activity almost completely transparent to supervisors, they could become more effective in monitoring key risk indicators and intervening early to steer the industry away from emerging risks. This would require them to draw on a wider range of data sources, including alternative sources, such as blogs, social media, and industry chat rooms, and to adopt advanced analytic techniques, such as machine learning.

Digital technology could also allow supervisors to plug into the firms they supervise. Not only could data be drawn directly into supervisors’ systems, but compliance could be quasi- automated by regulations being directly transmitted into financial firms’ systems — at least where the rules are sufficiently quantitative or otherwise rule-based. Operating costs will be reduced on both sides.

Put another way, supervisory agencies — or parts of them at least — will need to become more like fintechs, but this also means accepting more risk in the financial system than regional supervisors are used to.

The safety of the supervisory system has relied for the longest time on very stringent rules and controls on prudential ratios and capital ratios. This will not be sufficient for fintech, where the margin for operational and disruptive risk is higher and will result in a difficult trade-off between slowing fintech development or accepting more risk both in quantum of risk and new risk types.

This transformation cannot be achieved with the current mix of staff at most supervisors. Lawyers, economists, and risk analysts will still be needed. But supervisors must enter the labor market competition for data scientists and programmers. Attracting them will require new working arrangements and career paths at supervisory agencies.

This will be a difficult transition. But if they fail to make it, GCC supervisors will find it increasingly difficult to keep up with the industry they oversee.

AUTHORS

Mathieu Vasseux is a Dubai-based partner in the Financial Services practice.