US powerhouses have dominated the wholesale banking industry for the past decade. Now, the landscape is changing. Global and regional banks based outside the US are poised to benefit, closing the returns gap. However, all banks will need to respond to dramatic shifts in economics and the increasing pressure from non-bank competitors.

Navigating monetary policy, fiscal stimulus, and new capital regime

Over the past 10 years, the wholesale banking industry has seen a significant transformation, adapting its business model to increase resilience and generate sustainable returns. However, these efforts may soon face challenges due to two major shifts in the operating environment: the conclusion of the easy monetary policy and fiscal stimulus supercycle, and the introduction of a new capital regime starting in 2025. These shifts will place profound pressure on the economics and perimeter of wholesale banking. The recent rise in interest rates triggered a contained banking crisis in March 2023, challenging long-standing assumptions about liquidity and interest rate risk management. Additionally, new capital rules, particularly the Basel 3 Endgame rules proposed by US regulators, may fundamentally change the economics of wholesale banking and drive some activity out of the banking system entirely.

Higher interest rates and growth opportunities

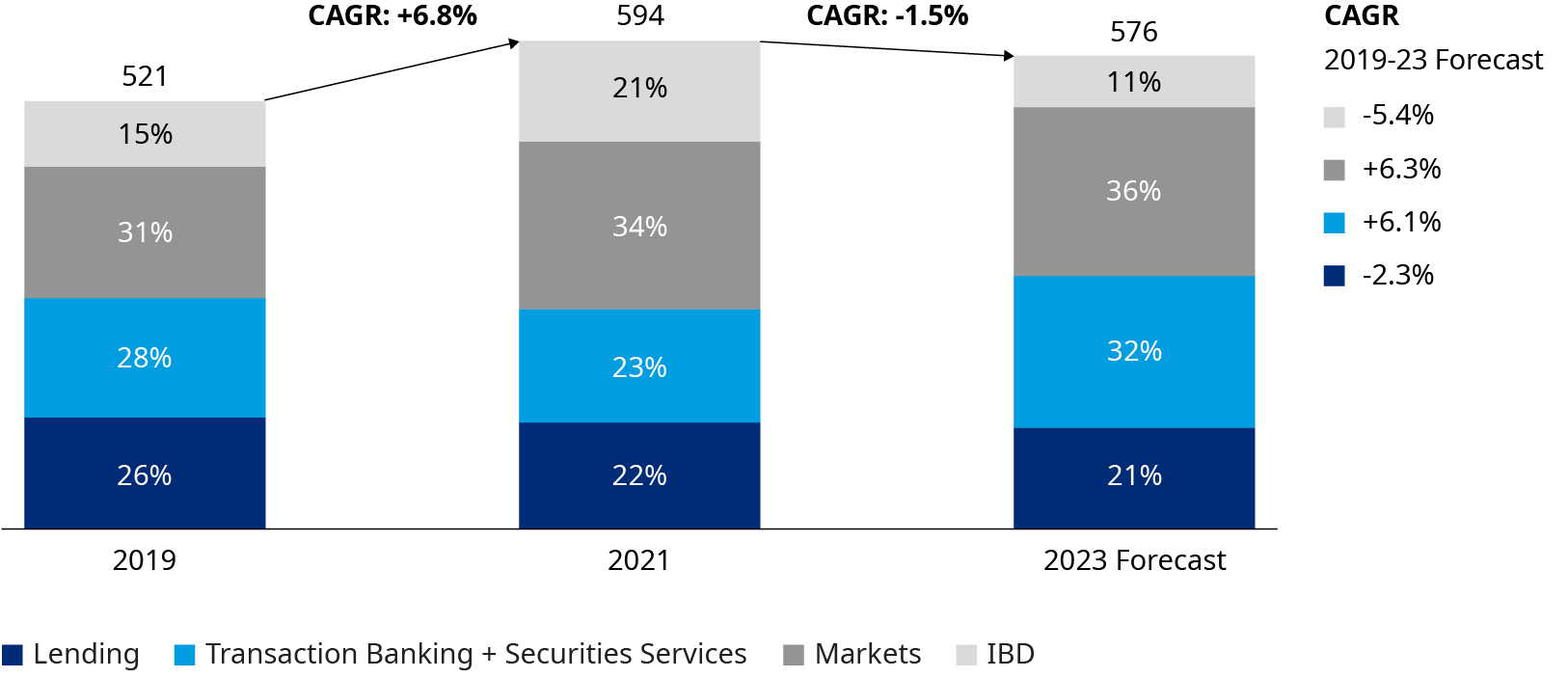

Despite the challenges, there is still positive news for banks. Higher interest rates will boost revenues and returns for banks with substantial transaction banking and securities services businesses. We predidct significant growth in these areas between 2020 and 2025, representing a larger share of the industry revenue pool. Furthermore, balanced implementation of Basel 3 Endgame capital rules outside the US will create opportunities for banks in other parts of the world to capture market share and close the returns gap with US leaders.

Adapting business models for improved economic performance

The structural shifts in the operating environment could also be the catalyst for wholesale banks to make long-awaited changes to their business models, leading to a step change in economic performance. By repricing and adapting their business models, US wholesale banks could potentially add back points to their return on equity (RoE), mitigating the drag caused by the new capital rules. This transformation could leave the global industry with an average RoE of 11.06% and US banks with an average RoE of 11.9 to 13.5% once the process is complete.

To succeed in this changing landscape, banks must build resilience into their revenue models, deepen and defend client relationships, adapt their business models to position themselves at the center of new ecosystems, and pull the right cost levers tailored to their target business model. While the US proposals to implement Basel 3 are still under review and may be revised, wholesale banks must be prepared to adapt to the new rules and navigate the varying starting points and strategic paths forward.

Industry outlook — revenue pools and economic scenarios

In the Industry Outlook section of our report, we examine the evolution of global wholesale banking revenue pools from 2023 to 2025 under three economic scenarios. We analyze the impact of inflation, monetary policy, and asset prices on industry revenues. Despite recent challenges, industry revenue pools remain structurally higher than pre-COVID levels, reflecting increased volatility and yield in the system. The outlook varies by business line, and successful players will leverage their advantages in driving robust interest income, scaling in liquid trading to capture sustained volatility, and accessing rapidly growing businesses and markets.

US capital rules and value shifts — the impact of Basel 3 Endgame

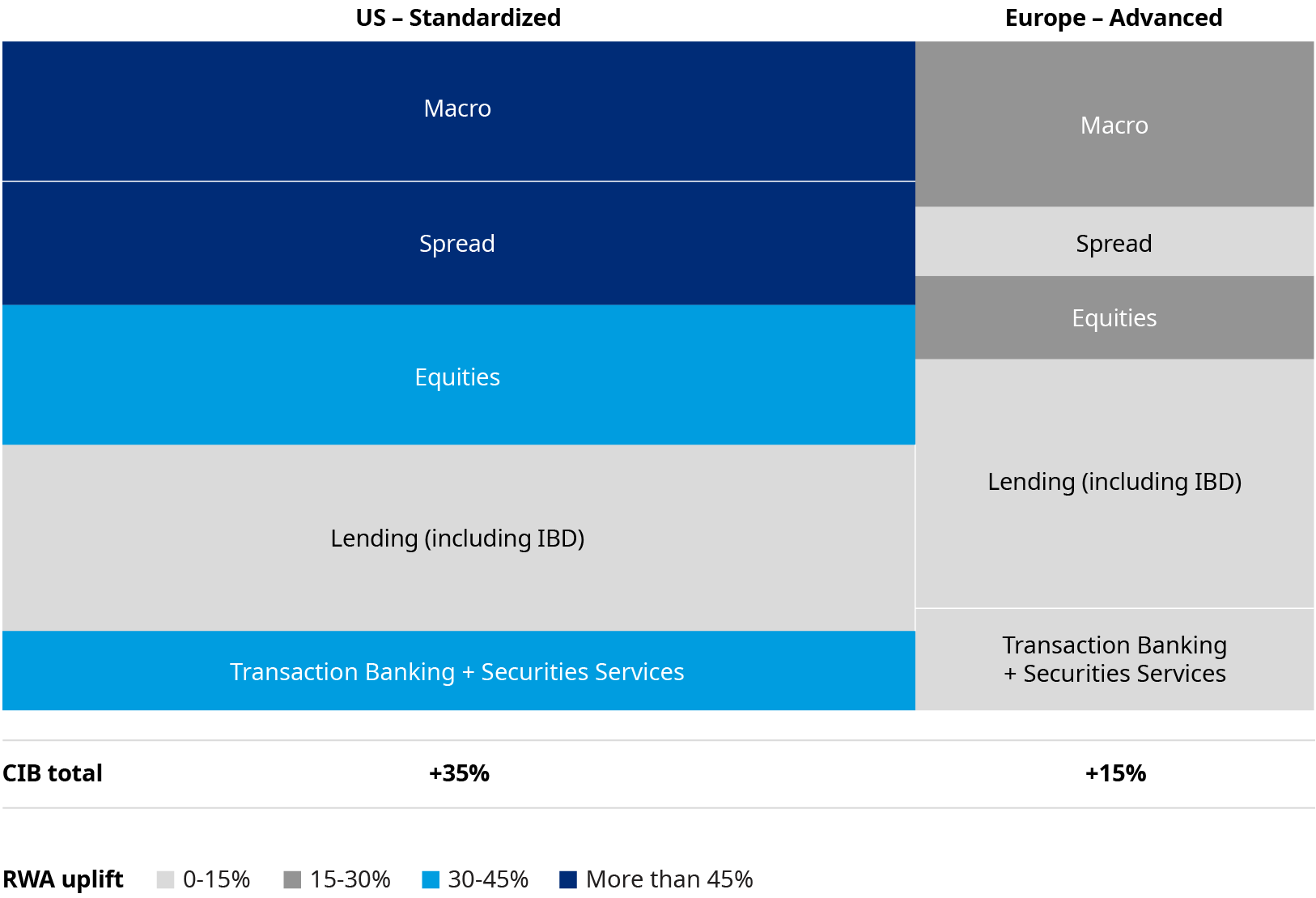

The US Capital Rules and Value Shifts section of our report delves into the impact of the proposed Basel 3 Endgame capital rules for US banks' wholesale banking businesses. The proposed rules represent a sweeping change to the bank capital regime and could have a material impact on wholesale banking businesses. Our analysis supports the view that the proposed rules would add a significant increase in risk-weighted assets for wholesale banking businesses.

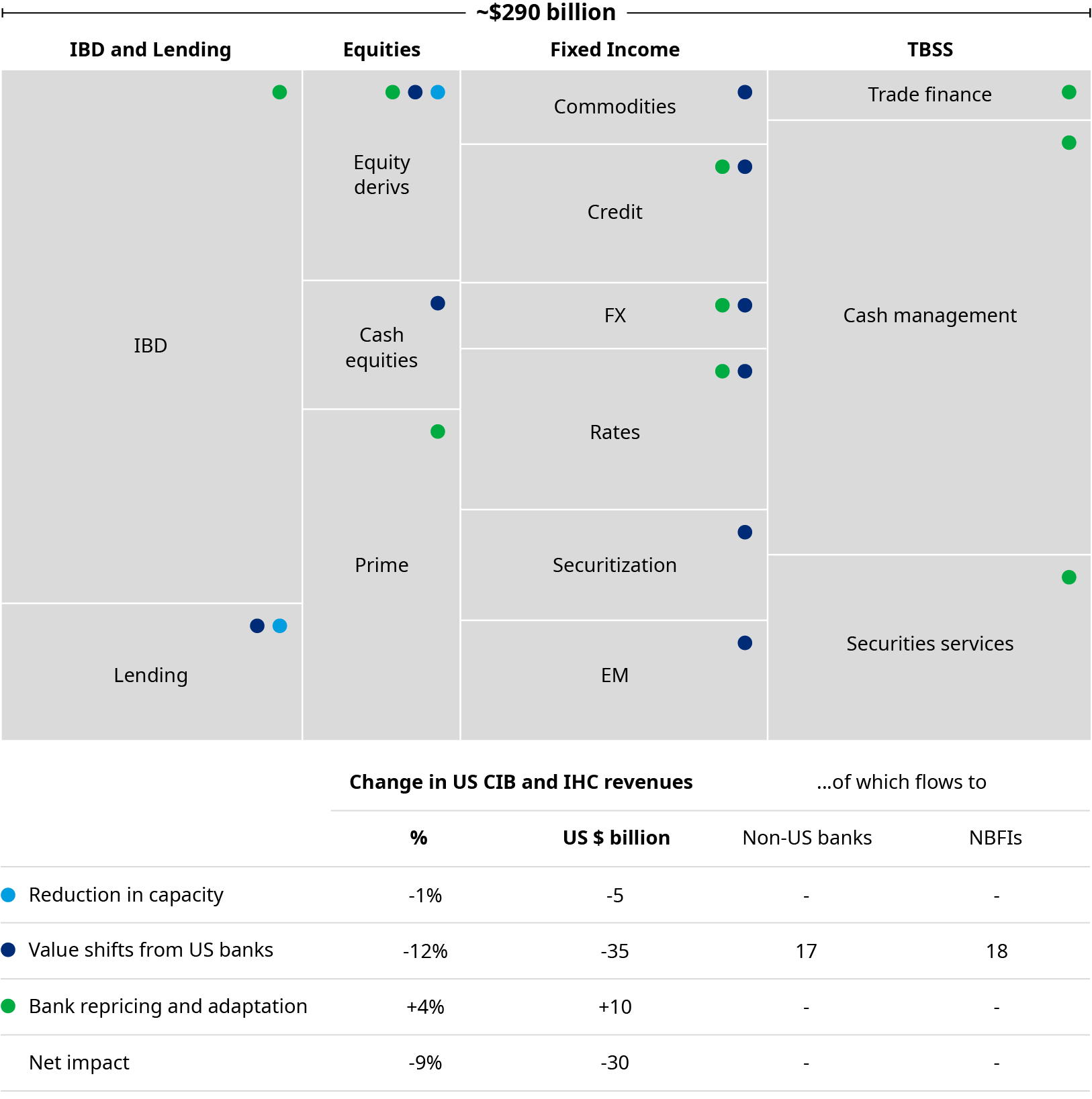

The outlook for the wholesale banking businesses of major international banks outside the US is cautiously optimistic. The impact of new capital rules would affect US banks more than international players, potentially leading to the release of capacity and $15-20 billion in revenues that could be captured by these international banks. However, there is a tension for these banks as they face pressure to allocate capital to wealth, asset management, commercial, and consumer businesses with more attractive multiples. This tension is expected to limit the potential revenue growth for these international banks to $6-8 billion.

To achieve even these levels of growth, it would be crucial to execute disciplined strategies that strengthen the client franchise, create barriers to entry against non-bank competitors, and improve economics by controlling capital and cost escalation. Additionally, non-bank financial institutions, particularly in the US market, stand to benefit from the proposed global capital rules, as they would face less pressure in holding risk and providing capital and liquidity to the market.

The key to thriving in the new era of wholesale banking

Strategic conviction and execution will be more crucial over the next five years than it has been since the global financial crisis. Banks must explain their strategy and path to strong returns amidst potential disruptions from new capital rules. While challenges exist, there are meaningful opportunities for all wholesale banks to grow and deliver strong returns. However, competition is fierce, and the economics of the business are vulnerable to external shocks and market perceptions.

One of the key lessons from the post crisis period is that banks that moved early and with conviction were the big winners in the decade that followed. Wholesale banks cannot afford to wait on the sidelines to act.