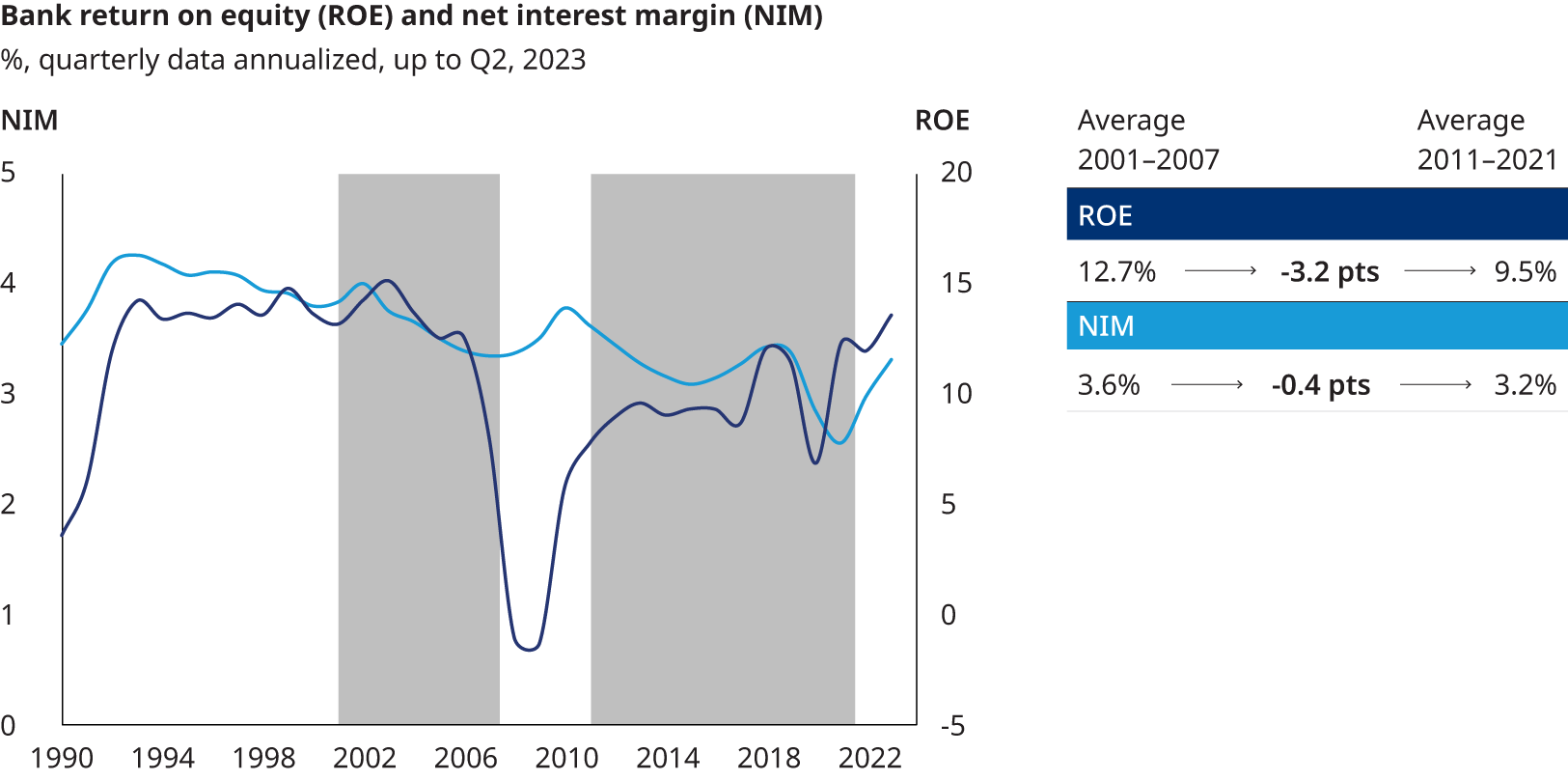

The dynamics of the financial sector shifted seismically when the period of Low for Long monetary policy — roughly 12 years marked by low interest rates around the world — abruptly ended in the second quarter of 2022 and moved toward what we call the New Monetary Order. To date, the transition to this New Monetary Order has been marked by central bank actions to combat inflation, primarily by rapidly raising interest rates and shrinking their balance sheets. While Low for Long saw a decline in average bank return on equity (ROE) and net interest margin (NIM), bank profitability has begun to rise along with interest rates. However, the challenges this transition poses began to emerge in early 2023, when Silicon Valley Bank (SVB) and several other firms with business models too heavily reliant on accommodative monetary policy floundered.

In addition to monetary policy, another important driver of evolution in this period has been the plethora of tougher banking regulations, with a particularly significant impact on global systemically important banks (GSIBs). In this paper, we analyze the effects of Low for Long on the financial sector and draw out four key takeaways with forward-looking implications for the complex current environment and beyond.

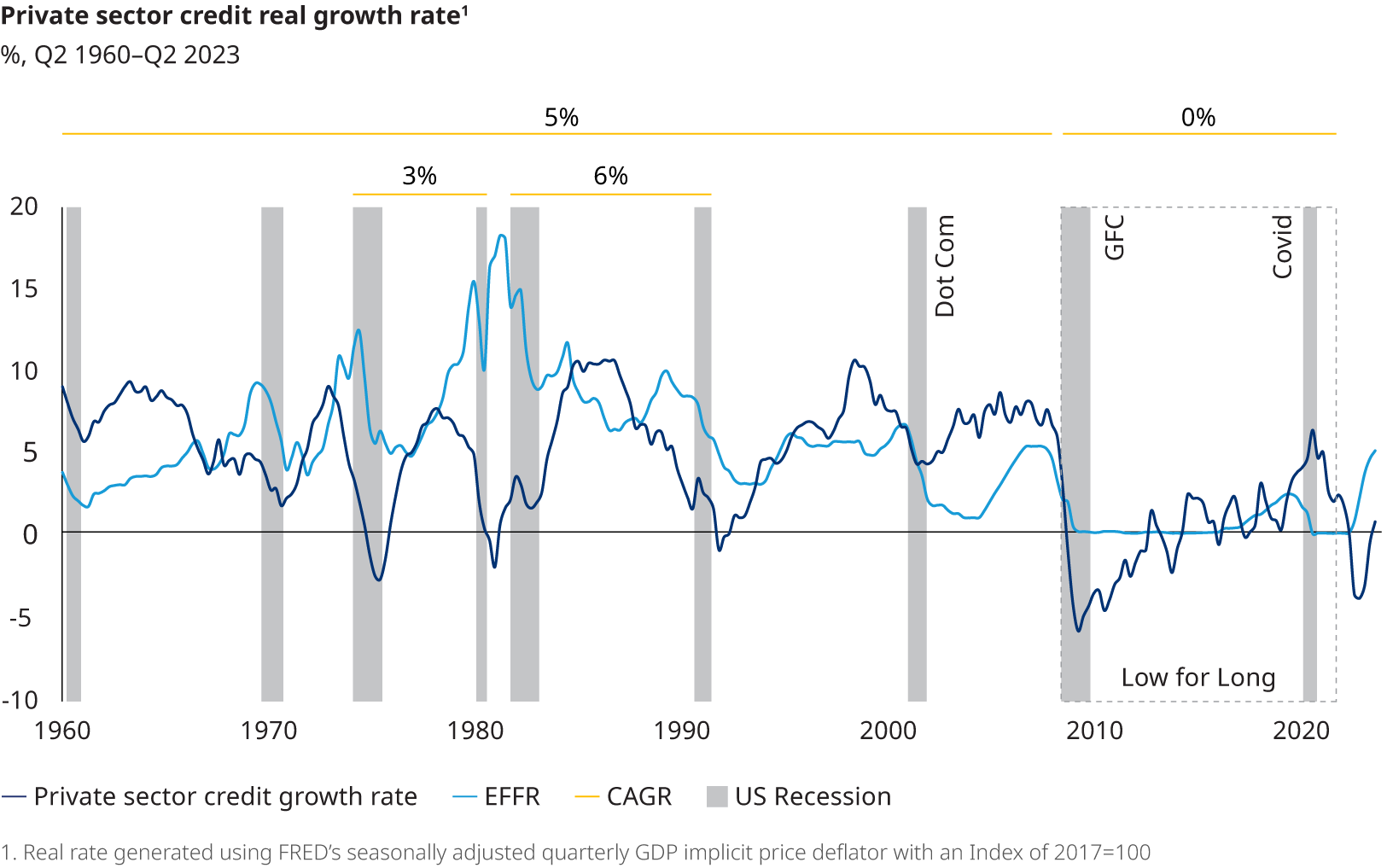

Anemic private sector credit growth

Private sector credit growth came to a halt during Low for Long compared with previous multidecade trends, falling from a 5% compounded annual growth rate in real terms from 1960–2007 to a 0% growth rate from 2008–2021, despite historically low interest rates. Significant deleveraging by both households and businesses immediately following the global financial crisis (GFC) shrank private sector borrowing. While growth recovered in consumer and business lending, it remained sluggish in residential real estate, and overall growth did not reach pre-crisis levels.

The New Monetary Order is subject to significantly higher and more volatile rates as well as substantial economic uncertainty, which will likely hinder any reversion of private sector credit growth to long-term trends. This will further increase competitive pressure as players fight over any high-growth segments.

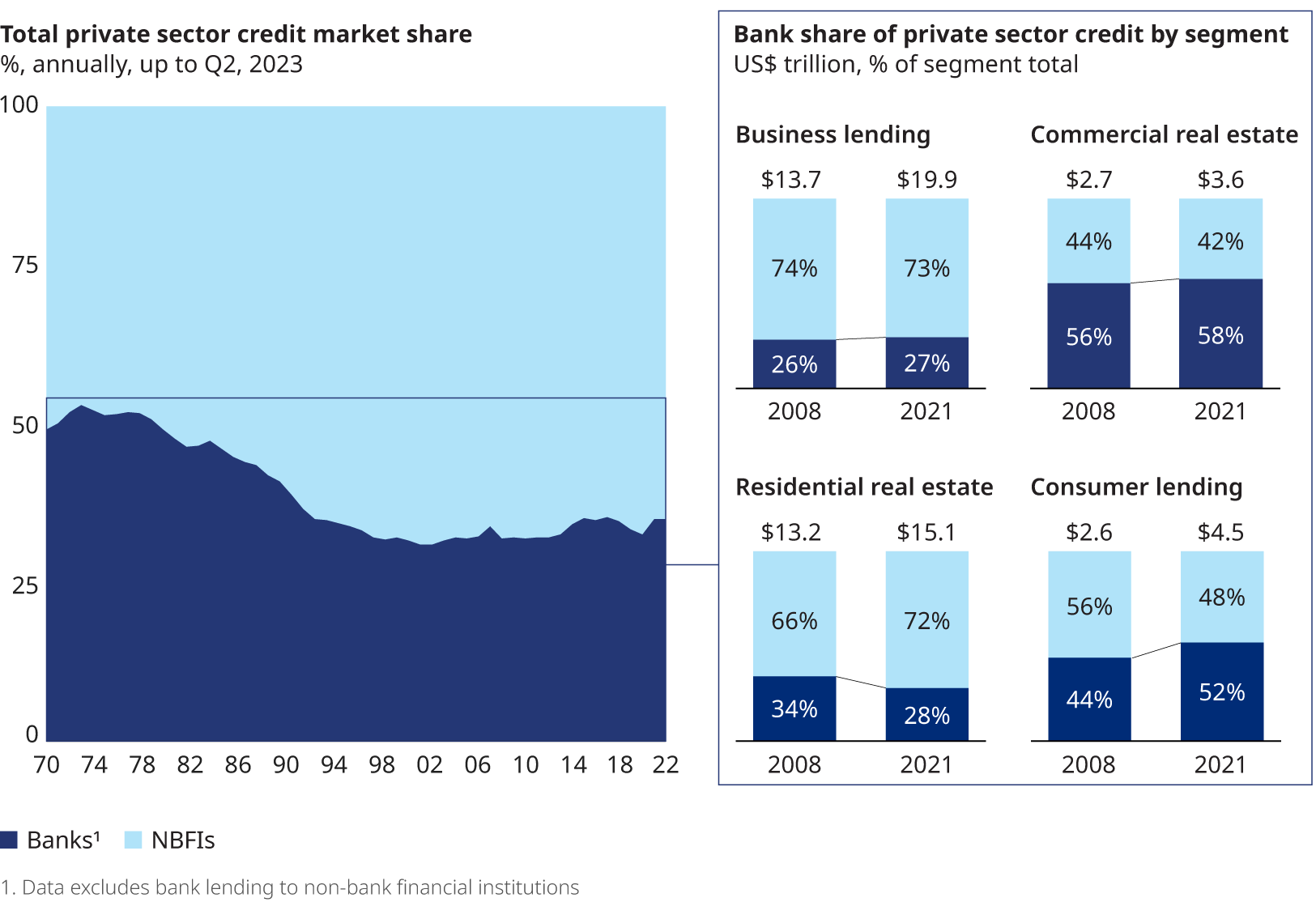

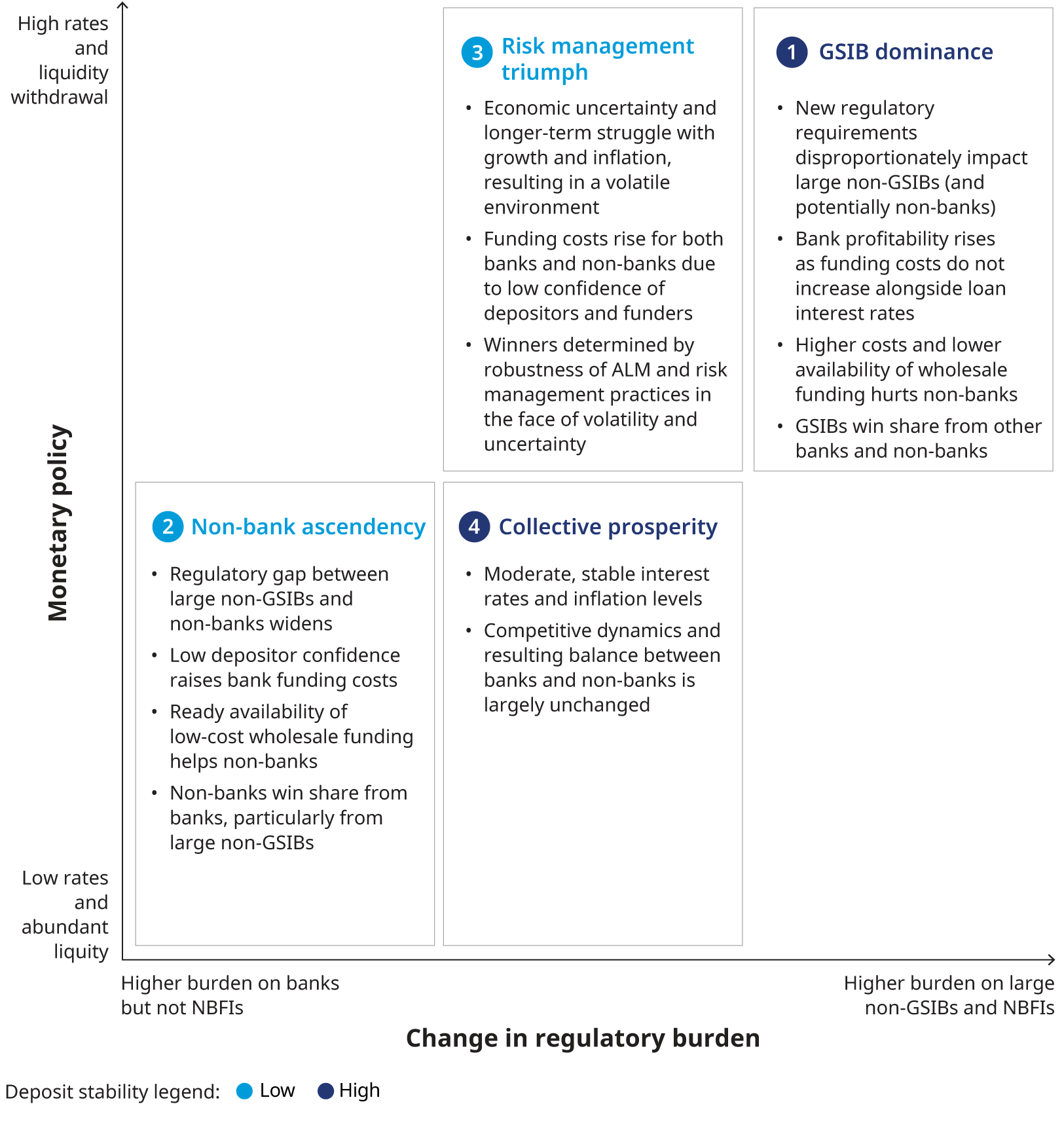

Market share dynamics shaped by the interest rate environment and relative regulatory pressure

While credit growth has been lackluster, competition has been fierce. Low for Long was marked by significant shifts across segments between banks and non-banks (although little change in aggregate), as well as between global systemically important banks (GSIBs) and non-GSIBs, largely driven by the relative intensity of regulatory pressure on these institutions.

Non-bank financial institutions, significantly less intensely regulated than banks as a whole, sought higher yields and gained share in riskier business lending. From 2007 to 2021, leveraged loans held by non-banking financial institutions (NBFIs) more than doubled, while their management of private debt assets increased by more than five times.

On the other hand, consumer lending was a bright spot for banks, substantially offsetting the loss of market share elsewhere. Overall, the shares of private sector credit remained largely the same for banks and NBFIs.

Non-GSIBs took share away from the US GSIBs in most credit asset classes, resulting in more than an eight percentage point loss in market share for GSIBs from 2009 to 2021, excluding loans to other financial institutions. This market share loss declined to three-and-a-half percentage points when including loans to other financial institutions, a big part of which was tremendous growth in financing NBFIs, which grew by a factor of more than 10 during Low for Long.

Looking ahead, the regulatory pressure on all banks is increasing further relative to non-banks. At the same time, the regulatory gap between GSIBs and large non-GSIBs is likely to narrow, as many stringent regulations and supervisory requirements that previously applied only to GSIBs will apply to large non-GSIBs as well.

Competition for high-quality deposits

Running a profitable bank with a strong risk-return profile under the New Monetary Order will hinge on optimizing asset-liability management (ALM). A stable deposit base will be central to this task, albeit significantly trickier to achieve than it was during Low for Long.

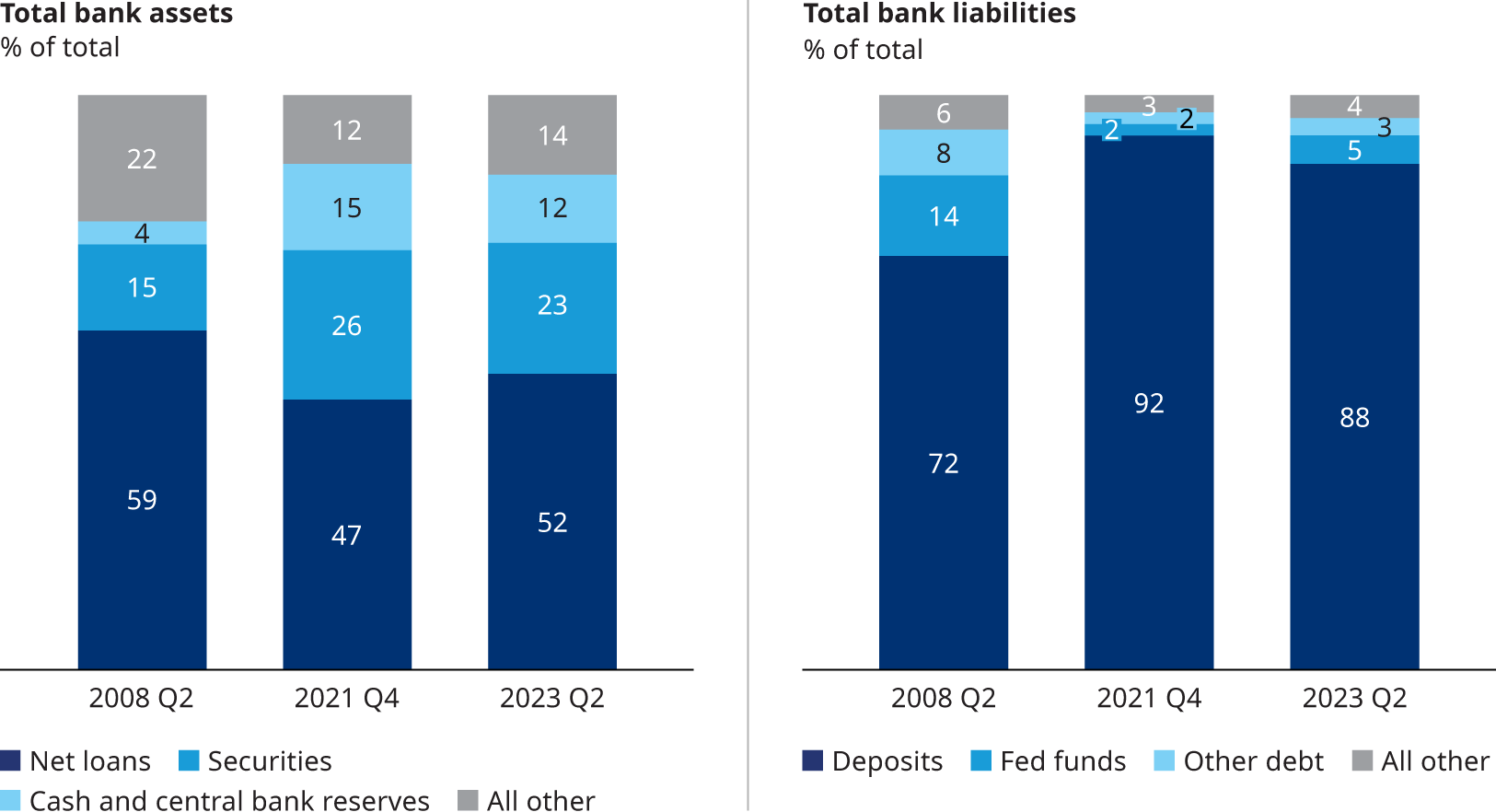

Indeed, deposits are becoming a battleground for banks, with deposit betas emerging as a major driver of earnings volatility. During Low for Long the banking system became more reliant on deposits as a source of funding. Deposits comprised 92% of bank liabilities in 2021, compared with 72% in 2008. With rapidly rising rates, this number has decreased to 88% as of the second quarter of 2023.

Deposit movement is faster and stronger in some segments, with businesses serving more sophisticated customers experiencing elevated deposit betas. Combined with an uncertain interest rate environment, which exacerbates the volatility of depositor behavior, the ability to understand, acquire, and retain higher-quality deposits will be a key competitive differentiator.

On the assets side, regulatory shifts during Low for Long pushed banks to increase their securities holdings, while the interest rate environment prompted them to extend the duration of their investment portfolios in search of yield. This resulted in substantial unrealized losses in available for sale (AFS) and held to maturity (HTM) securities portfolios when rates rose, with unrealized AFS and HTM losses for FDIC-insured institutions peaking at $690 billion in the third quarter of 2022. Unwinding the ALM failings of the past is a huge task ahead for the system.

Value of optionality in balance sheets and business models amid volatility return

The past two years have subjected firms to a range of different conditions, with some weathering the storm better than others. Firms that had strategies built around Low for Long conditions suffered, as assumptions of continued low rates or stable financial conditions were proven unfounded.

Significant uncertainty around the interest rate environment, deposit betas, economic growth, and lending volumes, as well as other tectonic shifts such as climate, geopolitics, and digitization, is making it more challenging than ever to provide earnings guidance. Proactive risk management will be at a premium in the face of uncertainty in the years ahead, and firms should seek opportunities to invest in cheap optionality. This could take the form of hedging, strengthening, and diversifying workforce expertise, or placing bets on a wider range of business initiatives.

We recommend scenario analysis as a way for financial institutions to prepare for the future. We end this paper with a set of recommendations relevant to financial institutions and policymakers alike as the industry navigates the New Monetary Order.

This paper focuses on the US experience. While many of these themes were present globally, experiences varied by country and region. As a result, we are releasing separate reports providing perspectives on the New Monetary Order for Europe and the UK, Asia, and Australia.

Additional contributors include Ted Moynihan, Managing Partner and Global Head of Financial Services; Til Schuermann, Partner and Co-Head of the Americas Finance, Risk and Public Policy Practice, Hannah Vazquez, Principal Finance and Risk Practice and Salman Asaf, Engagement Manager Finance and Risk Practice.