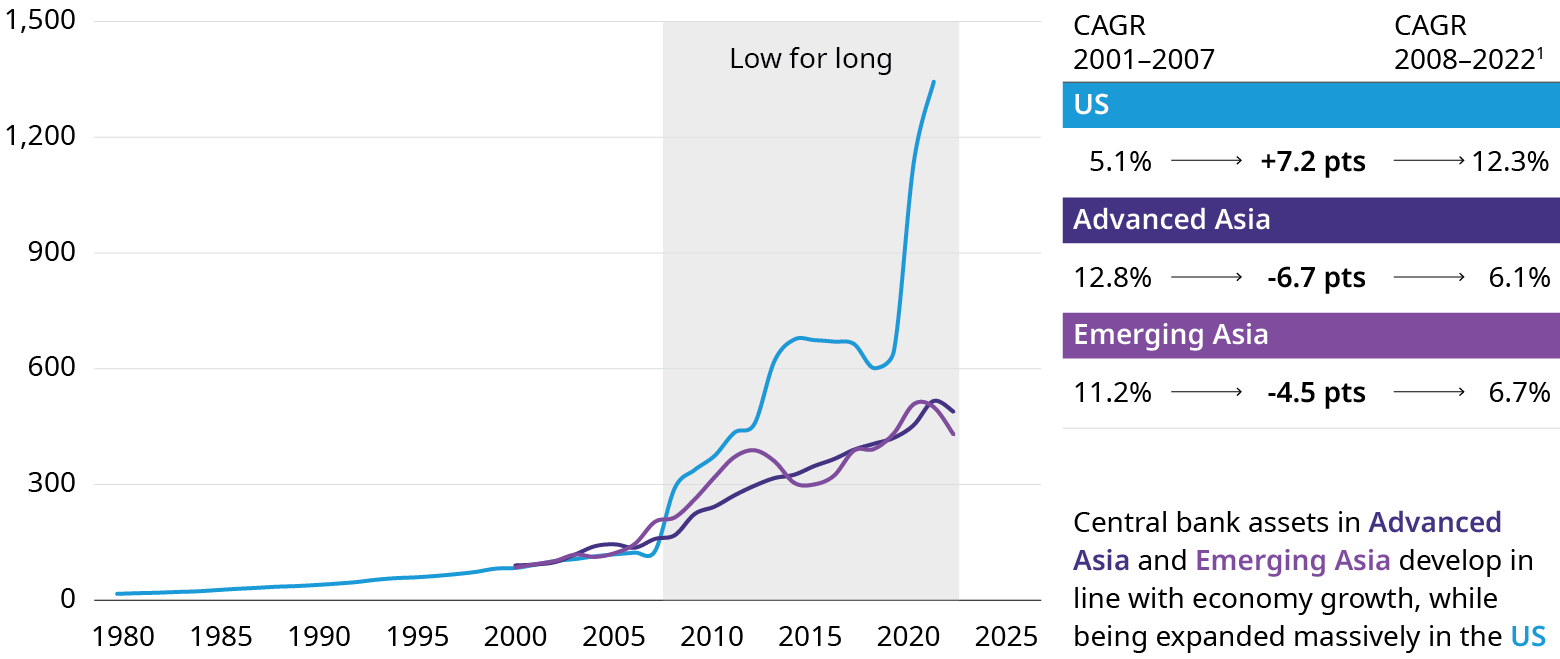

The global financial landscape is in the midst of a seismic transformation. A nearly 15-year period of ultralow interest rates, known as “Low for Long,” is giving way to a “New Monetary Order” marked by rising rates and, in some regions, stubborn inflation.

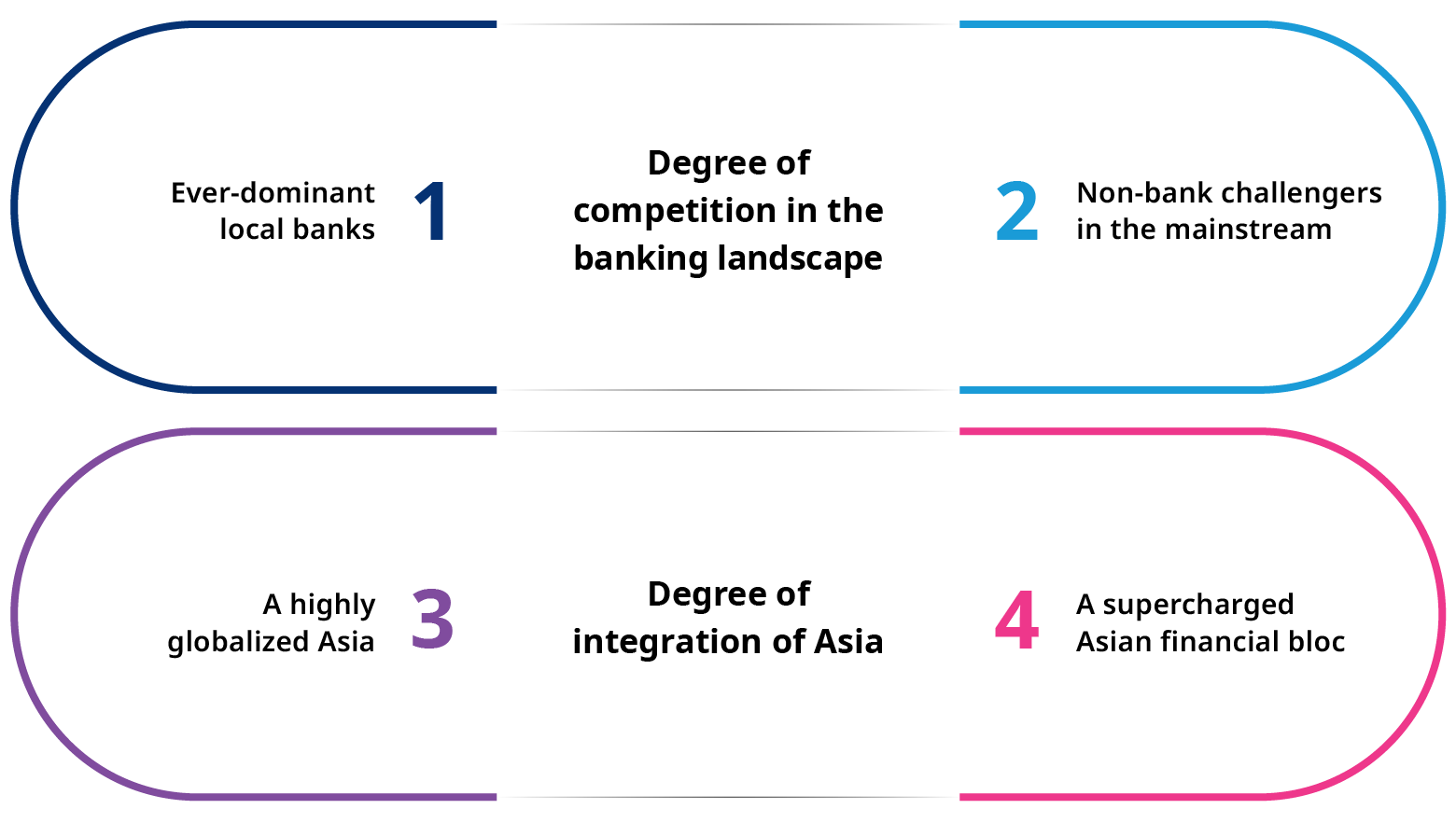

This report examines the ways Asia's future financial landscape might be reshaped. We see four distinct scenarios unfolding, each with its own set of implications: local banks triumph as global banks pivot; non-banks ascend in the region; Asia remains highly global, with the US dollar and global capital remaining crucial; or a supercharged Asian bloc takes shape.

What a New Monetary Order will look like in Asia

The Asia experience of Low for Long was different from that of the United States and Europe. The effect was more nuanced, and it did not produce the paradigm shift observed elsewhere. The same is true of the region’s recent rate hike and inflation experience.

However, there are still knock-on effects for Asia, given global financial and economic linkages. Domestic champion (tier 1) banks in each country have further expanded their dominant positions. Their balance sheet and funding structures are largely unchanged, and they have not needed to materially shift their strategy. Foreign banks and neo-challenger banks are still trying to chip away, with varying degrees of success. They have the capabilities to gain a share but need a differentiated strategy.

The role of the Japanese financial institutions in terms of providing external financing to the region or making direct acquisitions, especially in the Association of Southeast Asian Nations (ASEAN), has flown under the radar and is one to study for foreign players looking to make inroads. Japan’s slow reversal of its zero-interest-rate policy means the country’s financial institutions and intraregional capital flow will remain a strong influence on how the New Monetary Order plays out in Asia.

Non-bank financial institutions (NBFIs) are slowly growing their market share, but from a low base. There is ample opportunity to expand into underserved segments. Foreign banks could also reposition to focus on NBFI opportunities where they have significant experience. Legacy domestic banks will need to stay alert to the challenges and find ways to participate in any material NBFI opportunities.

The tension between globalization and regionalization will grow in Asia as part of a New Monetary Order. Higher interest rates or tighter regulation in the rest of the world could trigger capital outflows from the region or spur global banks to refocus strategies on their home markets. In their place, Japanese capital and regional financial institutions would play a more dominant role. Chinese financial institutions will also grow in regional importance.

Finally, the rise of a multipolar currency region including the USD is increasingly likely, especially in ASEAN given tight linkages and maturing intra-regional payments infrastructure. The RMB will play a leading role in this shift, as the country is now the biggest trading partner for most Asian countries. Higher Chinese capital outflows, if Chinese policy settings allow, would only accelerate the RMB’s regional rise. Together, these shifts will boost Hong Kong’s role as a global RMB hub and as China’s valve for managing the currency’s internationalization.

This report evaluates diverse scenarios shaping Asia's future financial landscape. In short, our findings unveil the region's potential path along a single or combination of these scenarios: ever-dominant local banks, non-bank challengers in the mainstream, a highly globalized Asia, and a supercharged Asian financial bloc.

How the New Monetary Order will play out across financial institutions

A grand experiment in global financial markets is playing out as central banks around the world establish a New Monetary Order that looks very different from the era that preceded it. Asia is both central to the conversation and separate from it in important ways.

For financial services firms, there will be winners, losers, and wildcards no matter which scenario prevails. Financial institutions should look for early signs of a tipping point in policy rate differentials, regulatory trends, and geopolitics and pivot accordingly.

Asia’s financial journey through the New Monetary Order is still to be determined, but many of the forces that will shape its course are already coming into view. Now is the time for leaders to navigate.