The wealth industry is on the cusp of the next evolution towards wealth management 3.0, offering attractive growth opportunities and the ability to make financial advice and investments more accessible to a broader demographic and range of clients.

In our 2022 Morgan Stanley and Oliver Wyman Global Wealth and Asset Management report, Time to Evolve, we explore the opportunities and priorities for wealth and asset managers as the industry shifts towards wealth management 3.0.

The report explores three pressing strategic and investment priorities for wealth and asset managers to successfully evolve to wealth management 3.0, and we also share our global industry analysis, trends, and insights.

Why wealth managers must evolve their growth strategy

For over a decade, many wealth managers have focused on the ultra-high-net-worth (UHNW) and higher-net-worth (HNW) segments, thereby not prioritizing less wealthy clients. Only players with a premium brand or strong investment banking capabilities have been able to profitably grow in the highest wealth band segments, as the UHNW market is both hard to scale and highly competitive.

We see a revenue pool of approximately $230 billion in the lower HNW and affluent segments, which wealth managers can now tap in a profitable way.

How modular digital models enable wealth management 3.0

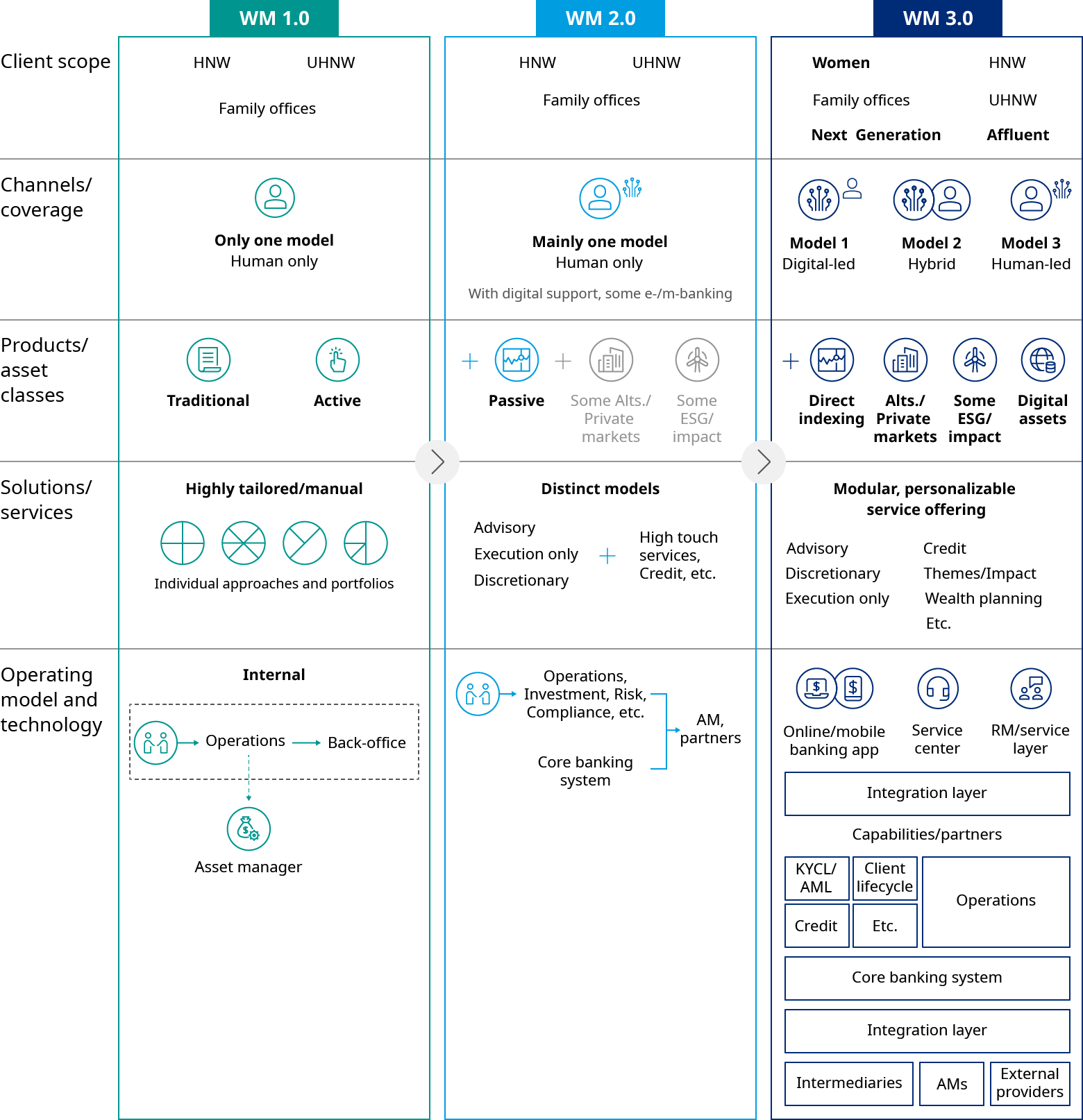

We believe the next decade will be about wealth management 3.0 — the transformation to a scalable and modular wealth management proposition, enabled by digital transformation. Facilitated by technology, wealth managers can make superior financial advice and investments accessible to a more diverse client base at lower, differentiated costs to serve.

Clients can pick and choose different modules of advice, products, and services to create their own personalized solutions. Wealth managers will support their clients along the journey through different channels, from human- to digital-led. Digital solutions will also form the base layer to cater to more traditional, higher-wealth clients, who increasingly expect enhanced digital experiences alongside traditional, human-led, bespoke service offerings.

For many wealth managers, this will require significant change and investment in their coverage and service models as well as operating models and technology in order to win market share profitably in the future. Leading firms that are accelerating the transition to wealth management 3.0 have been investing a high single-digit percentage of their revenues in this transformation effort and are planning to continue to do so for the next three to five years.

Why asset managers must rethink their distribution model

For asset managers , the wealth management channel becomes ever more important. We expect the share of the wealth and retail client segment of total assets under management (AUM) to grow from 58% to 64% in the next five years.

As wealth managers transform their service and delivery models, asset managers will need to evolve their distribution approaches. Asset managers face fundamental choices: partner and distribute through wealth managers, build captive digital-led wealth management distribution solutions, or establish open platforms geared towards this segment. A combination thereof may also work for some. Each model comes with benefits and drawbacks, but they all require re-architecting the wealth channel and associated operating model.

The interaction and distribution models between wealth and asset managers will require deeper technical integration and more personalized end-client experiences. Success will increasingly become a function of how effectively asset managers can forge partnerships with wealth managers through building integrated operating models and better end-investor experiences.

Tailored market insights, data and analytics, and better access to investments through digital-and human-led channels and portals will enable advisors to deliver value to their clients across the full lifecycle.

Market forces accelerating the move to wealth management 3.0

Advancements in technology, combined with a shifting macroeconomic and geopolitical environment, are accelerating the transformation of the wealth and asset management industry toward Wealth Management 3.0.

Market conditions are increasingly uncertain. After a decade of strong asset class performance, 2022 marked a more challenging environment, with slower and more volatile returns expected—approximately 4% to 5% CAGR over the next five years.

Inflation and geopolitical risks are rising. Sustained inflation, tighter liquidity, and the Russia–Ukraine conflict are heightening the risk of slower economic growth and driving greater geopolitical tension and deglobalization.

This regime shift is intensifying complexity, margin pressure, and cost challenges, pushing firms to rethink their service and operating models. At the same time, client expectations are evolving rapidly toward ESG offerings, private markets, digital assets, greater personalization, and seamless digital hybrid experiences. As a result, technology will play an increasingly critical role in enabling the next stage of industry transformation.

How wealth management 3.0 will transform service delivery and operations

We see wealth management 3.0 as the next stage of evolution triggered by the paradigm and regime shifts outlined within the report. Over the last couple of decades, wealth managers have successfully moved to more digitalized, data- and IT-driven models (“wealth management 2.0”) from their bricks and mortar, paper-based, white-glove only origins (“wealth management 1.0”).

The next stage will be defined by substantial modularization and diversification of offerings, service models, and operating models, allowing lower, more differentiated costs to serve — all facilitated by technology.

Wealth managers have been facing revenue margin pressure in recent years. This has been driven by a mix of factors, including deposit margin contraction (although some institutions have introduced countermeasures such as negative interest rates), pressure on mandate margins, and a change in client mix towards UHNW, as well as continued change in product mix towards cheaper passive products.

Rapid AUM growth coupled with tactical efforts to realize productivity increases allowed large wealth managers to succeed in maintaining cost-income levels. Pressure on smaller firms and booking centers has grown significantly, leading to increased consolidation and footprint rationalization, particularly in Europe, where the lack of a real banking union still hinders a fully integrated operating and funding model across markets.

Considering the cyclical headwinds and structural changes outlined above, we foresee that profit pools of wealth managers are under threat unless there is a fundamental transformation of service and operating models.

Global wealth growth slows amid rising geopolitical risks

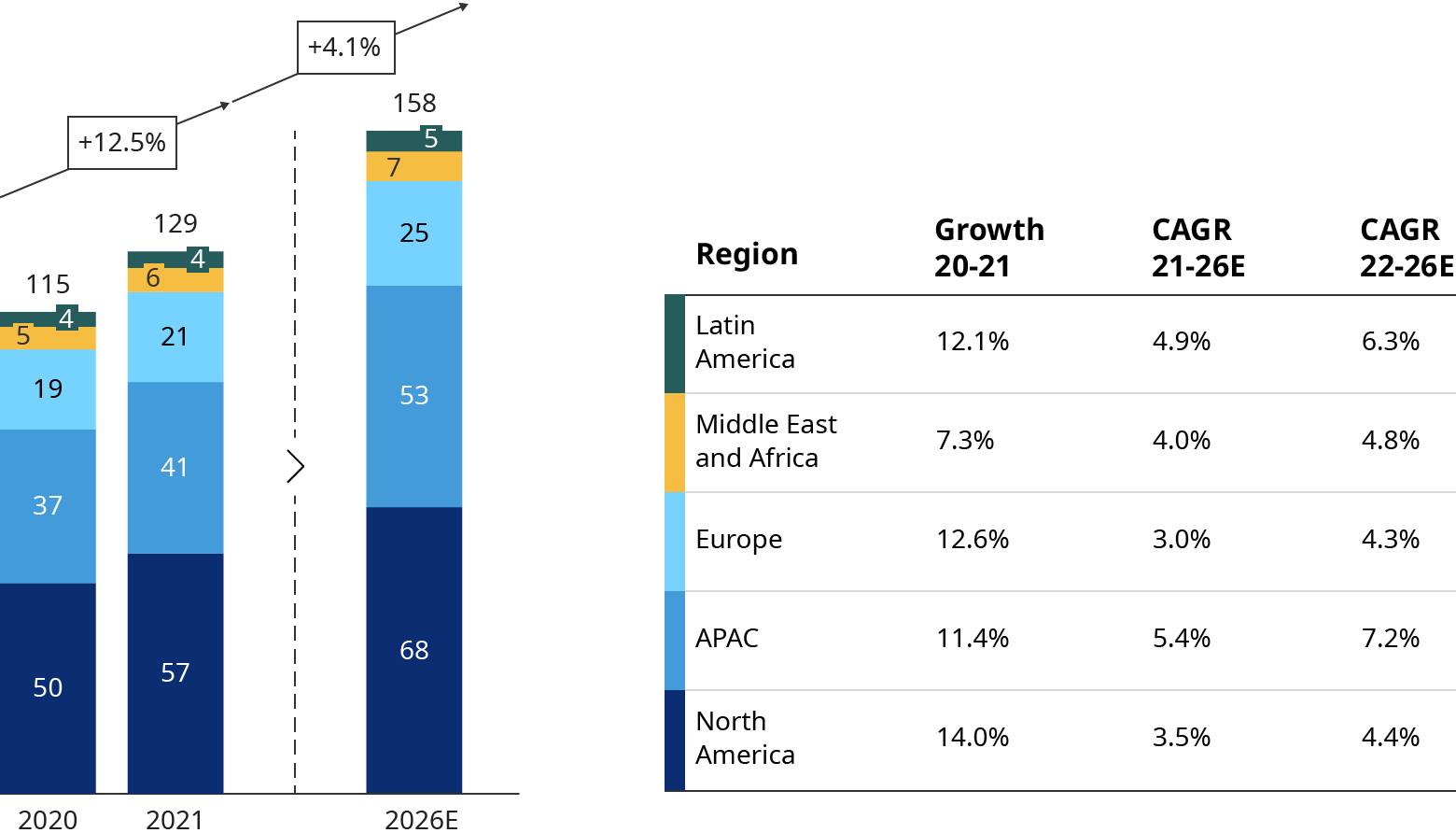

Heightened geopolitical tensions, inflation, and uncertainty regarding economic growth will negatively affect global AUM growth in 2022, where we expect a slight decrease in personal financial wealth for the first time in over a decade.

We expect growth to be around 4% per annum over the next five years through 2026, materially slower than the 8% seen in the last five years (2016-2021). While Asia-Pacific and North America look set to drive roughly 80% of worldwide new wealth creation until 2026, the growth differential between regions is narrowing.

Over the past decade, the primary focus of internationally oriented wealth managers was on higher wealth band clients, as they drove the majority of AUM growth and, given their oftentimes institutional needs, provided the opportunity for larger bank-owned wealth managers to foster cross-divisional revenue opportunities with their corporate and investment banks. Many wealth managers struggled to profitably serve lower wealth band clients given uniformly high costs to serve, and consequently they managed cost-income ratios by offboarding and restricting the access of these clients.

We expect UHNW investors with more than $50 million in wealth to continue to drive wealth creation and to account for more than 40% of total wealth growth by 2026. However, this segment accounts for less than 15% of the overall potential wealth management revenue pool and for less than 20% of its growth.

Broader banking revenues linked to the UHNW segments, such as from investment banking, will likely also come under more pressure due to deleveraging, slowed deal activity, and potential reduction in banks’ risk appetite. This growth will also come with higher uncertainty and risks compared to the last decade, where, for example, European collateral could finance a transaction in the US for a Chinese client. Nevertheless, UHNW will remain a core segment for global wealth managers.

Wealth managers should focus on these three priorities to drive growth

The largest revenue growth opportunity will be in the affluent and low HNW client segments with more than $300,000 and less than $5 million in wealth. This segment looks set to create approximately $45 billion of new revenues and account for about 60% of the total wealth management revenue pool by 2026. Currently, we see a revenue pool of approximately $230 billion in this segment, of which only 15% to 20% is penetrated by wealth managers.

We see three priority investment areas for wealth managers to accelerate their transition:

- Coverage and service model: Introduce full omnichannel capabilities that combine human-led, hybrid, and digital-led interaction models to serve clients more effectively across different needs and preferences.

- Delivery model: Make delivery more flexible and reduce the cost to serve by transforming operating models and technology, lowering costs from $8,000 to $20,000 per client in traditional human-led premium propositions to $2,000 to $8,000 in hybrid models and $500 to $2,000 in digital-led models.

- Value management: Create transparency on client-level economics and implement a systematic approach to measure, manage, and communicate value creation using digital dashboards and real-time information. This will enable dynamic management of revenues, costs, and profitability at the product, advisor, and client level.

Three strategic priorities asset managers must address in wealth management 3.0

Wealth management 3.0 will be defined by the substantial modularization and diversification of offerings, service models, and operating models that allow for lower, more differentiated costs to serve — all facilitated by technology.

As the wealth channel becomes more dominant and wealth managers transform their service and delivery models, asset managers need to rethink their positioning with wealth managers and ultimately the end clients. We expect a significant shift in the way they interact, from a simple intermediated distribution between an asset manager’s wholesale team and the wealth manager’s fund selection team towards a deeper technical integration. This will support delivery of more customized content, products, and solutions, enabling a more personalized end-client experience at lower costs. We also expect a few asset managers will create their own end-to-end wealth ecosystem with direct captive or open digital investment and wealth management platforms.

Despite the opportunity for direct distribution models, we expect intermediated channels via wealth managers to dominate. A strategic priority of asset managers will be refining the interface with wealth managers and adapting their operating models accordingly.

We see three emerging themes that asset managers need to address to succeed:

- Increased importance of integration and customized content: In selecting asset managers, wealth managers will place increased weight on the ability to build technical integrations with their own operations to streamline content delivery and facilitate development of customized products and outcome-oriented solutions.

- Technological adoption and sophistication as drivers of economics: Technological capabilities are becoming more important than pure scale as a driver of operational efficiency, allowing smaller players to compete more effectively against scale players.

- Supercharging advisors and clients: As end-clients in wealth management 3.0 need more (digital) guidance on a broad suite of products and a higher-quality digital customer experience, asset managers must develop the (digital) content capabilities that truly elevate their advisor partnership.

Wealth Management 3.0 is reshaping the industry, and firms that modernize now will be best positioned to capture the next wave of growth.