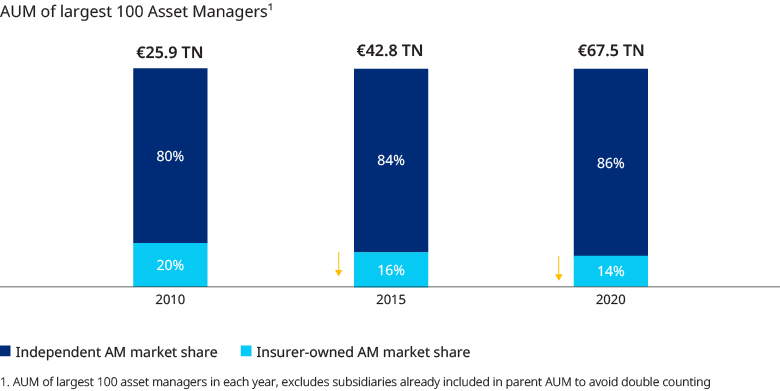

Life Insurance businesses have transformed in recent years, with steady movement away from capital-heavy, guaranteed products and fully vertically integrated business models to unit-linked products and open architecture platforms working through independent advisers. However, their asset management business models by and large haven’t adapted. Insurer-controlled asset managers historically have been significant players – a decade ago insurance asset managers represented over 20% of investment industry assets under management (AuM), but this share has fallen continuously and is now only 14%.

Without significant change to business models, we expect this slide to be accelerated by a combination of heightened commercial pressure on the asset manager, continuing low yields impacting insurers’ own asset allocation, continued dismantling of the vertically integrated business models which previously guaranteed distribution access, and therefore the need to compete in the open architecture space.

Overcoming these pressures requires insurance asset managers to refocus their business models to leverage specific advantages of expertise or client access. In this paper we examine new archetypes in insurer-owned asset managers that seek to optimize capital efficiency and third-party business growth in combination with improved operational effectiveness.