The 2022 edition of our annual report with Morgan Stanley offers insights into the next cycle for the wholesale banking industry.

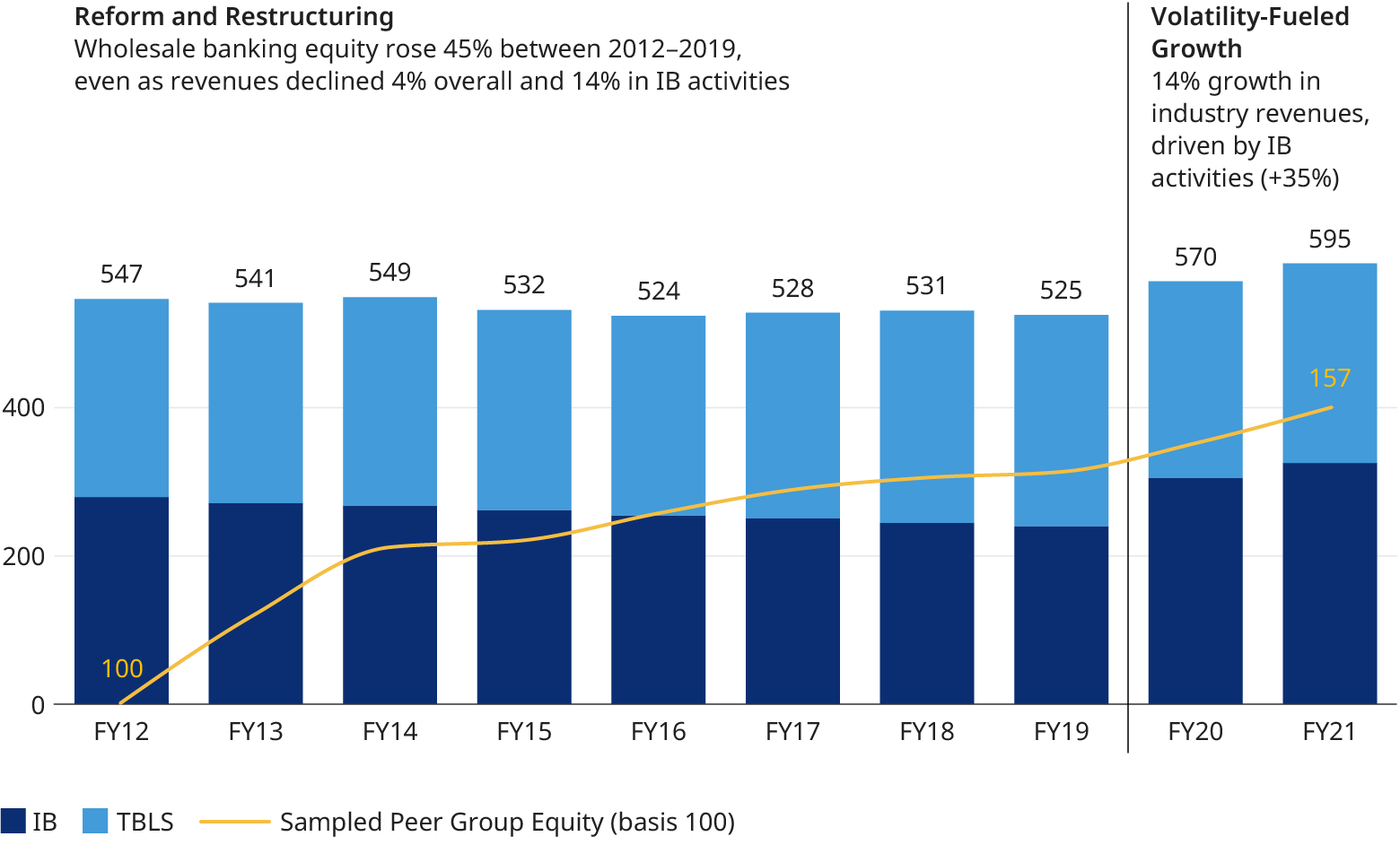

The wholesale banking industry has passed through two cycles over the past decade: reform and restructuring from 2012-2019 and volatility-fueled growth from 2020-2021. The fundamental question facing the industry now is what the next cycle will hold.

Wholesale banks face great uncertainty as we head into 2022, but we see more cause for optimism than concern.

1. IB (Investment Banking), TBLS (Transaction Banking, Lending, Security Services). 2. Basis 100 industry equity with growth modeled on an index consisting of publicly reported figures from the following peer group: J.P. Morgan, Goldman Sachs, Bank of America, Morgan Stanley, Barclays, UBS, Societe Generale, BNP Paribas, Deutsche, CACIB, HSBC and Credit Suisse.

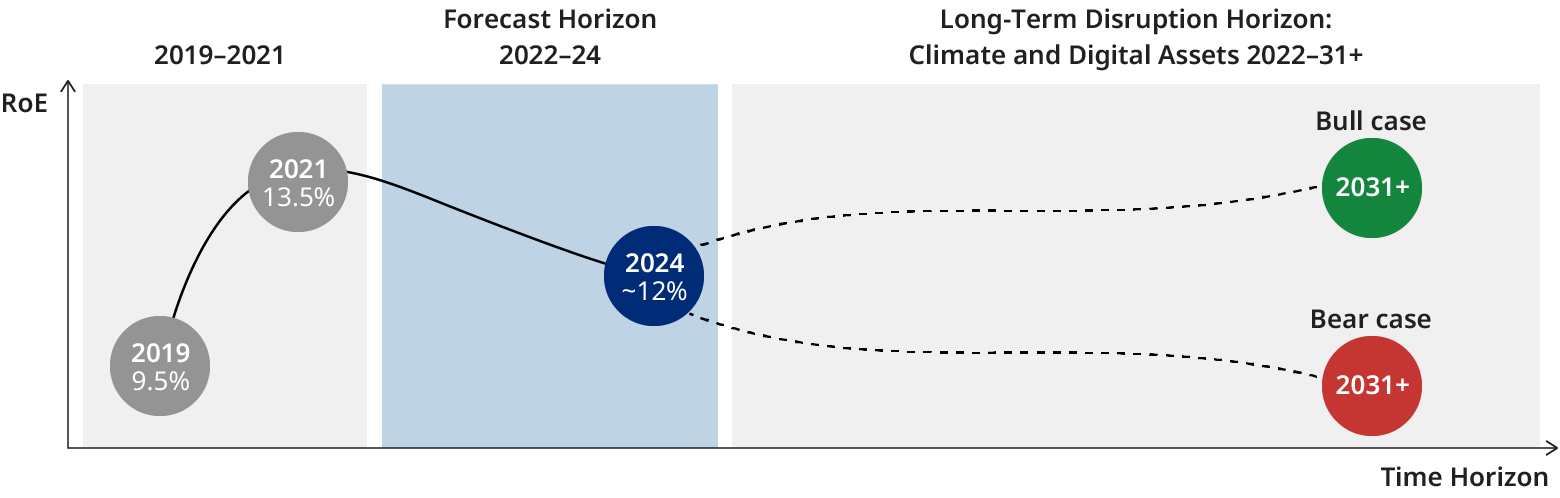

Reform and restructuring fundamentally transformed the business model for wholesale banks, improving resilience by shifting key revenue drivers from risk warehousing to client activity. Volatility-fueled growth generated an industrywide windfall, pushing revenues to nearly $600 billion (versus $524 billion in 2019) and restoring healthy returns to 14% (versus 9.5% in 2019).

With storm clouds on the horizon driven by geopolitical and economic disruptions, the key question facing the industry now is what the next cycle will hold.

- Will industry revenues revert to 2012-2019 levels in the next cycle or remain elevated?

- Which market shifts will drive growth in the next cycle? Which are resilient to geopolitical and economic pressures?

- Will banks capitalize on or be disrupted by the climate transition and digital assets adoption?

- Have banks adapted to perform in a broader set of market conditions, including escalating geopolitical pressures?

- What will define the leaders and laggard in the next cycle: business model or execution?

Six active and emerging market shifts support a robust revenue outlook that should comfortably exceed 2019 levels in all our scenarios: corporate demand, rates normalization, private markets demand, macro volatility, commodities volatility, and the China onshore opportunity. We estimate the cumulative revenue impact is $70 billion over the 2019 baseline.

And the industry is far more resilient to market shocks following the reform and restructuring cycle. This was successfully tested at the onset of the pandemic in 2020. What has not been tested is the success of wholesale banks’ efforts to build more agile, scalable, and efficient technology and operating models that will drive performance in all market conditions.

The climate transition

The climate transition will disrupt many of the industries that wholesale banks serve, but the industry has the expertise and client franchise required to support the transition of these industries to net zero while building new “green” revenue streams in decarbonization finance, carbon trading, etc. With no or little action to evolve the existing business model, a meaningful share of this revenue could disappear or shift to banks (or non-bank competitors) with more active approaches to the transition. However, we see credible signs that wholesale banks are repositioning their business model to defend existing revenue pools and build new streams in decarbonization finance, carbon trading, etc.

The digital assets revolution

The digital assets revolution may launch a new asset class and disrupt legacy businesses, but the industry has the expertise and the model to transform cryptocurrencies into an investable asset class for corporate and institutional clients (and potentially shift to more efficient technology and operations in their core business lines). The rapidly growing market has been dominated by firms outside the traditional banking industry thus far and there is a risk that this market continues to evolve and expand with wholesale banks on the sidelines. However, we believe the fundamental driver of adoption of digital assets by corporate and institutional clients will be the introduction of more clarity in regulation, which will be of advantage to banks that already operate in highly regulated markets. This will provide an opportunity to catch up just as the market hits an inflection point.

The next cycle should create opportunity for wholesale banks to grow revenues and sustain returns well above the 2012-2019 lows.

There is more at stake than revenues alone - wholesale banks that can successfully reshape their business around new opportunities will have a powerful narrative for investors, clients, and employees. Execution, even more than business model, will increasingly define the winners and losers. The winners will be defined more by their vision and discipline in execution than business model, home market advantage, and other factors that mattered more in previous cycles.