This article was first published on June 4, 2020.

Oliver Wyman has collaborated with Corridor Platforms to bring our readers a COVID-19 crisis management paper "Credit Decisioning Agility And Governance."

Corridor Platforms is a leading decision workflow governance and automation capability designed by industry veterans to rapidly transform risk and marketing decisioning at banks, enabling them to leverage new data, AI and automation to create competitive excellence in revenue growth, risk control and operating efficiency in the age of digitization.

Below is an excerpt from our paper. For the full PDF version of "Credit Decisioning Agility And Governance," please click here.

COVID-19 has severely impacted the consumer lending industry, with much uncertainty around what is yet to come. The global economy and unemployment rate have changed so fast and in such unprecedented ways that the past is no longer a reliable predictor of the future.

As customers face extreme financial difficulties — asking for payment holidays and forbearances — banks are making decisions and planning actions that will have a potentially severe and lasting impact on their institution’s financial health and share price. Underwriting and credit standards will likely be tightened across the customer base, leading to long-term regulatory, growth and profitability challenges.

The extreme extent of impact to customers from the pandemic has created irrevocable change, and the past is no longer a good predictor of the future

Today’s challenges also present new opportunities. Our paper helps banks act now and develop a foundation for competitive excellence — today and post-crisis.

For the last decade, digitalization has been an important driver of transformational change. In the midst of the pandemic, it is an immediate imperative.

In our paper, Oliver Wyman and Corridor Platforms have collaborated to explore how a well-designed decisioning platform can provide a bank with adaptability and speed, robust governance and controls, and enhanced monitoring capabilities. Such a platform enables the seamless integration of new data, analytics, and strategy across the customer life cycle.

Additionally, we evaluate how a platform utilizing open APIs allows firms to realize returns on investment in technology, analytics, and talent by leveraging existing systems as quickly as possible. Finally, we pose examples of the “must haves” required to start this journey, providing the means to allow institutions to transform their decisioning capabilities in a matter of months rather than years.

Banks who invest now will create a competitive advantage to not only aid in navigating the crisis, but to succeed and grow as we emerge from the pandemic

THE TIME IS NOW TO BUILD BACK BETTER

Given the unique nature of this crisis and the potential for multiple waves, a constant adjustment of segments, strategies and actions may be required — especially as new information and performance data loops back. Current business as usual bank governance, legacy technology and processes are often not geared to move this quickly. It is a critical time for banks to design and implement sustainable, adaptive risk management

approaches, which will not only enable well-planned actions to control risk and maximize profitability, but also to serve customers and the broader public

THE ROAD AHEAD: WHAT’S NEEDED TO TRANSFORM RISK AND DECISIONING

There are three capabilities that banks need:

1. ACCELERATED DECISIONING LIFE CYCLES (CLICK HERE)

The extreme extent of impact to customers from the pandemic has created irrevocable change, and the past is no longer a good predictor of the future. The future credit environment is uncertain, and traditional models based on historical delinquencies, unemployment rate, or gross domestic product (GDP) will not be enough.

However, a crisis is a good time to learn, compress timelines and drive innovation. The good news is that the capabilities needed to successfully maneuver through the pandemic are highly overlapping with those driving digital transformation. Investing in and building capabilities now will set banks up for long-term success.

In today’s environment, a well-designed integrated decisioning platform offers banks the connective tissue to effectively navigate the crisis and beyond. Deploying innovation at start-up speed is achievable due to newer plug and play automation capabilities that can enhance legacy technology within an 8-12 week period.

The advantage

By accelerating decisioning life cycles, banks can incorporate new sources of data and variables; create new, actionable customer segments; frequently recalibrate predictive models and scores; and rapidly test and implement new credit strategies.

This helps banks to achieve organizational agility without increased risk, but requires banks to create the proper connective tissue between all key stakeholders and processes. Doing so properly is critical as it provides the foundation to leverage real-time information flow for rapid decision making and seamless promotion to production.

2. ROBUST GOVERNANCE AND DECISION TRACEABILITY (CLICK HERE)

New internal and external data such as the as the epidemiological intensity of COVID-19 (which could be regional), unemployment metrics (which can be industry-based), and customer requests (whether a customer asks for forbearance or not) are now relevant in decisioning strategies. But incorporating this data needs special care. Banks need to ensure that permissible purpose and fair lending regulations are top of mind as well as retaining brand and customer loyalty.

Compliance considerations should be identified and addressed upfront, with experts defining appropriate ways to use new data and being included in the design of various customer segments and action strategies. Banks should create upfront transparency on compliance metrics, so the first-line has clear rules right from the start.

Creating the new business rules and segments requires that the team evaluate the impact of various scenarios quickly, including volumes, losses, profitability, and operational readiness. As new data and models are deployed, retaining readily accessible, accurate and centralized records of data, model versioning and credit decisions made in production will be critical. There must be a process for the post approval changes to be implemented into production quickly. The last recession left a long tail of legal implications for banks, and the ability to demonstrate adherence to compliance guidelines post-hoc for legal and regulatory purposes will be imperative.

3. DYNAMIC MODEL PERFORMANCE AND PORTFOLIO MONITORING (CLICK HERE)

The COVID-19 pandemic has unfolded with weekly (and at times daily) shifts in epidemiological outcomes, lockdown patterns, government response, and business closures. These shifts in turn have driven unprecedented changes in customer behavior that must be addressed by financial institutions. To keep up with this crisis, banks must create new segments, models, and business rules to quickly evaluate the impact of various scenarios and understand expected volumes, losses, and profitability.

Centralized, real-time monitoring enables decision makers and experts to better identify and manage risks associated with models and business strategies, allowing for the continuous improvement of the segmentation and analytics underlying critical decisions.

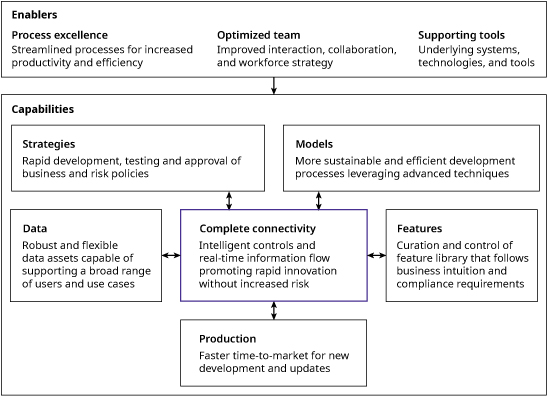

WHY AN INTEGRATED DECISIONING PLATFORM?

The underlying challenges described in our paper are largely not about revising individual models tailored to market conditions in isolation, but rather about how to transform the surrounding processes and technologies required to fully leverage those models. Every step of the analytics life cycle relies on the collaboration of several functions, including information technology,data management, decision sciences, and business owners. Additionally, each step is subject to inspection and approval by a range of stakeholders, including model risk management, compliance, and regulators.

Integrating a well-designed decisioning platform provides the benefits of cutting-edge analytics with the adaptability and speed of leading digital players. The platform can seamlessly integrate analytics and strategy across the customer life cycle

Achieving organizational agility in this environment requires carefully designing each step of the analytics life cycle to encourage experimentation and innovation within a well-controlled and efficient environment. In particular, the proper identification, design, and implementation of consistent processes, procedures, and tools can critically drive:

• Efficiency: Eliminate costly and time-consuming replication of work, miscommunication, or rework due to inconsistent application of standards.

• Modularity and consistency: Facilitate the reuse and recombination of existing elements in new models/strategies.

• Governance: Implement well-designed control points to allow for explicit oversight and the staged sign off for elements with specified purposes.

• Traceability: Data, features, and models can be traced from inception to deployment, with clear versioning and visibility into upstream linkages and downstream dependencies.

Looking across the analytics life cycle, many banks are at different places in the journey to achieve the connectivity and efficiency that allows this kind of growth. Prior to the pandemic, banks had started to invest in a wide range of vendor and in-house point solutions to solve pieces of the puzzle, but these cannot be effective without robust end-to-end connectivity and governance.

Achieving organizational agility through connectivity

THE PATH FORWARD

Institutions must enhance capabilities to ensure faster adaptation and reactivity to market changes, robust governance and controls, and enhanced model and portfolio monitoring.

A well-designed integrated decisioning platform offers banks the connective tissue — to effectively navigate the crisis and beyond. It allows banks to provide end-to-end process owners an unmatched level of transparency and control over their processes.

Using an accelerated decisioning platform, banks can compliantly incorporate new and alternate sources of data; migrate to faster machine learning models and big data; and make decision and strategy changes quickly to react to the economy, competition, and consumer needs. These are exactly the capabilities needed to act with speed and agility to get through the crisis.

Finally, the journey to achieve this agility does not need to be long or arduous. By providing the right connective tissue and information flow between existing point solutions and infrastructure, the journey may be months rather than years, paving the way for improved customer acquisition, satisfaction, and value — throughout the crisis and beyond.