Customer remediation is an absolute priority for Australian financial institutions to meet community expectations and address the many findings from recent reviews and regulatory enquiries.

Remediation, including errors in process and policy application and the need to make things right, is far from a new concept. What is new is the sheer scale and complexity of ‘remediation incidents’, and the present wave of issues is unlike anything the sector has seen before. This wave has followed various regulator enquiries into financial advice and insurance, and the Royal Commission into misconduct in the Banking, Superannuation and Financial Services Industry, which exposed material issues affecting millions of customers.

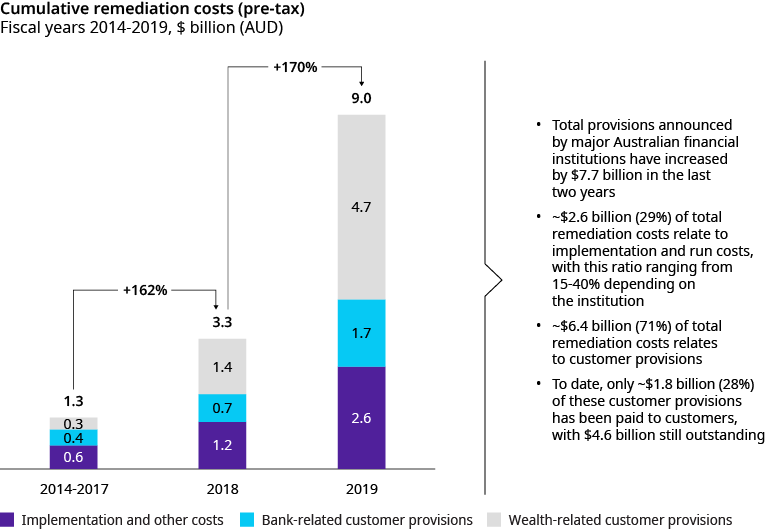

The result has been a dramatic increase in the size of customer remediation provisions in the sector. This figure has jumped from AUD $1.3 billion in 2017 to AUD $9 billion in 2019 (see Exhibit 1). The nature of these incidents has also expanded, from targeted issues in wealth management to a broad range of banking products and services. Remediation teams and programs are now expected to rectify a greater range of incidents, both in terms of size and complexity.

To restore trust and respond to the increasing demands of regulators, it is essential that Australia’s financial institutions establish and run remediation programs that meet defined customer outcomes as efficiently as possible

CUMULATIVE REMEDIATION COSTS OF MAJOR AUSTRALIAN FINANCIAL INSTITUTIONS

Notes: OW estimates given varying level of disclosure, and what is included in ‘remediation’ costs. Includes remediation costs for the largest Australian financial institutions. Includes discontinued operations.

Source: Company announcements, Oliver Wyman analysis

Remediation presents a substantial cost burden for institutions and brings fresh reputation risk. The exposure of incidents requiring such broad and deep remediation has furthered a loss of consumer trust in the sector, with a quarter of customers saying they do not trust financial institutions or advisers1. To restore this trust and respond to the increasing demands of regulators, it is essential that Australia’s financial institutions establish and run remediation programs that meet defined customer outcomes as efficiently as possible.

The challenge for financial institutions

The response to date by Australian companies has largely focused on recruiting remediation staff. Company reporting suggests major Australian financial institutions have over 4,400 employees working on remediation activities between them. However, this recruitment drive hasn’t always been accompanied by top-down strategic program planning, and while more staff will undoubtedly help deal with remediation issues, it is unlikely to act as a silver bullet.

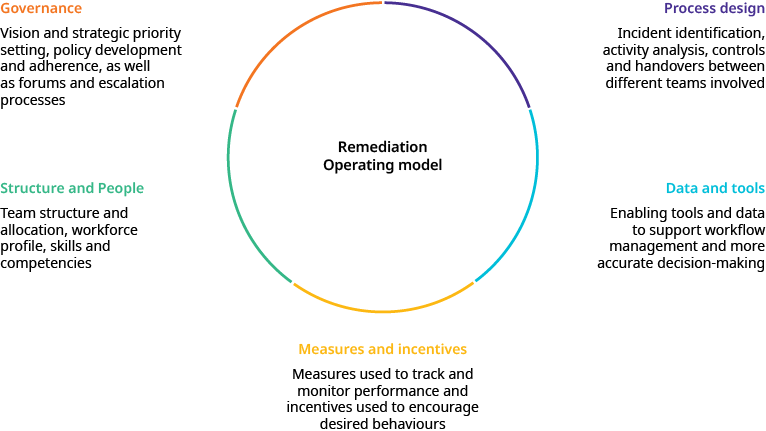

In our view, financial institutions should take a long-term view of their remediation programs across five key dimensions: governance, structure and people, process design, data and tools, and measures and incentives.

1 According to Dr Chris Culnane, Associate Professor Andrew Godwin, Professor Carsten Murawski and Cynthia Sear, University of Melbourne in their paper Improving the Finance Sector for all Australians

CUSTOMER REMEDIATION MATURITY MODEL

Source: Oliver Wyman analysis

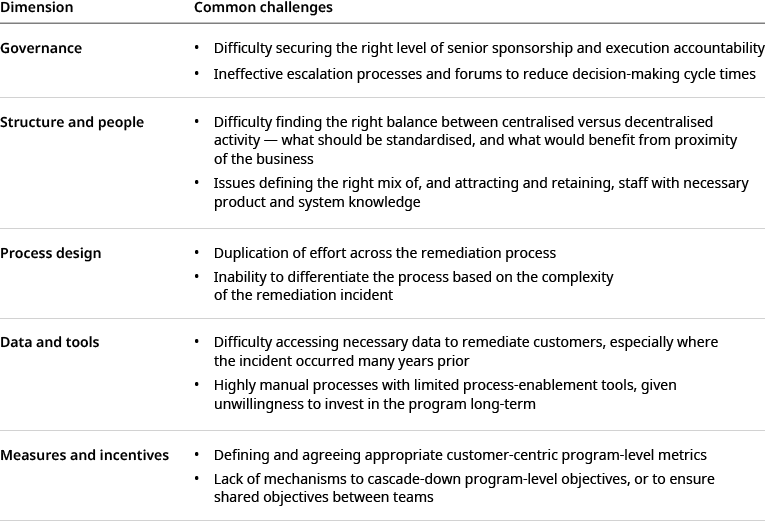

As a starting point, companies can look overseas to guide their thinking on common challenges across these dimensions. Banks in the United States and United Kingdom have been dealing with even larger scale remediation incidents, in some cases for over seven years. For example, it is estimated that since 2012, UK banks have incurred remediation costs of £48.5 billion for complexities associated with payment protection insurance (PPI) alone. 2 Based on our experience globally and in Australia, we have identified a set of challenges institutions tend to face in the early stages of their remediation program.

2 Jones, R. ‘The end of a scandal: banks near a final release from their PPI liabilities’. The Guardian, 24 August 2019.

These challenges impact how effectively remediation program(s) meet customer outcomes, mitigate risks, and the overall cost and speed of dealing with incidents.

Options to respond

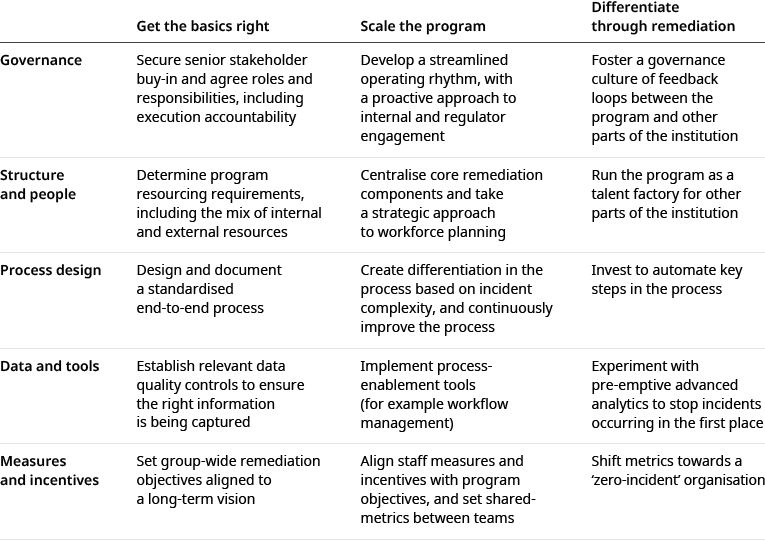

In response to these challenges, we recommend an iterative approach. Necessary thought must be applied to developing foundations before scaling and achieving a market-leading program. Remediation programs will look different within every institution – the volume of incidents, as well as their characteristics, will differ based on the company’s size, products and services, processes, systems, people, and location. That said, we believe there are three common steps to establishing and running an effective remediation program: getting the basics right, scaling the program, and differentiating through remediation.

Get the basics right

Effective remediation programs are constructed on strong foundations. This means that senior remediation staff must be vigilant in the early stages of the program preparation, as issues in setup will worsen as the program scales. In practice, this means securing senior focus on remediation, structuring, and planning to resource the program effectively, defining a robust remediation process, setting up data foundations, and agreeing program objectives. For example, one UK bank agreed to prioritise the remediation of incidents based on the financial detriment suffered by customers, while also considering the number of customers impacted, and the level of regulator focus. Getting these basics right is crucial in ensuring that the program can deal with an influx of incidents as institutions get better at identifying them.

Scale the program

Once the foundations are set, program operators need to consider implementing measures that ensure the program can be successful in the medium to long term. Necessary steps include setting up a proactive governance model, centralising elements of the program that benefit from standardisation and decentralising those that require fluid interaction with the business, differentiating and improving the process, implementing appropriate process-enablement tools, and cascading program-objectives down to teams and staff. For example, a number of overseas banks have set up central remediation teams, with a shared pool of data analysts, a team responsible for governance and reporting, and teams focused on specific types of remediations, such as legacy issues or incidents impacting large numbers of customers.

Differentiate through remediation

Once the remediation program is running efficiently, companies can look to use remediation for more than rectification of past mistakes. The program should shift from a reactive to a preventative mandate, acting as a differentiator actively creating value for customers and shareholders. One way to do this is to set up the program to attract and train up talent to be vigilant in spotting and preventing issues occurring. Other measures include establishing feedback loops, automating process steps, using pre-emptive analytics, and shifting towards metrics focused on preventing incidents from occurring. For example, one UK bank has set up a team within their centralised program to aggregate learnings from incidents they have remediated and integrate these learnings into product and service design forums.

CUSTOMER REMEDIATION PROGRAM EVOLUTION

Source: Oliver Wyman analysis

Conclusion

Australia’s financial institutions should accept that customer remediation programs are here to stay. Short-term fixes will fail to create long-term value and will ultimately lead to unsatisfactory outcomes. Rather than continue as is, the industry should embrace the opportunity to deliver positive customer outcomes and rebuild trust in the sector. With long-term focus and investment, Australia’s financial institutions can ensure not just that existing issues are dealt with effectively, but that in the future, such issues are far less likely to occur.