This article was first published on April 27, 2020.

Paycheck Protection Program - PPP

COVID-19 has taken an enormous human and economic toll on the world, and financial institutions globally are helping to implement government programs that have been designed to mitigate economic damage. In the United States, financial institutions have been rushing to implement the Paycheck Protection Program (PPP), a key provision within the Coronavirus Aid, Relief, and Economic Security (CARES Act), which provides fully guaranteed (and forgivable) loans to small businesses.

While the Paycheck Protection Program lending period expires June 30, 2020, and the funds may run out sooner, the pitfalls lenders face could lead to consequences for years to come. Our paper, Forgive But Don't Forget, offers immediate cross-functional recommendations while implementing the Paycheck Protection Program (PPP).

Lenders’ experiences from the global financial crisis should serve as a warning that good intentions are not enough, and the impact of any infractions can be expensive and long-lasting

Already, lenders are being accused of unfair practices in processing Paycheck Protection Program (PPP) loan applications and face a variety of risks:

- Lawsuits have been filed against the largest banks in the country, accusing them of prioritizing loans to larger businesses and existing lending clients.

- Lenders are processing loans differently from each other as well as changing their own practices repeatedly, partially driven by changes from the Treasury and Small Business Administration (SBA) — for example, one lender updated its application at least eight times in the first 12 days of the program.

With the second tranche of Paycheck Protection Program funding approved by Congress, the time for lenders to act is now to improve processing, minimize additional risk, and change public perception. The focus must include both refinements to new loan origination and front-running potential issues in loan forgiveness, servicing, and ultimately guarantee redemption.

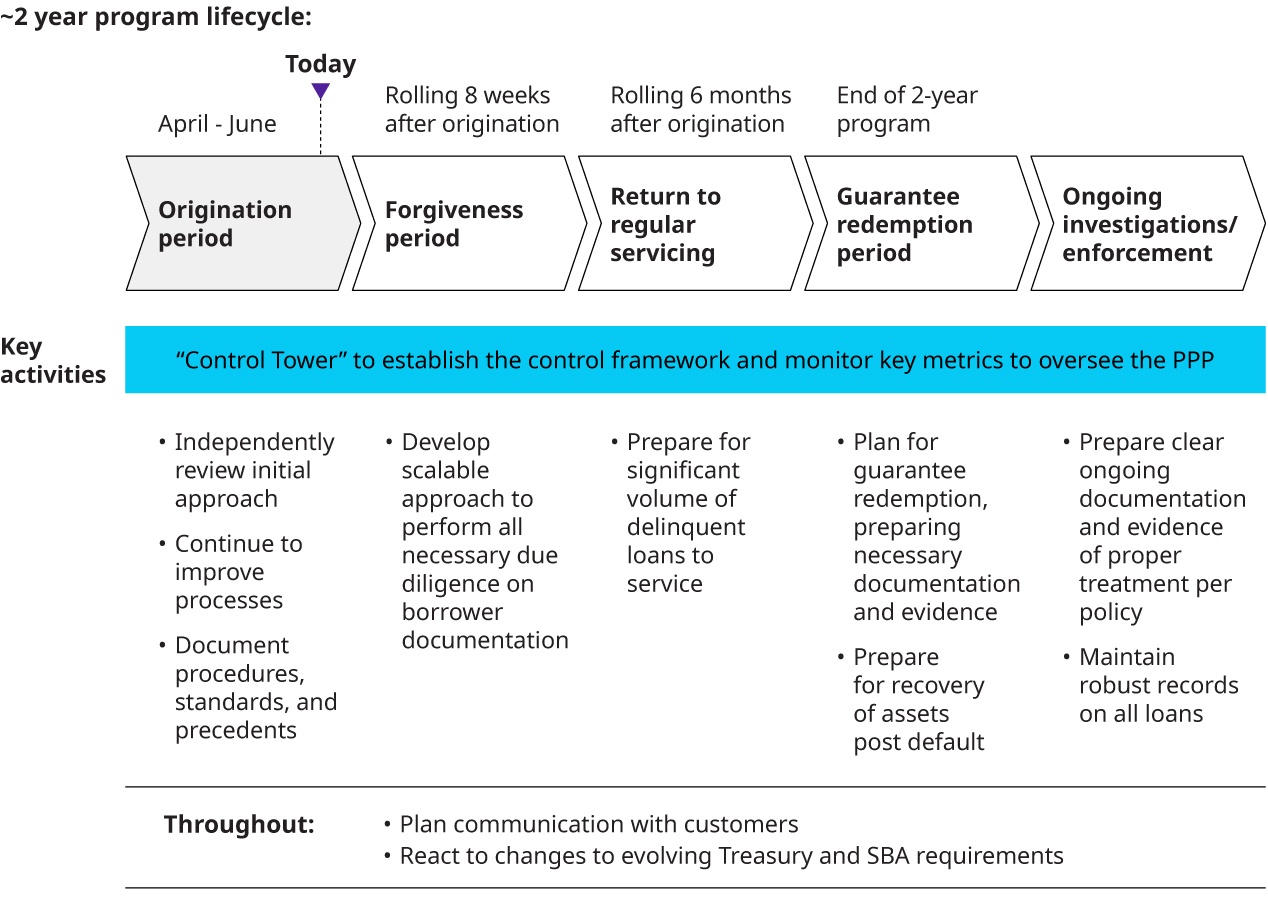

The primary focus of lenders so far has been on the origination period and getting borrowers’ loans processed and funded through the SBA. Lenders need to establish and maintain appropriate operational processes and controls throughout the loan’s life cycle. The following provides a summary of recommendations intended to help lenders implement the Paycheck Protection Program with robust and fair processes. For more detail, please view the paper's PDF version.

THE TIME TO ACT IS NOW.

While the first round of the Paycheck Protection Program funding has been exhausted, lenders have an opportunity to identify prior shortfalls, continuously improve origination in subsequent

round(s) of funding, and plan ahead for forgiveness, servicing, and loan disposition.

Key activities across the Paycheck Protection Program life cycle

Already we are seeing lenders experience reputational damage from their approach to the Paycheck Protection Program. The risks that are present in the remainder of the Paycheck Protection Program will require executive attention, institutional resources, and careful management. The time to act is now.