First, we take a look at climate change – a global problem that should now be classed as a financial risk for banks, and not just viewed through the lens of corporate social responsibility (CSR).

Next, we look at the risk artificial intelligence (AI) and machine learning poses financial institutions, finding that there is no time to waste in establishing an AI risk framework.

For asset managers and wholesale banks, meanwhile, our annual analysis found that both face falling margins and a challenging market environment over the next few years. To overcome this and achieve breakthrough growth, management teams need to lock-down their strategy for China as markets open up.

Finally, we take a look at the future of clearing, finding that despite increasing transparency and stability of financial markets since the financial crisis, there is still work to be done to maintain a robust financial markets ecosystem.

Managing Climate Change – A New Financial Risk For Banks

Climate change is a global problem, and an increasing financial risk banks need to be aware of too.

The bankruptcy of the major Californian utility PG&E, dubbed “the first climate-change bankruptcy” by The Wall Street Journal, is a recent example of how much there is to lose by not getting it right. The French supervisor, ACPR, published a report on April 10 2019 to highlight the issue of climate change for banks and insurers.

With the growing recognition of the financial stakes, rising external pressures, and upcoming regulations, how should banks – and specifically their risk management teams – manage climate risks?

Historically, banks have approached climate change through the lens of Corporate Social Responsibility (CSR). With increasingly high financial stakes, growing external pressures, and new regulations, a pure CSR approach is no longer sufficient. Climate change has become a financial risk for banks and needs to be treated as such.

Our paper, Climate Change: Managing a New Financial Risk, provides industry perspectives from a climate risk awareness survey we conducted in partnership with the International Association of Credit Portfolio Managers (IACPM) across 45 global financial institutions.

It presents how institutions can integrate climate considerations and opportunities into their financial risk management frameworks, before providing guidance on implementing the Financial Stability Board’s Task Force on Climate-related Financial Disclosures (TCFD) recommendations.

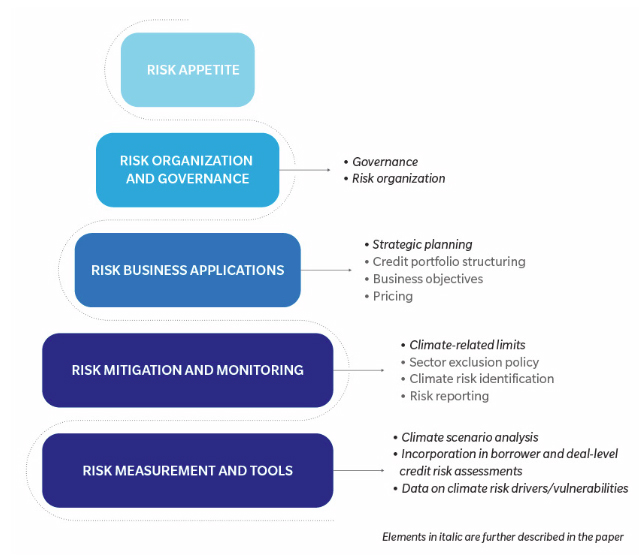

To effectively manage climate risks and protect banks from its potential impact, institutions need to integrate climate risk into their financial risk management frameworks, as shown in the exhibit below.

Exhibit: Risk Management Framework And Integration Considerations

Why Banks Need To Prepare For AI Risk Now

Whilst being prepared for the threat of climate change risk, banks should also be mindful of the threat – and not just the opportunity – artificial intelligence (AI) and machine learning poses to their institutions.

The advantages are clear: AI allows institutions to serve their customers better through tailored product recommendations, seamless customer on-boarding and support, near-instant underwriting and pricing decisions, secure identity verification and real-time fraud detection.

But with the benefits comes risk. The risk is created via the deployment of AI applications (“AI risk”) which does not wholly fit into any existing risk bucket. Instead, AI risk is a composite risk that cuts across multiple aspects of non-financial risk.

For example, an AI application can create technology risk, cyber risk, information security risk, model risk, compliance and legal risk, third party vendor risk, and many other types of risks (e.g., fraud risk) depending on the specific use case and application. Because of this complex and composite nature, AI risk currently does not have a clearly designated second line owner at most financial institutions. Roles and responsibilities across the different second line functions are also typically not articulated to holistically govern the risk. This creates gaps in governance and oversight.

To help navigate this issue, our article on AI risk outlines six steps that can be taken to ensure it is appropriately managed at an institution, finding that establishing an AI risk framework as soon as possible is vital. In taking action against AI risk, there is no time to waste.

Asset Managers And Wholesale Banks Look East For Growth

Both wholesale banks and asset managers are under increasing investor pressure to accelerate growth while managing down costs – yet face falling margins and a challenging market environment, according to our annual analysis.

The report forecasts that over the next five years total asset management industry revenues will grow at just ~1%. Three growth zones – emerging market clients, private markets and solutions – will drive this, growing from 38% of the fee pool to 53% by 2023.

For wholesale banks, by mid-2018 there was a growing optimism that they had weathered the worst, with expected revenue growth of 3%. But the revenue outlook weakened and 2019 started slowly. As a result, the report predicts industry wide revenues will grow at only ~1% by 2021, delivering only modest improvements in returns on equity (RoEs).

To negate these low forecasts and achieve growth, management teams in both industries are advised to decide their strategy in China as markets open up. The growing pool of externally managed assets under management (AUM) is highlighted as an opportunity for foreign asset managers, and over the long term can also drive an expansion of the investor wallet for wholesale banks.

In the battle to adapt and leverage new technologies, established firms with the capital to reinvest as well as new entrants are looking to quickly outcompete slow-moving incumbents. They will do this by leveraging data advantage in providing new client solutions. Meanwhile, investment is ramping up in both industries meaning that incremental and 'greenfield' builds should be considered to accelerate growth.

The Future Of Clearing: Maintaining A Robust Markets Ecosystem

Our joint report with the World Federation of Exchanges (WFE) on the future of clearing has found that despite increasing transparency and stability of financial markets since the financial crisis, there is still work to be done to maintain a robust financial markets ecosystem.

Commitments to increase transparency and promote stability of financial markets, made and reiterated at 2009 and 2011 G20 summits, were carried forward by International standard setting bodies (FSB, IOSCO, CPMI and BCBS. This was done with the introduction of a series of policies, regulations, standards, and frameworks aimed at promoting the use of central clearing and enhancing the resilience of CCPs.

The report argues that strong progress has been made in meeting G20 objectives, with a significant shift to central clearing of OTC derivatives and ongoing investment by CCPs in their risk management and core processes while bolstering financial resources. But there is still work to be done for supervisors, CCPs and clearing members.

Supervisors should finalize the central clearing agenda and implement the clearing obligations, addressing a range of factors that may impede the use of clearing services. For CCPs, the focus remains on core risk management capabilities (credit, liquidity, operational risks and default management), and exploring ways in which to further enhance the accessibility of clearing.

Exhibit: Overview Of Some Of The Post-Crisis Regulatory Reforms Impacting CCPs And Their Stakeholders