This article first appeard in BRINK on January 24, 2018.

Despite relatively good conditions for the financial services industry in 2017, many executives are expressing a gnawing sense of concern that the structural advantages of their businesses are eroding, raising questions about where future growth will come from.

In particular, there is a perception within the industry that more new customer value is being generated in other industries than in financial services and that big tech companies in particular will be entering the industry in force in the coming years.

The State of the Financial Services Industry 2018 report by Oliver Wyman confirms these concerns, finding that traditional financial services firms will need to accelerate customer value creation or risk conceding an increasing share of customer attention and wallets to other firms, primarily to those big technology firms.

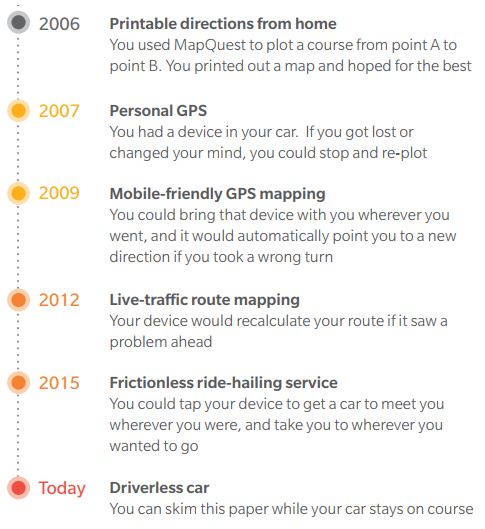

To show how quickly technology evolves, just consider the advances that have been made in how we find physical destinations in the last decade while the financial services industry was recovering from crisis:

Back in 2006, which would you have considered more likely in 10 years: 1. Help plotting a secure financial future with daily advice to achieve this goal, or 2. A car that drives itself? And which of those would you have thought to be more valuable to most consumers? For most, financial direction is far more valuable than the driverless car. Someone is going to build a version of Google Maps for financial lives with potentially revolutionary implications. Maybe it will be Google, Amazon or Alibaba. Maybe it will be JPMorgan Chase, BBVA, or MetLife. But it is going to happen.

In the 10-year period since the financial crisis, the financial services industry has come from the brink of disaster toward relative health. In the same 10-year period, a group of spectacularly successful technology firms has gone from being seen as irrelevant to financial services to a point where they are considered behemoths whose threat to core financial services is contained largely by the hope that they do not want to be regulated.

Financial services firms can learn a lot from big tech about how to close the value gap

We believe that this is outdated analysis—we do not think the growing regulatory headwinds they face will dramatically alter their momentum. Financial services players urgently need to consider how these firms are creating new value for customers and driving growth, both of which are fundamental challenges for the financial services industry today.

It is not that the financial services industry needs more innovation, but it needs to harness innovation toward creating better customer outcomes at the risk of self-disruption and, in some areas, the risk of short-term loss of shareholder value. And it needs to do so quickly or continue to watch underlying growth and relative value shift elsewhere in the economy.

Many firms in financial services already use the terminology “customer value.” However, it most often refers to the amount of value generated for shareholders by delivering products to the customer. We think this is the root of the problem. Financial services firms must begin to quantify the other side of this exchange as well: How much value are financial services solutions delivering to customers? How is that evolving over time? How does it compare to other solutions in the market? And how could new value be created to improve the exchange and stimulate new shareholder value in the future?

Many people are willing to pay in exchange for value for help to solve their problems with an experience that makes their lives better. But there is a big customer-value gap today, and it is unclear who is going to close that gap and reap the rewards. As this year’s Oliver Wyman report demonstrates, financial services firms can learn a lot from big tech about how to close the value gap and show how innovation can be oriented toward better customer solutions. It’s time for financial services to learn and react or continue to watch value shift to other parts of the economy.