This report is a joint product of the International Banking Federation and Oliver Wyman.

With the increasing role of digital interactions in all our lives, consumers have an overwhelming need to provide reliable and trusted digital proofs of their identity. Such is the strength of this demand that it will inevitably have to be fulfilled in the next few years.

In this report we describe how action is being taken to meet this need, either by the public sector or by private companies. The report highlights how banks’ involvement can ensure digital identity schemes are more trustworthy, secure, and convenient. The report also examines the key decisions for banks, and for other stakeholders including banking federations, policymakers, and regulators.

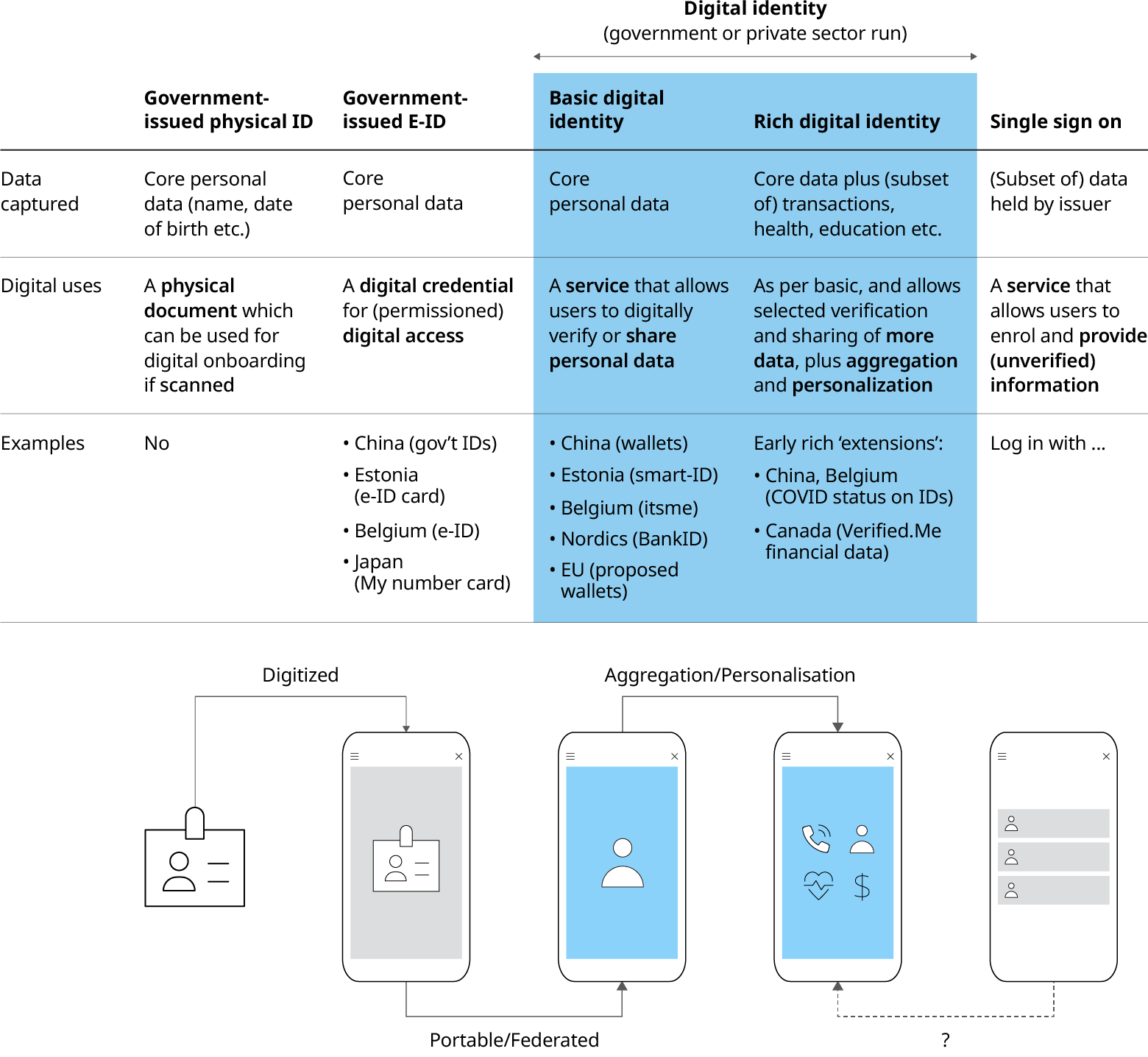

There is a spectrum of approaches to digital identity. Physical identity credentials can be used in digitized processes. Some governments now issue digitized ‘e-ID’ identity credentials, which citizens can use to verify their identity. Digital identity is then a single, integrated identity relationship allowing a citizen to verify their identity for access to many services or products provided by third parties. In time, a rich digital identity will enable users to bind securely a wider set of personal data.

Many of the national schemes not led by governments are led by banks. The report highlights how banks’ involvement can ensure digital identity schemes are more trustworthy, secure, and convenient. Banks operate in a highly regulated environment which requires strict AML procedures and significant safeguards for personal data protection. As a result, they are well placed to facilitate digital identity schemes.

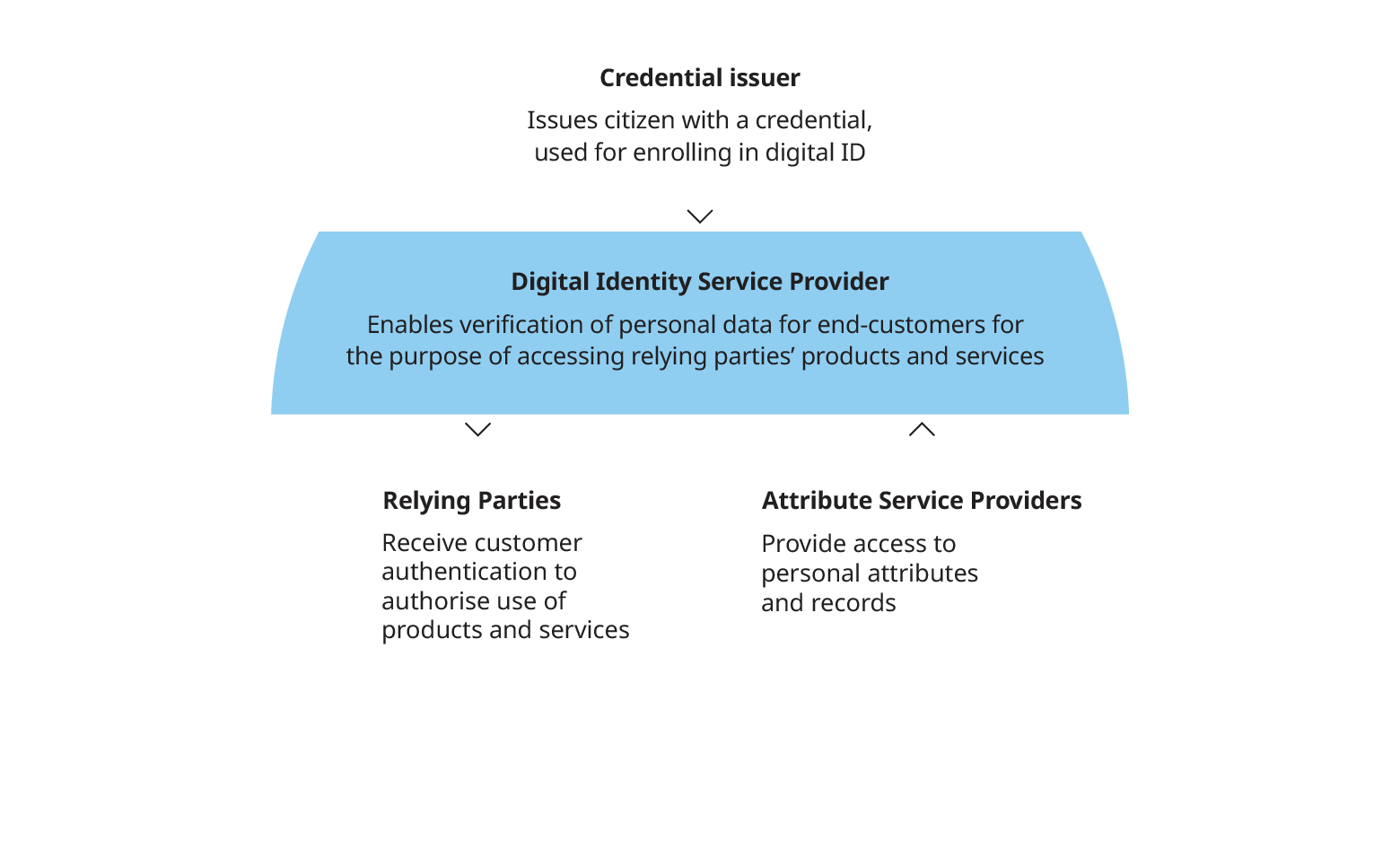

The key decision for banks is around what part to play in the evolving digital identity ecosystem. We see three choices for banks - accept digital identity as a relying party, provide data as an attribute service provider, or become a digital identity service provider (potentially in collaboration with other banks). Participation offers multiple benefits, including lower operating expenses and reduced fraud risk exposure, enhanced customer perception and loyalty and new potential revenue streams. We examine each of these roles and their associated business case in the report.

The implications of the shift towards digital identity will be far-reaching and the extent of this is only being fully realized now. If done well, digital identity will ensure that all interactions are made easier and more secure, increasing citizens’ confidence online and trust in the banks’ role in their life.