This piece was first published on May 8, 2020.

It is no secret that the current COVID-19 pandemic has had far-reaching impacts on businesses, consumers, and society at large. While many sectors have been hit hard, others such as the United States grocery industry have experienced a surge in sales amid the crisis.

For these essential retailers, the month of March was “like the lead-up to Thanksgiving or Christmas”. Bank of America reported that card spend on groceries was up 36 percent in March year-over-year.

However, this has required a significant increase in costs, as grocers have needed to spend more on labor and transportation as well as stepped-up store hygiene measures and personal protective equipment in order to keep shelves stocked and shoppers and employees safe.

Now the question on everyone’s mind is: how is the topline likely to develop from here on? For now, the gains in sales have been enough to cover the increased costs. But are these sales sustainable or will they disappear? Worse, is there a trough just around the corner that will offset the recent spike in sales as consumers begin to draw down their pantries?

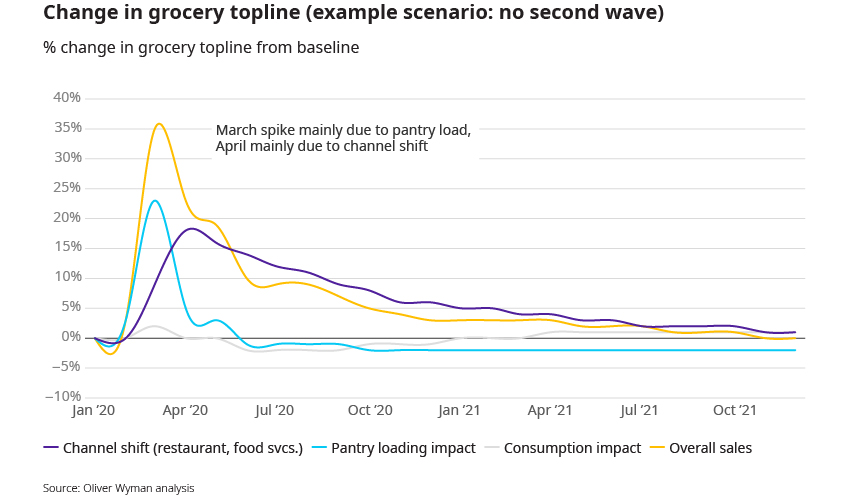

To answer these questions, Oliver Wyman has developed an in-house model to understand and forecast COVID-19 impacts on grocery topline over the next 18 months as the pandemic and its economic repercussions unfold.

MODELING COVID IMPACTS ON GROCERY

We have taken a bottom-up approach to modeling, forecasting monthly sales by grocery department, and leveraging best-in-class market research and reports to continuously validate our results.

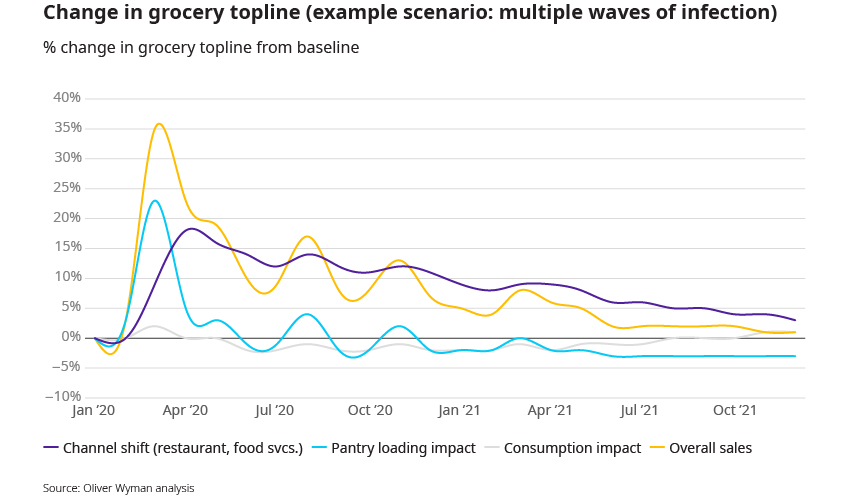

For flexibility in this volatile environment, we incorporate multiple scenarios including a quicker-than-expected return to normal and second wave outbreaks to stress test the impact on food retailer top lines.

- At the heart of the model are three main impact drivers from the pandemic:

- Channel shift from restaurants and food service

- Pantry loading (change in home inventories)

- Changes in consumption behavior

CHANNEL SHIFT FROM RESTAURANT AND FOOD SERVICES

Widespread stay at home orders have curtailed spending on food away from home. Bars and restaurants, for example, are closed for dine-in across most of the country. OpenTable reported bookings were down 100 percent YOY by mid-March in every country where the company does business, as consumers chose to stay away. Other sources of shifted meal occasions include company cafeterias, college/K12 cafeterias, airline meals, and even hotel room service.

While some food service industry volume has been retained through shifts to drive-in, takeout, and delivery, much of it has in fact moved over to grocery. Increased time at home has made cooking more feasible.

Eating at home is also more attractive to consumers looking to tighten their purse strings, given it usually presents a more affordable option than eating out. According to Investment Zen, the average cost of a meal is $4 at home versus $13 at a restaurant. To put this in perspective, if the entire US restaurant industry volume shifted over, this would result in around $185 billion of uplift to grocery.

As states around the country begin to ease lockdown restrictions, some volume may flow back. But some of it is likely to stay with grocers. A CBS News poll found 71 percent of respondents said they would still not feel comfortable going out to a bar or restaurant even if stay-at-home restrictions were lifted. As the recession settles in and unemployment numbers continue to rise, many may not be able to afford to, and as restaurants close their doors permanently, supply will contract.

PANTRY LOADING

Last month, headlines swirled all over the news about people hoarding toilet paper leading to widespread shortages. NCSolutions, a data and consulting firm, reported that sales of toilet paper were up 845 percent on March 11 and 12 as states began announcing lockdowns.

Similar, albeit less extreme, effects were noticed across several grocery departments, including cleaning and disinfectant products, shelf-stable packaged foods, bottled water, and medications.

While there is some consensus that most of the consumer stockpiling has already happened, there is still much speculation around when and to what degree consumers will begin unloading their pantries.

We expect this release to be slow in playing out. Consumers are likely to maintain elevated levels of pantry inventory as insurance against future waves of infection requiring additional lockdowns or stay-at-home orders. The pandemic will leave lasting scars on generational psyches — just as those who came of age during the Great Depression scrimped and saved for the rest of their lives, this generation may always keep a month’s supply of toilet paper and pasta on-hand.

CHANGE IN CONSUMPTION BEHAVIOR

During the lockdown, underlying consumption patterns are also changing, as daily patterns are upended, in turn impacting purchases in retail channels. Beauty products, for instance, are reporting sales declines during the lockdown period as consumers continue social distancing.

Alcohol, on the other hand, is seeing higher consumption, at least in the US. According to Wine and Spirit Wholesalers of America, surges in alcohol sales at US grocery stores and liquor stores have more than offset the decline in alcohol-related sales in bars and restaurants. Further, market research firm IWSR attributes those sales to increased consumption, as consumers are experiencing increased stress as a result of the pandemic. Let’s raise a glass in sympathy with all the stressed parents juggling work-from-home and homeschooling.

Finally, while in the panic-buying period availability trumped price, as time goes on the economic repercussions of the pandemic are having an impact on product mix. Consumers are shifting to private label, downtrading from premium products, and purchasing larger pack sizes, similar to what was seen during the 2008/2009 recession.

Our analysis suggests that these shifts in consumption, while less of a driver than channel shift and pantry loading overall, can make a big difference at the individual department level.

SO WHAT DOES THIS MEAN FOR THE GROCERY INDUSTRY OVERALL?

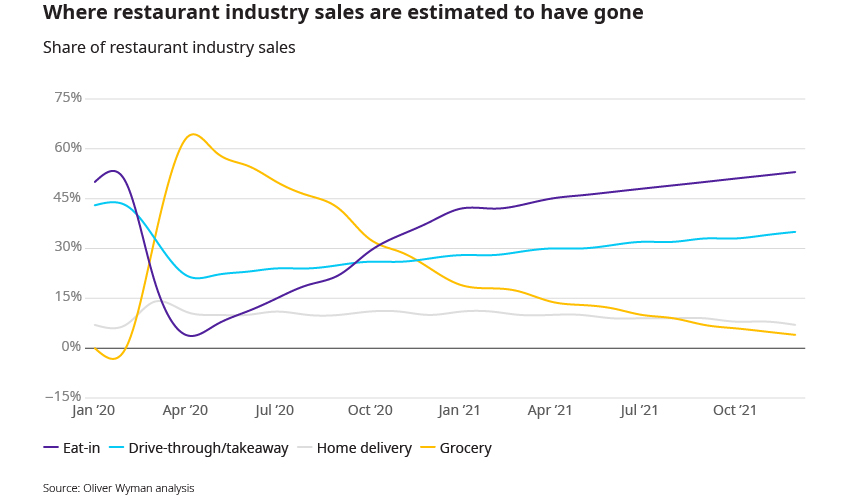

The COVID impacts on grocery topline has been (and will continue to be) an ever-evolving, month-by-month story. In March, the dominant effect was pantry loading, while in April it was the channel shift.

We find that the US grocery industry will continue to see a sales tailwind from COVID-19 over the coming months, though not nearly at the same levels of early surge. The shape of the curve will in large part depend on the success of containment measures in preventing subsequent waves of infection, how quickly consumers return to restaurant channels, and how quickly they draw down their pantries.

Some effects will persist long into the “new normal.” In a post COVID-19 world, consumers are likely to continue eating more at home, especially if they are cash-strapped and spending less on eating out. Consumers may also maintain elevated pantry levels for some time due to lingering fears of a secondary outbreak.

WHAT THIS MEANS FOR YOUR COMPANY

While the grocery industry is expected to benefit, the impact will be uneven at the individual retailer level.

The extent to which a grocer captures the shift in meal occasions will differ based on competitive positioning. Retailers with stronger e-commerce offerings and a better footprint of stores will capture an outsized share. Discount grocers, for example, will be better positioned than premium players during the recession. Further, companies that are able to forecast accurately, react quickly, and avoid out-of-stock will win customers over.

Perhaps most importantly, as we enter the “long suppression” phase of the pandemic, social distancing measures will be more local in their implementation, so the impact will depend more on your unique store footprint. Some areas will recover faster and others will need to enter subsequent rounds of “lockdown” after flare-ups in local infections. Oliver Wyman’s Pandemic Navigator tool includes forecasting at the county level which can help understand where and when future lockdowns are likely to be implemented.

All grocers are now doing their own internal modeling to forecast COVID-19 impacts on the business, but in many cases these models do not disaggregate the various impacts or allow businesses to anticipate a different impact in subsequent waves of lockdown (for example, if home inventory levels are already high, there will not be a similar “pantry load” in the lead-up). Oliver Wyman’s model can serve as a valuable sense-check to validate grocers’ own internal models and enable more proactive planning for what is now obvious will be a marathon, not a sprint.

As grocers start to build out topline modeling forecasts, one question remains. For the industry as a whole, and for individual grocers, will the (smaller) sustained boost to top-line be enough to offset the massive increase in costs?