And the centers’ increasing sophistication means that specialists can run them more effectively, eventually increasing their valuations. The divestment of data centers therefore represents an opportunity to strengthen telecom operator’s balance sheet.

As big tech companies achieve stellar market valuations in 2020, telecommunications operators have articulated strategies to become tech companies themselves. They want to be agile, enjoy global scale, and drive their development through software. They plan to standardize IT in the cloud, move to cloud-based 5G environments, and upgrade their global fixed networks to fiber. And to interact more effectively with their customers, telecoms companies increasingly use online – or at least online-enhanced – channels and target customer needs based on a vast pool of harvested data.

This is a good strategy framework, but it is not easy to implement. IT migration must be married with legacy systems, local regulations, and “not invented here” corporate cultures in a way that makes a business case. Getting the myriad of detail right requires significant investment and focus. We think this is easier to achieve without owning data centers.

Leave data centers to specialists

Data centers are one of the foundations of the ecosystem made up of telcos, IT and the cloud. However, telecom operators’ data center real estate can be a distraction from their core businesses – and the centers could be worth more carved out as separate units.

Some telcos will benefit from continuing to run data centers. These will be operators with a strong IT services business and the DNA and commitment to achieve long-term market success based on a global footprint, significant scale, and continued acquisitions. But most operators would be better off selling their data-center assets and investing more in their strategic transformations. There are five major interrelated reasons to do this:

1. Tectonic Shifts in Data-Center Technology

The data center industry is going through a number of technology disruptions that will alter – fundamentally and in unpredictable ways – the way tenants use them. These disruptions are now occurring on the data-center, cloud, and IT value chains. We think each has the potential to revolutionize how telecommunications companies work with data centers.

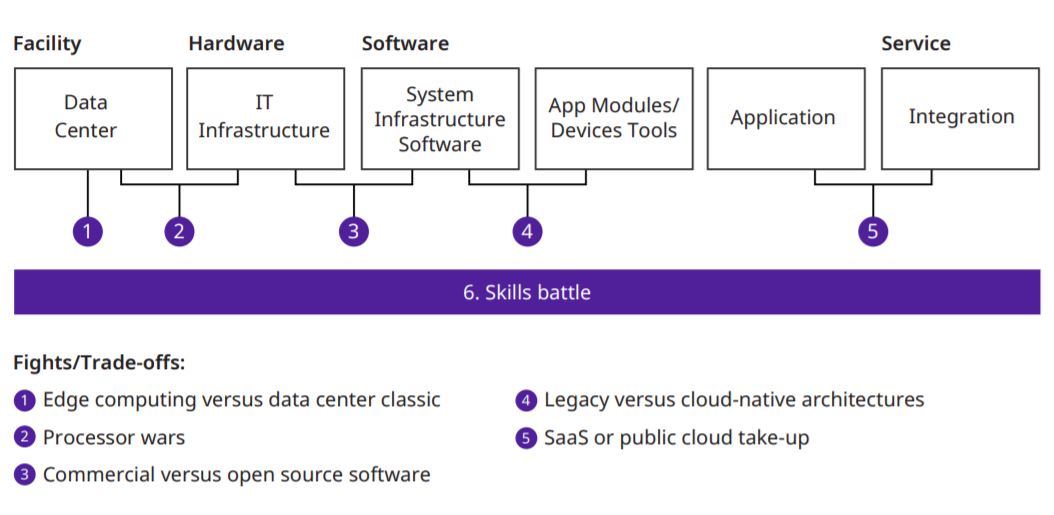

Exhibit 1: Cloud value chain and battlefields

Source: Oliver Wyman Analysis

There are six key technology shifts, shown by the red areas in Exhibit 1.

- Edge computing vs. DC classic: Computing and other workloads (for example, network-supporting IT and content delivery networks, or CDNs) will move to the edge – closer to the locations where they are needed. However, it is hard to predict when and to what extent this will happen.

- Processor wars: The outcome of the competition between ARM/Nvidia and x86 processors will help determine the most suitable hardware platform for a data center and the power footprint required.

- Commercial vs open source software: As software moves to open source, data centers must accommodate fewer specialized hardware solutions with a dedicated power footprint and cabling requirements.

- Legacy versus cloud-native architectures: As with open-source software, the shift from legacy to cloud-native application architectures will alter the connectivity and power requirements in data centers.

- SaaS or public cloud take-up: Enterprises that choose to use the public cloud or SaaS will have to run a far smaller share of IT infrastructure in their own perimeter.

- Skills battle: Telecom companies will often find it hard to attract the right skilled talent. Challenges include companies’ branding and the salaries and development opportunities they can offer.

Data centers are a critical yet non-core operation for telecoms companies. These technology disruptions create a high degree of unpredictability, and they need to be addressed by workers whose skill sets make them hard to hire, build, and retain.

2. Uncertain Telco Data-Center Needs

Given the ongoing restructuring of IT infrastructure and migration to the cloud, telecommunications companies have found it hard to forecast their data center needs, measured by the electric power or space required. In addition, the proliferation of partnerships with SaaS companies is pushing software outside the IT perimeter. Likewise, cloud-computing platform providers are taking on a significant amount of IT workloads. The resulting uncertainty over their future data-center needs means telcos require data-center capacity that is flexible. This is easier to acquire if they rent it when and where they need it instead of owning the infrastructure themselves.

3. Superior Operational Capabilities of Data Center Specialists

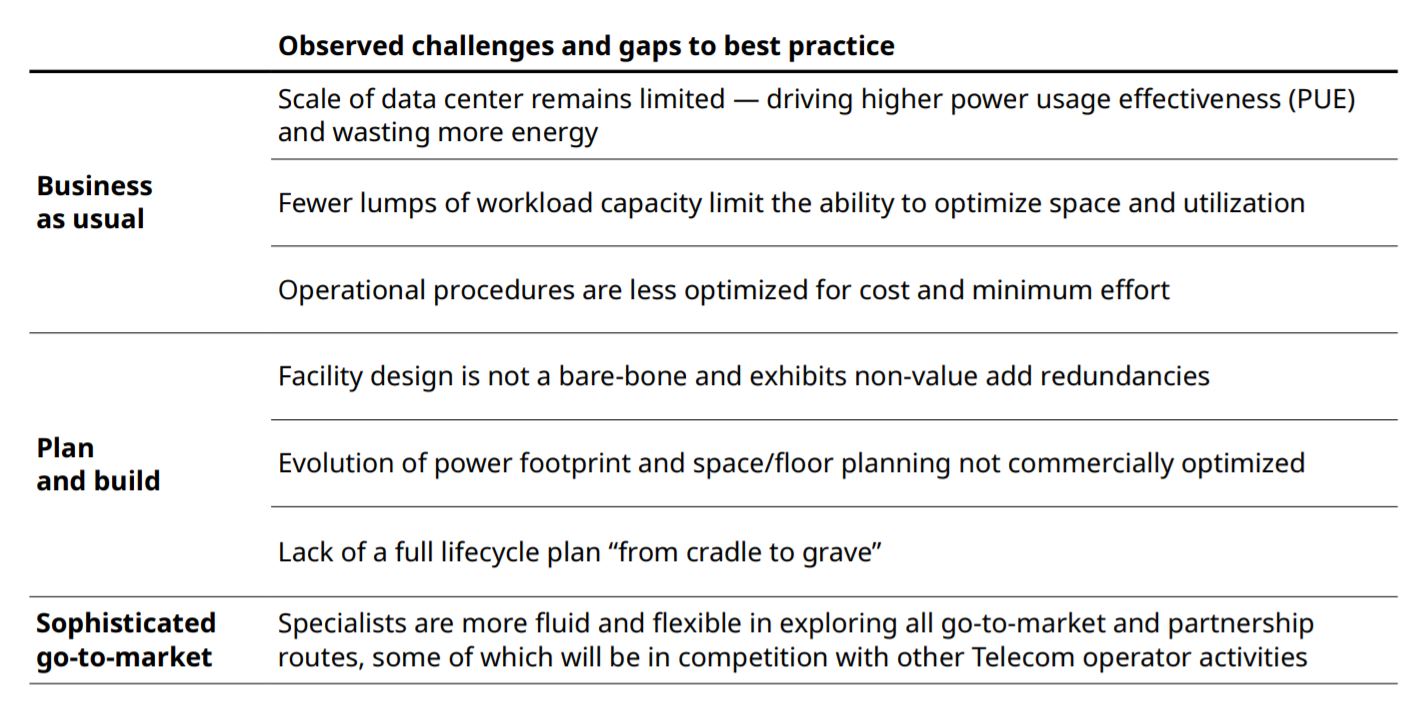

Technology disruption and the uncertainty of future needs imply that telecommunications companies are often going to be less effective at operating data centers than data-center specialists. For telecom operators, data centers are a non-core business, so they are unlikely to achieve either significant scale benefits or operational excellence.

The areas where operating efficiency can potentially be improved will vary according to the specific circumstances at each company. But our observations of telco-operated data centers suggest that at least some of the above challenges will apply in many cases. A telecom company with a dispersed business model will often not prioritize its data center. As a result, it will not achieve the same potential as a specialist with an unrelenting focus on efficiency.

4. Increasing Debt Burden

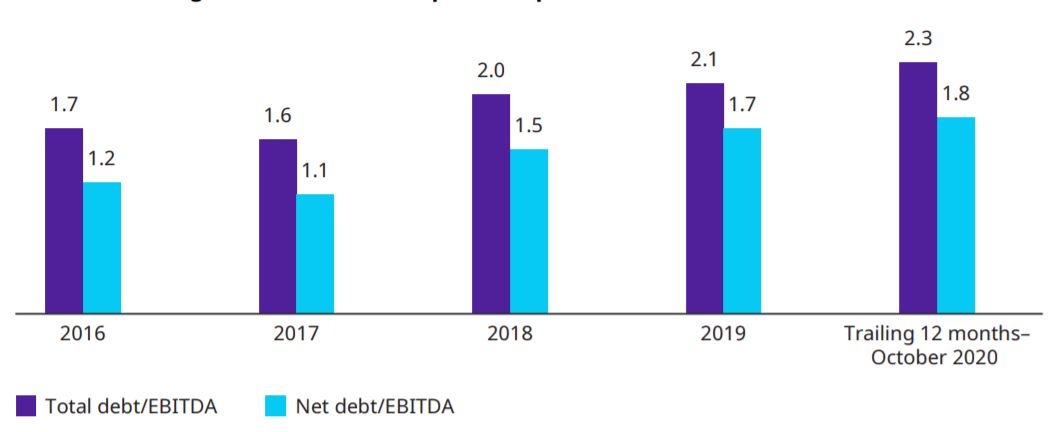

To cope with growing capital expenditure needs and declining EBITDA margins, telecommunications companies have increased their debt over the last five years. In 2020, their average total debt reached well over twice earnings before interest, taxes, depreciation, and amortization (EBITDA). (See Exhibit 2.) This debt will need to be repaid despite stagnating sales, negligible market growth, and the companies’ plans to continue paying dividends. One source of funds has been the sale of telecom towers. Data centers are another asset that can yield substantial cash if carved out.

Exhibit 2: Average debt/EBITDA multiples for operators around the world

Source: S&P CapitalQ (October 2020).

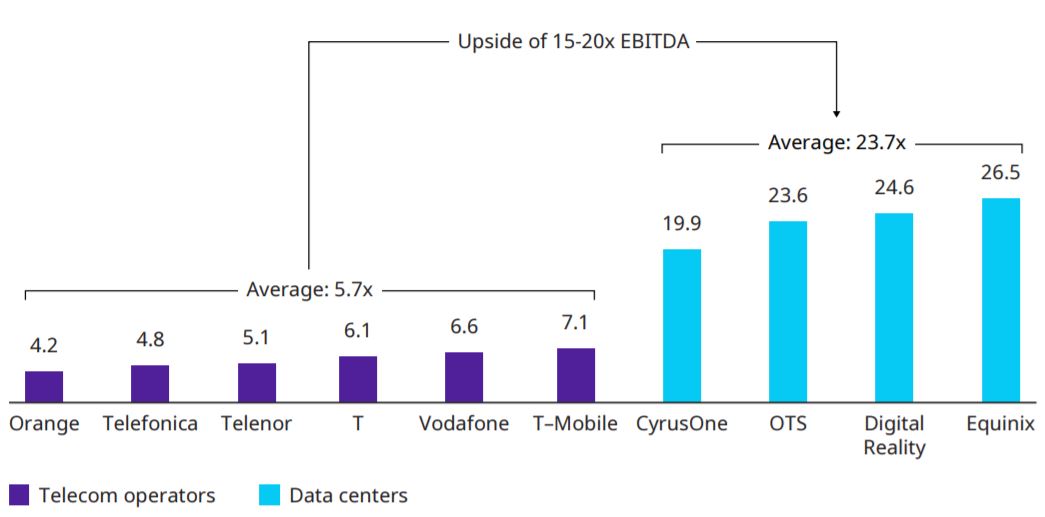

5. Valuation Arbitrage of Data Centers vs. Core Telco Business

At recent stock market levels, the enterprise value (EV) multiple of top data center specialists is around 20 to 25 times EBITDA. But a basket of European telecommunications companies yields a multiple of just four to seven. (See Exhibit 3.) Carving out a telecommunication company’s data center assets will therefore usually increase the asset’s valuation. A specialist firm is better able to leverage the asset: It has more routes to market, and this is reflected in a market valuation that is greater than the sum of the parts. Sometimes, a specialist firm may also be able to acquire cheaper financing than a telecom operator.

Exhibit 3: EMEA telecommunications operators and data centers trading multiples (2020, EV/EBITDA)

Source: Bank of America report (September 2020), "RBC datacenter download" report (April 2020). Note Company usually present across multiple geographies, EMEA being one of the core ones.

Why The Time To Act Is Now

Data centers can be highly profitable, but that does not mean telecommunications companies are the best organizations to realize this potential. Upcoming technology shifts, telecommunication companies’ uncertainty over their needs, and their lack of sophisticated operational capabilities are three strong reasons for them to rethink their data-center strategies. Moreover, data centers have high valuations, and telecoms operators are burdened with high debt at a time when they need funds to invest in fiber and 5G networks. There is now, therefore, a strong case for telcos to carve out their data center real estate. A few telecommunication players in Europe and the United States have already successfully sold their data centers over the last five years. We believe that most other operators have untapped potential to benefit from such carveouts.

Authors

Partner

Senior Consultant