While it preserves the brokerage model in the name of client choice, access and cost considerations, the Rule will nevertheless result in largescale change. Firms must develop a point of view on client best interest; re‐align brokerage advice models, disclosures, supervision and compliance oversight; and overhaul end‐to‐end technology and operational infrastructures to adapt to the new environment. Firms operating both brokerdealer and advisory models will be forced to choose between a single standard of client care, or separate regimes that each satisfy their ‘best interest’ obligations with the resultant client confusion and operational complications.

Regulation Best Interest will have significant implications for broker‐dealers’ business models in what is already a rapidly evolving advisory landscape. It will also require a substantial uplift in most firms’ supervisory and control structures

Though the Rule is generally considered less onerous than the now‐vacated DOL ‘Fiduciary Rule’, it is more expansive in breadth (for instance, Reg BI has very significant disclosure requirements). Broker‐dealers will need to actively manage the complexity of committing to long‐term business model changes while interpreting broad principles‐based regulatory requirements. The magnitude of the effort to comply is further exacerbated by the need to involve multiple stakeholders including business leadership, distribution, product, compensation, compliance, technology and operations.

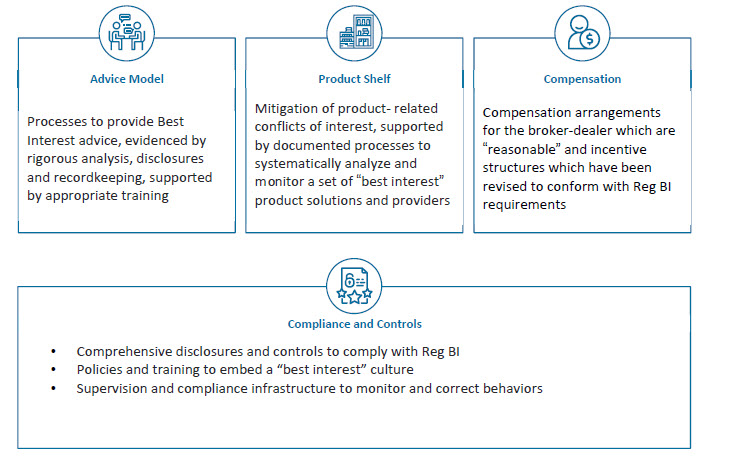

In our new paper, we recommend that broker‐dealers begin their Regulation Best Interest readiness programs now, and expect many firms will rely heavily on increased standardization of their advice models, systematic reassessment of their product shelves and potentially redesigned compensation grids to meet the required new standard.

Critical Rule Impacts

Despite industry requests, the SEC did not provide prescriptive guidance around many aspects of the final Rule, including the definition of “best interest” or a “bright line” test for compliance. As a result, broker‐dealers will need to carefully consider the general principles in the Rule and develop their own firm‐specific interpretations. Initial decision‐making will then need to be course-corrected as incremental guidance becomes available from the SEC and industry best practices emerge.

Broker‐dealers will need to carefully consider how to balance investor choice, competitive differentiation, practical implementation considerations and compliance risk – all of which will need to be supported by a comprehensive implementation, change management and training program.

Oliver Wyman Impact Framework