This article was first published on April 30, 2021.

Editor's note: Oliver Wyman is monitoring the COVID-19 events in real time, and we have compiled resources to help our clients and the industries they serve. More of our latest Financial Services thought leadership and industry expertise can be found here.

Over the past year, C-suite executives across all industries have had to think carefully about balancing "the desire to reimagine the business for the long-term and the need to remain disciplined and profitable in the short-term” (See Oliver Wyman's "When Vision and Value Collide" 2020 report). For insurers in particular, striking the right balance is critical to the industry’s future.

This paper shares our perspectives on taking a CustomerFirst approach—realigning corporate strategy with investments that are deeply tied to customers’ needs — to drive new business growth, maximize value, and capitalize on today’s market trends. Below is an excerpt from the report, for the full PDF version of Think CustomerFirst, please click here.

Where to start?

Our structured, systematic approach can help executives navigate this next wave of uncertainty and beyond—whether you lead a multi-billion-dollar insurance company or are a mid-sized player looking to gain market share. As an example, our previous Reimagining Life Insurance paper outlined a range of opportunities to help consumers improve their financial lives. We believe that insurers could be poised for long-term growth by rethinking their core value proposition around solving customer’s most pressing problems.

In this "Reinventing Insurance" installment, we explore how insurers can (re)frame their journey to capitalize on market trends and generate new shareholder value by creating new customer value

In this "Reinventing Insurance" installment, we explore how insurers can (re)frame their journey to capitalize on market trends and generate new shareholder value by creating new customer value

The COVID-19 pandemic has accelerated profitability impacts and industry disruption trends that were playing out pre-crisis. Insurers were already facing catastrophic headwinds—such as low shareholder returns (five years with returns at half of market levels), flat market capitalizations (due to companies returning capital to shareholders), and price/earnings multiples trading in the mid-single digits. And then the pandemic hit.

Today’s new normal has made it even more critical for insurers to increase their investment and innovation bandwidth. Many insurers have growth challenges with their current business models and are at risk of being rendered obsolete by competition and disruptors. There is a compounding effect of these headwinds against a backdrop of huge unmet financial needs from consumers across retail financial services sectors (insurance, retail banking, and wealth and asset management). Our interpretation of these megatrends, widely shared by our clients, is that the industry is losing relevance with consumers and could be heading toward secular decline.

We believe these trends will lead to consolidation and a greater separation between leaders and laggards. The good news is incumbents are now in a good position to solve customers’ most pressing problems and can deliver faster by assembling and absorbing more capabilities from rising fintechs and insurtechs.

We summarize a CustomerFirst activation plan to unlock new growth and market share and provide a set of practical recommendations for insurers to drive progress

Think CustomerFirst

We are operating in a new world. One in which capital is no longer scarce and information and knowledge are abundant. People no longer have to live within the confines of what companies have historically offered and are not as concerned about how industries have been defined. Today, insurance consumers have many more choices to fulfill their needs, and they are open to both established and de novo brands that represent progress. Power has shifted from the supply side—incumbents in well-defined industries—to the demand side—people with problems they seek to solve, to fulfill, driven by time and convenience.

For insurers seeking to maintain relevance and grow, the old rules of the game—manufacturing a product and distributing it through well-understood physical channels, with the right price and appropriate marketing brand awareness—no longer work. As the relentless forces of digitization collide with behavioral and societal shifts, the historical moats that have sustained many insurance incumbents are not as deep or as wide as they once were.

We are now living in a world of demand scarcity and supply abundance: insurers, brokers, and technology incumbents are fighting for relevance and scarce customer attention, oftentimes through mostly undifferentiated products. The COVID-19 pandemic has accelerated the collision of these megatrends—societal and policy; tech and data; and behavioral—encouraging disruptors to capitalize on them.

Activate a CustomerFirst mindset

Therefore, while regulation, distribution channels and brand may have kept insurtech and big tech disruptors at bay for quarters or even years, it will not fix the declining margins and low-to-no-growth reality for most insurance incumbents. At the same time, however, the consumer opportunity continues to grow. We believe this yawning value gap between what people need and what current products provide exists because incumbents are focused on product-selling under the old logic and rules of the game, instead of problem-solving with a CustomerFirst mindset.

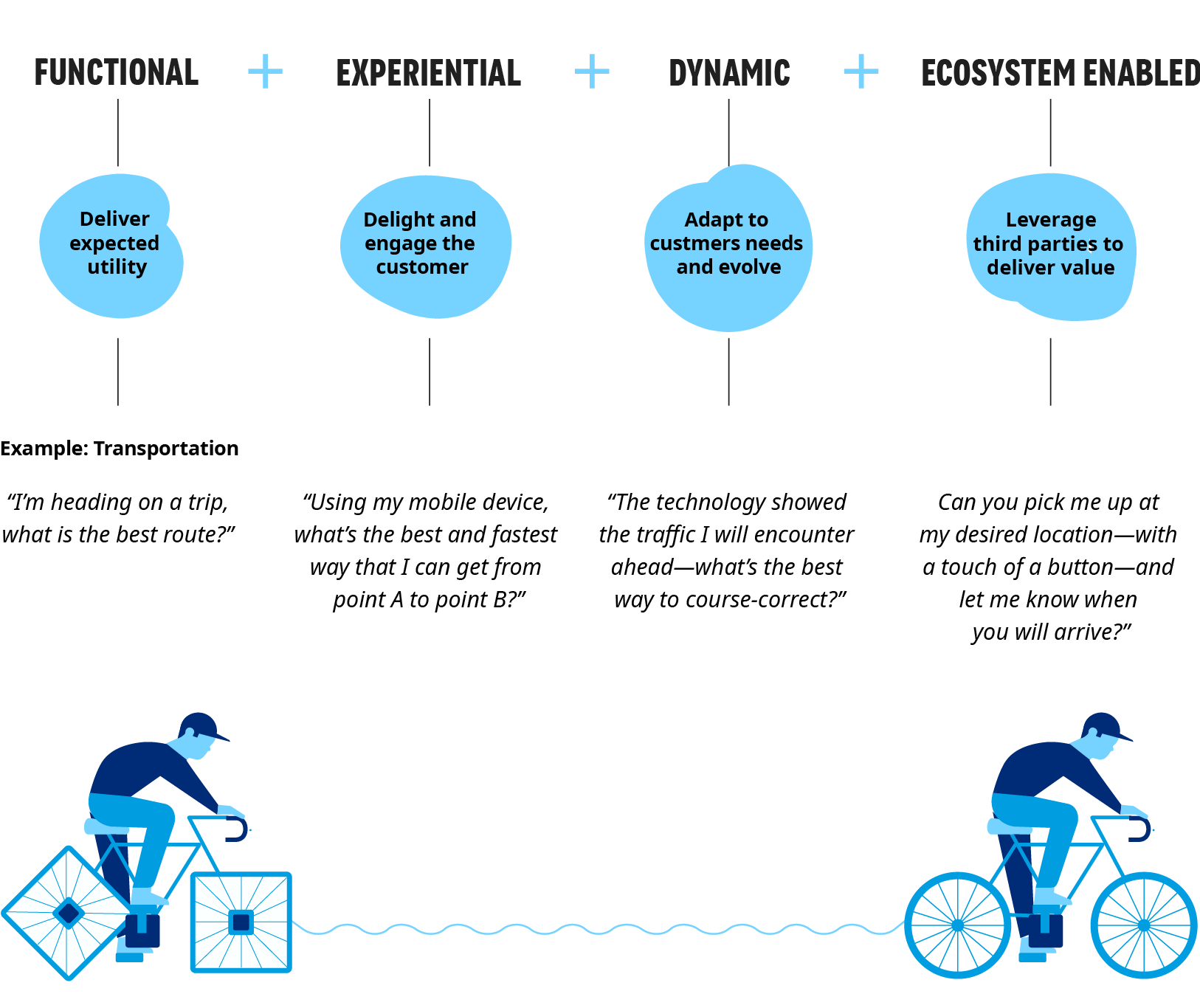

The new game places consumers in control of their lives and with the power to vote with their attention. Consumers expect active solutions (see Exhibit above) that “know them” and move with them through stages of their lives, and they have been taught to expect this by big tech players who bind great experience with the right products at the lowest total cost. In the battle for attention, companies who “do more of what customers want and less of what they don’t want,” win more share of attention.3 They start by solving a focused problem brilliantly with a subset of consumers, earning the right to more of their consumers’ attention for a broader scope of needs. With increasing attention, they build a treasure trove of customer data—signals of future intent versus records of past transactions, for example— that they harvest to improve experience or surface more of the right products at the right time, or both. We have seen big tech companies generate flywheel momentum or an accumulation of wins that leads to scale and outsized growth— the kind that investors covet.

The path to future value

The mismatch in consumer demand and market supply across financial services leads to an extraordinary opportunity for future growth. By thinking and managing in a CustomerFirst way, insurers can reposition themselves as active growth players with an increasing share of customer attention. What’s at stake? We believe those who take a CustomerFirst approach can recast themselves as “growth versus value-only” stocks and will experience Price/Earnings (P/E) expansion based on building new moats around underserved customer needs.

Below, we outline a starting set of seven practical considerations that can help your teams to begin making progress—and frame or reframe your reinvention endeavors. For the full details, please see the Think CustomerFirst PDF.

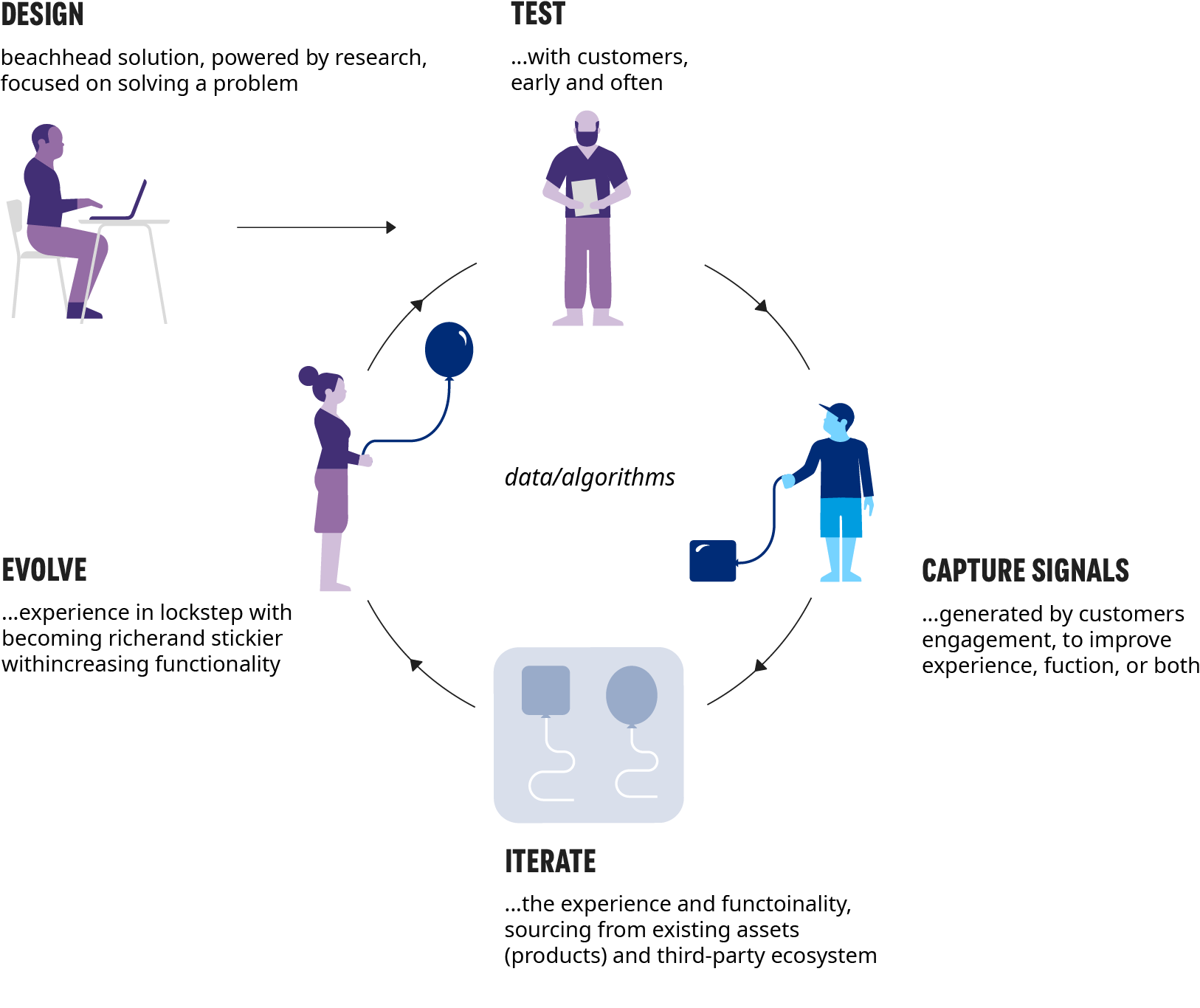

What is an active solution? Let's take a closer look

As companies gain a better understanding of their customers, they develop richer solutions with a greater scope. This kind of customer momentum can then trigger the “growth flywheel.”

It is crucial for insurers to embrace a test-and-learn mindset as they get on the growth flywheel, and to maintain it through every step of the journey rather than solely in early stages.

Get started!

Oliver Wyman can help your business reinvent itself to restart the growth engine. A CustomerFirst mindset and playbook are important aids for the difficult business transformation journeys underway.

The Prize: incumbent insurers can become more relevant than ever, critical enablers to their customers’ financial lives.