Data was analysed pre-Covid.

The digital economy is expected to add 1.1 percentage points to the European Union’s annual economic growth and to boost GDP by over 14 percent by 2030. That implies an extra €2 trillion of GDP by 2030, which is similar to Italy’s current GDP.

Today, however, Europe relies on overseas companies for most of its digital life. The digital identity of many European citizens depends on foreign email addresses; 92 percent of the western world’s data is stored in the US.

This digital dependence is a major problem. To thrive economically, Europe needs to become a leading digital economy, but this will only be possible if Europe regains control, trust, and sovereignty in data and digital technology. We think Europe will only be able to transform itself into a digital leader if it can deliver a digital action plan combining four basic elements.

In short, Europe today does not have access to the four elements required to thrive in the digital economy. One result is that Europeans are largely dependent on foreign digital technology companies. In 2019, the market capitalisation of the four biggest US and four biggest Chinese tech companies was 17 times the market capitalisation of the top 10 EU telcos.

There are four important ways in which Europe can begin to recover digital sovereignty and form a basis for its digital economy to grow.

1. Join forces to build 5G infrastructure.

First, costs should be spread, and investments should be targeted at areas that are likely to boost industrial competitiveness. For 5G, that means operators together building an interoperable European open radio access network (O-RAN) — a new way of building RANs, based on software infrastructure. Operators should be able to form focused alliances with industries in which Europe leads, such as the automotive, Healthcare, and energy sectors. Bigger, well invested shared networks allow mobile operators to compete on services whilst pooling resources in infrastructure, avoiding duplication of effort. These groupings could trigger the development of clusters of laboratories around Europe that form islands of technology innovation. Governments and the EU could allow tax breaks and let telecom companies issue “digital bonds” under favourable conditions. They should take into account the benefits of such groupings in the development of new products and services and amend competition policy accordingly. And specific 5G regulations should be designed to guarantee that transmitted data is secured and regulated in Europe.

2. Build a European distributed cloud and edge infrastructure.

A second essential component of the digital future is the development of new services based on a distributed cloud and edge infrastructure largely available, and based on European rules on topics such as data storage and processing. Strengthening and accelerating European secured and distributed cloud, such as Gaia-X, the Franco-German initiative, is essential. This would enable data infrastructure and services that comply with strict data protections rules. Allowing Europe to form a wide coalition of industrial companies which offer a broad range of digital services.

3. Develop an industrial data strategy.

A third pillar is an industrial strategy for data. This needs a new legal and regulatory framework. One condition is regulation that protects data as property, just as a house is protected. Also needed is a standard, EU-wide definition of sensitive data and the rules governing the storage and processing of this data. The General Data Protection Regulation (GDPR) was a step forward for individuals; similar rules and principles are now needed for data used in business-to-business interactions. In addition, pan-European data alliances that enforce data portability rights can create new arenas for data and distributed AI at the edge. Then, data will be increasingly stored in Europe, and both individuals and organisations should be able to obtain secured European sovereign digital identities. Further, European education must also evolve to give greater importance to digital skills, such as artificial intelligence and cybersecurity.

4. Develop a European cyber leader.

Fourthly, Europe needs leading-edge cyber technology. A first step is links between the defence and private sectors, which could mobilise defence budgets and build cyber products for both military and civilian use. European companies should be encouraged to form alliances so as to mutualise assets and share data. Some of this could be made systematic potentially through a central organisation such as CERT-EU, the computer emergency response team for the EU institutions and agencies. Europe should also create a leading cybersecurity campus, as well as European cyberproof labels to raise awareness of cybersecurity and encourage the development of capabilities.

THE NEXT DIGITAL WAVE: EUROPE, THE US AND CHINA

Europe is a major player in the world economy, generating about a quarter of global output, as measured by GDP. Europe is also home to some of the world’s most important industrial enterprises, including major vendors of 5G equipment, large automotive companies, and leading telecom players. However, Europe is lagging the United States and China in digital technology.

One reason is that European companies do not invest as much as their foreign rivals. European enterprises on the list of the world’s 500-largest tech companies invested a total of €27 billion in tech research and development in 2018. That was half as much as the Chinese companies on the list, which invested €50 billion; and one-fifth of the amount invested by US companies on the list — €134 billion.9 (Europe and the US have similar GDPs, while China’s is about 70 percent the size.)

Overall, the top four US tech companies and the top four Chinese tech firms invested over €270 billion in R&D from 2014 to 2018.

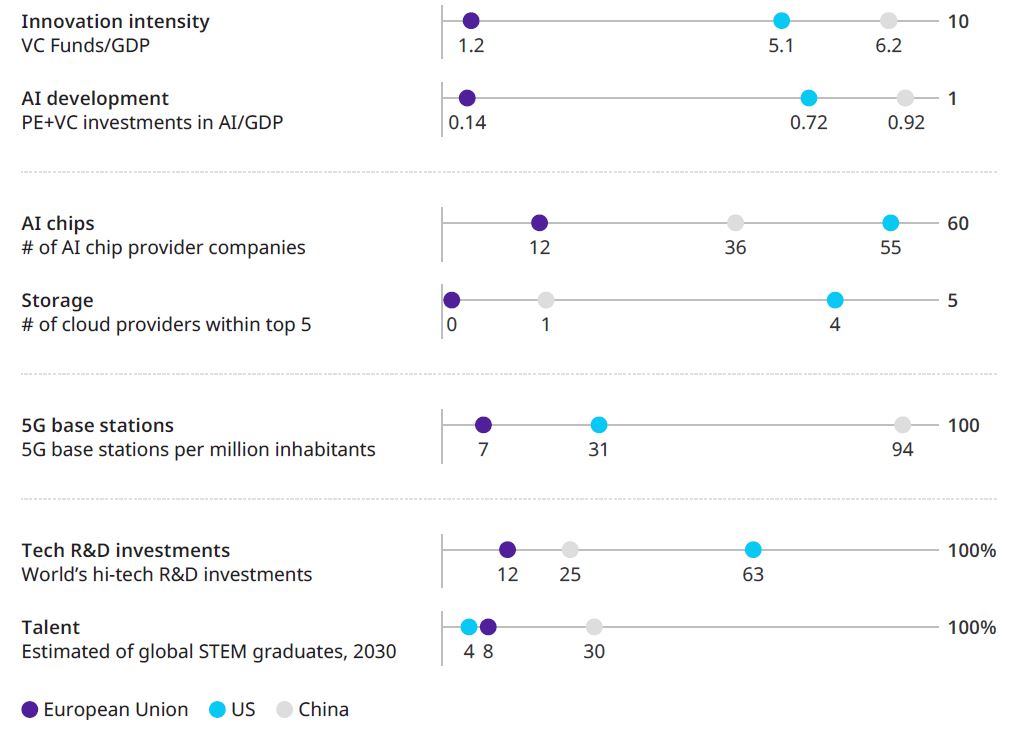

European venture capital investments were about a fifth of those of the US and China relative to GDP in 2018.11 These lower investments in tech innovation have resulted in a lag in cloud infrastructure and hardware manufacturing. Similar gaps are observed in privateequity investments in artificial intelligence: Worldwide, about 80 percent are in US and Chinese companies, and just 8 percent in European.12 At the same time, both the US and China are investing substantial public funds in AI. The US budget for 2020 alone, for example, was close to €2 billion, including ending by the Department of Defense. The European Union is planning to invest a mere €2.5 billion in AI from 2021 to 2027 — though that figure is just for EU funds and does not include funds from member-state governments.

Exhibit1: Digital Capabilities

United States, China, and the European Union

Source: Oliver Wyman analysis

Around 80 percent of data in the cloud is stored by five large tech companies, none of which is European. In hardware, no European company was among the top 10 providers of semiconductors by sales in 2019 The EU is also behind in the number of producers of AI chips, with 12 firms; China has 36 and the US 55.

The full report includes:

- Huge data growth highlights the importance of sovereignty

- The next digital wave: Europe, the US and China

- The coming opportunities: from 5G to AI

- A digital action plan for Europe

Authors

Partner

Partner

Partner

Principal