By Douglas J. Elliott

This article was first published on May 29, 2020.

Governments and central banks are devoting trillions of dollars to help small and medium-sized enterprises (SMEs) recover from the effects of the Coronavirus Recession. Unfortunately, the great bulk of this money is going out as loans, further burdening balance sheets and creating the risk that many SMEs will eventually fail or will limp along as zombie companies that are too crippled by debt to fulfill their economic roles.

We need to complement this lending with the addition of equity capital. Equity reduces firms’ risk levels by providing funding that does not have to be repaid, unlike debt. Society has a strong interest in ensuring that SMEs operate with sufficient equity to handle a wide range of potential shocks. Below explains this in more detail.

Ideally, market forces would achieve this societal goal without need for government intervention. Unfortunately, there are significant market failures under the current extreme conditions. My focus is on remedying these problems.

This paper lays out a decision framework to assist governments in designing policies to encourage equity infusions into medium-sized businesses. The fixed costs of supplying equity capital would generally render this uneconomic for small firms, and larger companies are unlikely to need this assistance, except in special cases. In those cases, the techniques described here could also be useful. For the "Encouraging Equity Investments In Medium-Sized Companies" PDF version, please click here.

Governments should encourage equity infusions into the corporate sector as a crucial response to the pandemic

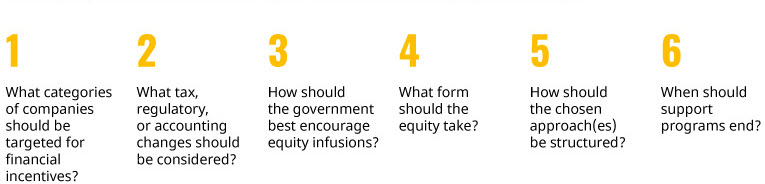

SIX DECISIONS TO CONSIDER

The optimal decision process for governments is organized around the following points:

WHY SHOULD SMEs HAVE MORE EQUITY?

Corporate debt levels in the US and many other countries were unusually high going into the pandemic, making companies more vulnerable to any shock to their revenues. It is no secret that large numbers of SMEs have suffered huge hits to their revenues that they have only partially been able to offset with cost cutting, including painful layoffs. The resulting losses reduced the value of these firms and forced many companies to take on more debt.

Higher debt and lower net worth make it more difficult to repay that debt and to cover payroll or other expenses, much less make needed new investments. Raising more equity would restore the capacity of SMEs to move forward on a sound basis while maintaining some margin of error to protect against unexpected shocks, such as potential lockdowns triggered by future waves of the pandemic.

WHY SHOULD THE GOVERNMENT STEP IN TO ENCOURAGE THIS?

Societies have a stake in vibrant SMEs, because they employ much of the workforce and generate a great deal of innovation. Further, a wave of bankruptcies caused by the Coronavirus Recession would destroy a huge amount of “going concern” value at these companies. Any good business has created internal infrastructure and a web of external relationships that would be difficult and costly to recreate. Finally, the loss of a significant number of SMEs would accelerate a trend towards concentrated market power in many industries that is already concerning.

In theory, financial markets would match equity investors to SMEs needing equity, without government intervention. Unfortunately, this has always worked less well for SMEs than for larger corporations. Further, the current recession means that there is a huge equity need to be filled across a wide range of firms at a time of very high uncertainty, which makes equity investment harder.

Society has a strong interest in ensuring that SMEs operate with sufficient equity to handle a wide range of potential shocks

Even if there is sufficient equity investment available in the aggregate, there are several reasons why desirable transactions may still not occur. Investors will demand cheap equity in light of the highly uncertain environment today, but businesses may not be willing to sell that cheaply, preferring to risk failure rather than sell shares at a fire sale price. The high level of competition for new equity in the current environment may also leave some firms out in the cold. This problem will be exacerbated in many cases by insufficient information about firms and their prospects to allow investors to get comfortable.

Thus, there appears to be a large market failure that justifies government intervention.

It’s time for governments to shift from a focus on corporate liquidity to a focus on solvency

SIX DECISIONS TO CONSIDER

1. WHAT CATEGORIES OF COMPANIES SHOULD BE TARGETED FOR FINANCIAL INCENTIVES? (CLICK HERE)

Governments should carefully focus their resources on the particular types of companies that both need and merit such support. Despite large resources at their disposal, governments face even bigger challenges and therefore need to be efficient and targeted in their strategies.

Targeted companies should pass the following tests:

Viability. The underlying business model of a company must be sound, allowing the firm to earn an acceptable return going forward, assuming it operates with a reasonably structured balance sheet. This could include companies that are executing major strategic changes, as many will be in response to the Coronavirus Recession. However, a firm should not be considered viable if the additional equity will merely allow it to limp along as a zombie company earning a meager return and therefore be too hobbled to contribute meaningfully to the economy.

Difficulty accessing equity. Governments should not waste resources on firms that have ready access to sufficient new equity at reasonable prices. For this reason, there may be little need for direct intervention to assist large public companies in raising additional equity. Medium-sized enterprises are the most likely targets to be optimal, although there may also be some larger firms in troubled business sectors that merit equity investments but cannot currently get them at reasonable terms.

Promotion of other societal objectives. Governments with relatively more interventionist views may wish to target firms that help further other societal objectives, such as environmental sustainability or national security. The pros and cons of this are actively debated, including in discussions of “Capitalism 2.0”, so I will not discuss them further here.

Avoidance of violations of competition or treaty constraints. Governments will wish to avoid creating or encouraging monopolies, oligopolies, or unnecessary barriers to competition as they make choices about who to aid. Further, a number of countries have treaty limitations on the aid they can provide corporations. In most cases this is the result of bilateral or multilateral trade agreements. In the case of the European Union, there are extensive constraints on state aid that are overseen by the European Commission to help preserve the single market.

2. WHAT TAX, REGULATORY, OR ACCOUNTING CHANGES SHOULD BE CONSIDERED? (CLICK HERE)

Governments should examine whether changes to tax laws, regulation, or accounting rules could solve or substantially mitigate any problems of access to equity. Most countries have approaches that present unnecessary obstacles to adequate equity levels. In some cases, this is a clear tax bias against equity, favoring debt issuance instead, as is true in the US. There are also sometimes accounting or management compensation approaches that encourage share buybacks rather than earnings retention. In some countries, there are unnecessarily cumbersome regulations that make it too hard or expensive to raise equity or to operate as a public company.

In general, it would be cheaper and more beneficial to society to fix problems such as these, rather than to try to counterbalance them with other incentives that may create their own distortions of economic behavior.

3. HOW SHOULD THE GOVERNMENT BEST ENCOURAGE EQUITY INFUSIONS? (CLICK HERE)

A series of five questions can guide policymakers to the optimal methods for encouraging equity infusions. The first question is whether the investment expertise lies in the private or public sectors. The remaining questions focus on the main obstacles to the private sector providing the needed equity on its own. This could be: lack of sufficient funds looking to invest in equity in the aggregate; too low a potential return; too high a risk; or too little information. Different solutions exist, depending on the obstacle. If there are multiple significant obstacles, then multiple solutions may need to be deployed to complement each other.

Q1: Do private sector investors have the necessary expertise to make good investment decisions in this environment?

In some emerging markets, government bodies, such as sovereign wealth funds, may have more expertise than private investors.

A: In most cases, private sector investors will be better positioned to make investment decisions and the government should use various incentives described below to encourage them to invest. If that is not the case, the government should take the lead, either investing the full amount needed or bringing in private sector investors as passive participants.

Q2: Is the problem primarily a lack of sufficient capital for equity investment?

If equity markets are undeveloped, there may simply not be enough money dedicated to equity investment to handle the very large equity needs driven by the Coronavirus Recession.

A: In this circumstance, the government can use its own funds to co-invest, magnifying the ability of private sector investors to provide a level of new equity adequate for the current need.Countries with well-developed equity markets, of which the US is probably the extreme case, may only need this type of intervention selectively for certain parts of the market. Some other countries may want to use this more widely to ensure sufficiently broad and timely equity infusions. Government funding could be through direct investment or indirect investment by mandating or encouraging quasi-government bodies to invest.

Q3: Is the main problem insufficient expected returns?

In theory, the existing owners of a firm and potential new equity investors should be able to find a mutually agreeable share price to raise the necessary equity infusion. However, there are multiple barriers that could prevent this under the current circumstances, such as: lack of adequate and timely information; the high degree of uncertainty about the economy and business models; lack of expertise in financial negotiations among managers of smaller businesses; etc. Any of these barriers could produce a gap between the price sellers demand and that which investors are willing to pay.

A: Subsidize investment with an upfront payment and/or periodic payments. The government could simply pay qualifying businesses to raise equity, lowering the price they would need to demand from investors. (Alternatively, investors could be paid to buy equity in qualifying firms, although this may be politically more difficult.)

Any payments could be made upfront or the government could choose to spread them over time, either to ensure certain conditions are met or to avoid continued payments if a company fails anyway. Tax breaks could also be used in lieu of outright payments, although this would only work to the extent companies anticipate making tax payments in the relevant period. So, firms with large tax loss carryforwards would not find this attractive.

It may be desirable for the government to receive warrants or use mechanisms to share in the profits if investments prove particularly lucrative. This would provide an upside to the government, on behalf of all taxpayers, and would be politically attractive. The negative is that the upside would come at the expense of either the business or the other investors, causing them to require better terms for the other aspects of the transaction, such as the price.

Q4: Is the main problem the level of risk investors currently face?

Investors generally make choices based on risk/return trade-offs. The high levels of risk that currently exist may be a larger barrier than price expectations. In particular, much of the risk today is classic “Knightian uncertainty” meaning we don’t even know the shape of the risk function, which is especially hard to price. The risks of most concern could be specific to the company or industry, such as the question of how much air traffic will rebound and when. Or, it could be macroeconomic, with investors focused on how bad the recession will be and what the shape of the recession and recovery will be.

A1: Reduce the risk for portfolios of investments in targeted enterprises. Governments could, for example, provide guarantees that a portfolio of investments in targeted companies will not lose more than X percent of their value. This could also be done for investments in individual firms, but the government can reduce its risk by taking advantage of diversification within portfolios. The government could charge a fee or take a share of the upside in exchange.

A2: Insure against some bad macroeconomic outcomes in order to reduce the risk investors face. The government could provide limited insurance to investors in qualifying businesses to protect against extreme macroeconomic outcomes, such as a cumulative decline in gross domestic product (GDP) of 10 percent over the following 12 months. This would help spur investment, to the extent that investors are seriously concerned about tail risks in the wider economy. The government could charge a premium for the protection.

Q5: Is lack of information about the firm and its prospects the biggest issue?

Particularly in the middle market, it can be difficult to obtain reliable information of the type that equity investors normally use when investing in larger companies.

A: The government could create a centralized data utility for information on SMEs or could encourage or provide support for a private sector initiative. Participation by SMEs would be voluntary. The information would be standardized for easy comparison. Many details would need to be worked out, but it opens the possibility for investors and businesses to move more quickly to find each other and to negotiate deals.

4. WHAT FORM SHOULD THE EQUITY TAKE? (CLICK HERE)

Equity can take a number of forms. The predominant form, and the strongest support for balance sheets, is “common stock.” This represents ownership of a piece of the company. It never has to be repaid, there is no guarantee of dividend payments, and it generally ranks last in order of preference in bankruptcy. In contrast, “preferred stock” has similarities to both debt and common stock. There is a defined dividend rate, analogous to the interest rate on debt, but it is not guaranteed. The only dividend protection generally is that common stock cannot pay any dividends without paying the full preferred dividend, including, in some preferreds, any unpaid prior year dividends. In bankruptcy, preferred stock has priority of repayment over common stock, but behind everything else. Unlike common stock, preferred stock generally carries no voting rights, except in limited circumstances necessary to protect the direct interests of the preferred holders.

The strongest support governments could provide would be to invest in common stock and/or to encourage private investors to do so. However, there may be cases where the interests of the government, the firm, or an investor are better served with preferred stock. For example, firms may be unwilling to give the government or investors voting stock or the government might rather have the lower risk of holding preferred stock. The debt-like nature of preferred stock may also make it easier to negotiate a transaction with less information than a common stock investor would need.

In sum, common stock investments would strengthen the balance sheets of targeted companies more and would therefore generally be better for the economy. However, information deficiencies, concerns about corporate control, or risk aversion by one party may push the government towards preferred stock instead. It is also, of course, possible to combine investments in common stock with investment in preferreds, if that would achieve a better balance of objectives than going with a single type.

5. HOW SHOULD THE CHOSEN APPROACH(ES) BE STRUCTURED? (CLICK HERE)

HOW SHOULD ANY CO-INVESTMENTS BE STRUCTURED?

There are two broad approaches governments could take to making co-investments. One is to create, or harness, a sovereign wealth fund that will actively decide about which investments to make, following guidelines set down by the government. The other is to take a more passive approach and agree to co-invest with qualifying investors in businesses that meet specific criteria.

The passive approach of co-investing with the private sector makes most sense where equity markets are well developed, and governments are less interventionist in ideology. In this approach, governments should ensure that a substantial portion of the equity funding comes from the investors and that those investors retain enough “skin in the game” to use their best efforts to identify good investments and negotiate an appropriate price for their shares.

If the government is tying its returns to those of investors, it will want to establish criteria for those investors to qualify, rather than agreeing to invest alongside anyone. This way, the government can ensure that those making the investment decisions are experts and have a track record of success.

The active approach may be more suited to governments with already substantial sovereign wealth funds or other internal expertise in investing, combined with an ideology consistent with government intervention on this scale. It will be important, of course, to ensure that the sovereign wealth fund managers are given appropriate guidelines and incentives. Governments will want the right investments to be made, at the right prices, from a societal point of view.

HOW SHOULD ANY SUBSIDIES BE STRUCTURED?

Subsidies could be relatively straightforward, but some decisions would still need to be made. The first choice would be whether to deliver them to the businesses that receive the investment or to the investors. These are roughly equivalent, from an economic point of view, since the subsidies would be factored into the price negotiations between the buyers and seller of the equity. That is, one dollar of subsidy to the business should reduce the required price from the investor by one dollar, just as one dollar paid to the investor should increase their acceptable price for the investment by one dollar.

However, there are likely to be administrative, accounting, tax or political reasons to choose one route over the other. The first three sets of reasons would vary considerably by jurisdiction. However, the political ones are likely to share a common characteristic, which is that the public is generally more sympathetic to the businesses receiving the aid than to the investors. This may tip the scales towards having the subsidy flow to the firm rather than the investor.

The second decision is how to determine the appropriate level of subsidy. Who should make the decision and on what basis? There should be strong guidelines for whoever does make the choice and it may be politically advantageous to use straightforward formulas, at the expense of a reduction in the ability to target subsidies optimally. Ideally, though, there would be some room for government experts to make judgments, within the overall guidelines.

The key criteria from an economic point of view are:

Social value of encouraging the equity infusion. This could be tied to a number of factors: size of the company, level of employment, and vulnerability if equity is not raised, for example. These social value considerations would set the upper limit of the subsidy’s size.

Need for a subsidy to make the transaction happen. Ideally, the government would provide just enough subsidy to make a transaction feasible. This may be difficult to determine but could be approximated by some rough criteria (such as assuming that larger companies, and those that are already public, will not need the same degree of encouragement). Even better would be to create some auction mechanism to produce competition for the subsidies, so that investors and businesses willing to accept lower subsidies would get preference, all else equal.

The third decision would be whether to provide an upfront payment, payments spread over time, or both. Upfront payments are the strongest incentives for a transaction and bring certainty. However, payments spread over time can have a measure of conditionality; if nothing else, that the business has not failed. Other conditions, such as regarding share buybacks or levels of debt or executive compensation could be added. Each of these conditions reduces the incentive effect, but may achieve other social goals. (Some of these requirements could also be attached to any upfront payment as well, but would require subsequent monitoring and penalties for violations.)

The fourth decision is whether the government should receive warrants or other rewards if investors do particularly well. Clearly this would be of value to governments and would help with the politics, since investors would not be the only winners. However, the incentive effect on investment would be reduced by the potential payouts to the government.

HOW SHOULD ANY PORTFOLIO GUARANTEES BE STRUCTURED?

The other broad way to make the risk/return trade-off more attractive to investors is to reduce the risk. This could be done directly by guaranteeing that losses would not exceed a certain level. Design decisions would need to address a number of questions.

Q1: What investors would be offered the guarantee?

A: In theory, the guarantee could be offered to any of the investors, since the goal is to get equity funding to the right businesses. However, governments will almost certainly want to limit their risk by only guaranteeing portfolios held by experienced, expert investors. At the same time, they will wish to avoid the appearance of favoritism, so there will be a need for sensible, objective criteria.

Q2: How large a portfolio would be necessary to qualify for the guarantee?

A: There is not a clear answer to this. The larger the portfolio size, the lower the risk for the government, all else equal, due to diversification benefits. However, the larger the requirement, the fewer the investors who might wish to participate.

Q3: What level of guarantee should be provided?

A: The same basic considerations apply as would be used to determine what level of subsidy to provide if that approach were used.

HOW SHOULD ANY INSURANCE AGAINST MACROECONOMIC TAIL EVENTS BE PROVIDED?

Another way to overcome risk aversion would be to target the largest source(s) of risk. Currently, a high degree of the risk relates to the uncertainty about macroeconomic prospects. We do not know how far GDP will fall, how long it will stay down, and whether there will be a V-shaped recovery, a W-shaped one, or something else. This makes it an unusually difficult time for investors to judge risks.

Governments could reduce that uncertainty by providing protection against the more extreme macroeconomic possibilities. For example, by insuring an investor against a drop in GDP of 10 percent or more for the next 12 months.

There is a threshold question when considering this approach, which is whether a government can afford the possibility of making a large payout in a future state of the economy where its revenues will be down sharply, and its other expenses have risen. This could prove too costly for some governments with tight fiscal constraints. However, other countries, including the US, should be able to afford this risk.

The potential cost of this insurance would be partially or fully offset by the reduction in government assistance necessary to aid the economy in that adverse scenario. The first round of reactions to the pandemic demonstrates that governments are prepared to make very substantial payments when the economy shrinks sharply. Additional equity at the insured firms would reduce the need to rescue them later and might allow them to keep paying some employees who would otherwise have been let go.

This approach would require several design decisions:

What event to insure against? The likeliest candidate would be an extreme, but plausible, cumulative drop in GDP. However, other events could also be considered. They would need to be objective, measurable, and reasonably related to the macroeconomic risks most relevant to the business receiving the equity infusion.

How long should the insurance protection last? It could be that the scariest risks are all in the first year, so that the protection need not be long lasting. However, there might be a case for a longer period.

What payout would be made? One might offer a payment of 25 percent of the initial investment if the event occurs, for example. This would leave the investor with substantial risk, but would protect their downside, especially as the value of the investment may still be positive, even if much smaller than the original price. Or, the payouts could scale up as the event worsened beyond the initial threshold.

What should the government charge for the insurance? The incentive is largest if there is no insurance premium. On the other hand, charging some premium would increase the likelihood that an investor who took the protection actually valued it. It’s easy to take protection for free, but perhaps the investor is not concerned about an event as extreme as the protection being offered. In that case, they might choose not to buy it. That said, sophisticated investors might see it as a cheap option and might even sell equivalent protection to other parties for a market price, rather than keeping it as protection. Of course, in that case it would work like an upfront subsidy, since there would be additional revenues for the investor.

6. WHEN SHOULD SUPPORT PROGRAMS END? (CLICK HERE)

There is a real need for strong government interventions in the economy during the current crisis, and likely during the recovery phase, including those actions described here. However, it is important for governments to pull back to sustainable roles as soon as feasible. Some of the ideas in this paper may be worthwhile to continue in the long run, but many will not be needed after we are out of the woods. Failure to pull back on emergency programs would distort markets, making it difficult to optimally allocate resources across the economy. They could also prove expensive to continue, soaking up scarce government resources. Therefore, where possible, these programs should be designed with end dates or with a defined process for determining when to scale them back or end them altogether. Otherwise, we risk proving once again the aphorism, “there is nothing more permanent than a temporary government program.”

CONCLUSIONS

It’s time for governments to shift from a focus on corporate liquidity to a focus on solvency. Governments should encourage equity infusions into the corporate sector as a crucial response to the pandemic.

Decisions about which policy approach to take follow a straightforward logic. There is no need for the government to do anything if market forces will bring the desired result on their own. Or analysis may show that the problem stems from tax, regulatory or accounting obstacles that could be eliminated.

However, it is almost certain that national policymakers will conclude there are significant market failures at this time, particularly for medium-sized enterprises needing equity. If so, the next step in the decision tree is to determine whether it is simply a question of total capacity for equity investments, in which case the government can co-invest with private sector investors in order to raise the aggregate capacity to the necessary level.

More likely, the problems would not be solved by additional capacity alone. The problem may be that the risk/return trade-off for investors causes them to demand an excessively low price, from a societal point of view, for the equity they wish to purchase. In that case, governments should consider either subsidies to improve the return side for investors or insurance to reduce the risk side. The choice between subsidies and insurance depends on a variety of factors, including the government’s fiscal capacity to bear the losses if insurance payouts are triggered, as well as the risk appetites of the private sector investors, which will help determine the effectiveness of a risk-reduction approach. In addition, political, administrative, tax, and accounting factors would need to be considered.

Whatever approach(es) are taken, the time to move forward is now, before too many medium-sized enterprises fail.

Douglas Elliott is an Oliver Wyman partner focused on the intersection of Finance and public policy. He is the author of the book, Uncle Sam in Pinstripes: Evaluating US Federal Credit Programs. Prior to his current position, he was a scholar at the Brookings Institution and a Visiting Scholar at the IMF. Before that, he was the founder and principal researcher for the Center On Federal Financial Institutions. He began his career with two decades as an investment banker, primarily at JP Morgan.