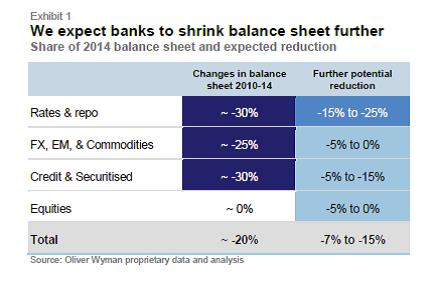

Financial regulation and quantitative easing (QE) are at the heart of a huge shift in liquidity risk from banks to the buy-side, which is increasingly a concern for policy makers. We expect liquidity in sell-side markets to deteriorate further, as regulation shrinks banks’ capacity another 10-15% over the next two years. Our interviews with asset managers found concerns over scarcer secondary market liquidity, particularly in credit.

Regulatory risks are rising for asset managers, as policy makers increasingly fret about the risks to financial stability from QE exit and market structure changes. Our base case is for an incremental approach that involves stress testing of select funds and a range of micro reforms. This could add an extra cost of 1-5% to asset managers.

Diminishing returns on capital from market making demand even greater efficiency, dexterity and scale from wholesale banks to achieve 10-12% returns. More firms will trim this business, ultimately leaving a potentially attractive prize for those able to endure.

We expect banks to shrink balance sheet further

Share of 2014 balance sheet and expected reduction