Despite this, we see a good return on equity (ROE) – after adjusting for the many one-off Profit and Loss (P&L) impacts and regulator fines – in the retail and business banking market as a whole, and opportunities for further improvement. We also observe widening differences across markets, ranging from rising returns in the UK and Swedish markets to weakening returns in Spain and Italy.

While we see a common set of themes relevant for European retail bank management teams, their importance and prioritisation differ markedly across countries. At one extreme, challenges from regulation and changing customer behaviours provide both risks and opportunities for growth, whereas in the most crisis-hit European markets, low interest rates and credit loss management provide the biggest challenges.

This report builds on last year’s publication “An opportunity for a renaissance” and on the research and experience of Oliver Wyman consultants to provide an updated view of the underlying economics of Europe’s largest retail and business banking markets, their resulting outlook and management agenda, and some emerging best practices in managing these issues.

The report is structured into 3 sections:

- Current market performance: a detailed, country level review of European retail and business banking profitability and the underlying drivers.

- Progress report and management agenda: an updated perspective on progress against last year’s management agenda and a view on today’s priorities by market.

- Thematic perspectives: Oliver Wyman’s views on emerging best practices in three of the major challenges facing European retail banks in the next 3–5 years:

3.1 Living with low interest rates.

3.2 Transforming small business banking.

3.3 Delivering impact via improved customer experience

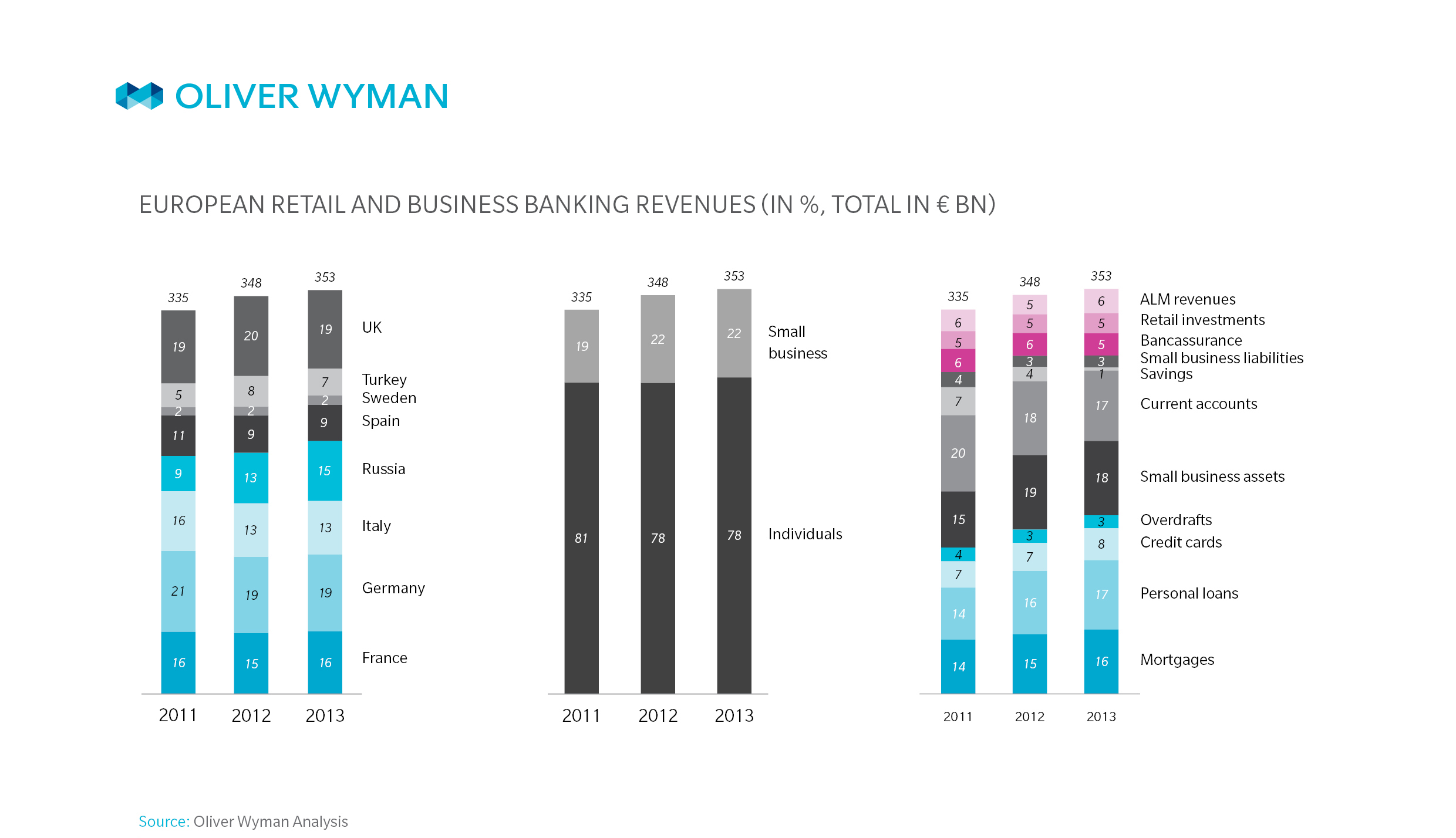

European Retail and Business Banking Revenues

2013 has been another challenging year for European Retail and Business Banking. Revenues have slowed down their past growth (+1.6% in 2013) and at the same time, we observe a shift in product mix with asset products gaining ground (albeit mainly offset by a corresponding decline in retail deposits). At a segment level, we see a proportional increase in revenues across the small business and individual segments.

Underlying Profitability still Varies Significantly Across European Markets

With the exceptions of Spain and Italy, underlying ROEs across European retail and business banking markets remain healthy, reemphasising the importance of this business to overall bank profitability and pointing to a more promising future for bank performance as legacy issues (non-core portfolios, legacy conduct provisions) dissipate in future years. Indeed we expect that retail and business banking will not only fuel the recovery of Europe’s economies but will be the underlying driver of improving bank returns going forward.

.jpg)