The Potential New Normal in Insurance Products

Editor’s Note: The following article is part of an ongoing series offering our strategic advice and expertise on what healthcare industry stakeholders should do in response to the rapidly evolving novel coronavirus (COVID-19) pandemic. This is Part 2 of a three-part series. In Part 1, ("Is There a New Normal in Commercial Health Insurance?") we described the potential mix shift under various unemployment scenarios and modeled the various life flows and top-line revenue impact for payers. Here in Part 2, we examine product and distribution implications of our “new normal” in the US. In Part 3, ("What A New Member Mix Means for Payers") we will again look more closely at the mix shift modeling, including varying recovery scenarios, margin impact, and possible future legislation.

As payers respond to the COVID-19 pandemic, they are moving quickly. They are waiving fees, assisting providers, and communicating constantly with members. In the meantime, they should also be taking the long view, thinking carefully about the future and what the new normal may look like once the curve flattens out.

In Part 1 of our series, we presented a model explaining how COVID-19 may shake up the health insurance mix for millions of people later this year. As we continue to push forward into unchartered waters, not knowing how long the pandemic will last and how quickly the economy will rebound, we do know one thing: The “Corona Effect” will have a profound influence on what consumers want from their employer health and well-being benefits, and what employers can afford and desire to offer. Payers who remain out in front with effectively marketed new product offerings will be well-positioned to serve their members as we adjust to a new normal.

The “Corona Effect” will broadly redefine the outflow of lives from the employer ranks to Medicaid, Affordable Care Act (ACA) exchanges, and the uninsured. If this outflow becomes permanent, payer economics, line of business focus, product portfolio, sales and broker alignment, and more may look very different in time. For those who remain on commercial insurance, employees will demand more holistic healthcare and greater financial protection. Virtual, easy access to primary care could be the norm. Employers will focus even more on value and administrative burden reduction and be open to trying more innovative products and serving their employees more effectively and affordably given future threats of sudden employment disruption. And, depending on the administration, the government might ease some ACA restrictions and impose others to stimulate employer coverage, particularly at the lower end of the market. Even if there is a return to the status quo in terms of funding sources, consumer, employee, and employer needs will be forever altered.

Below, we detail what all of this may look like.

Employer Product and Distribution Implications of a New Normal

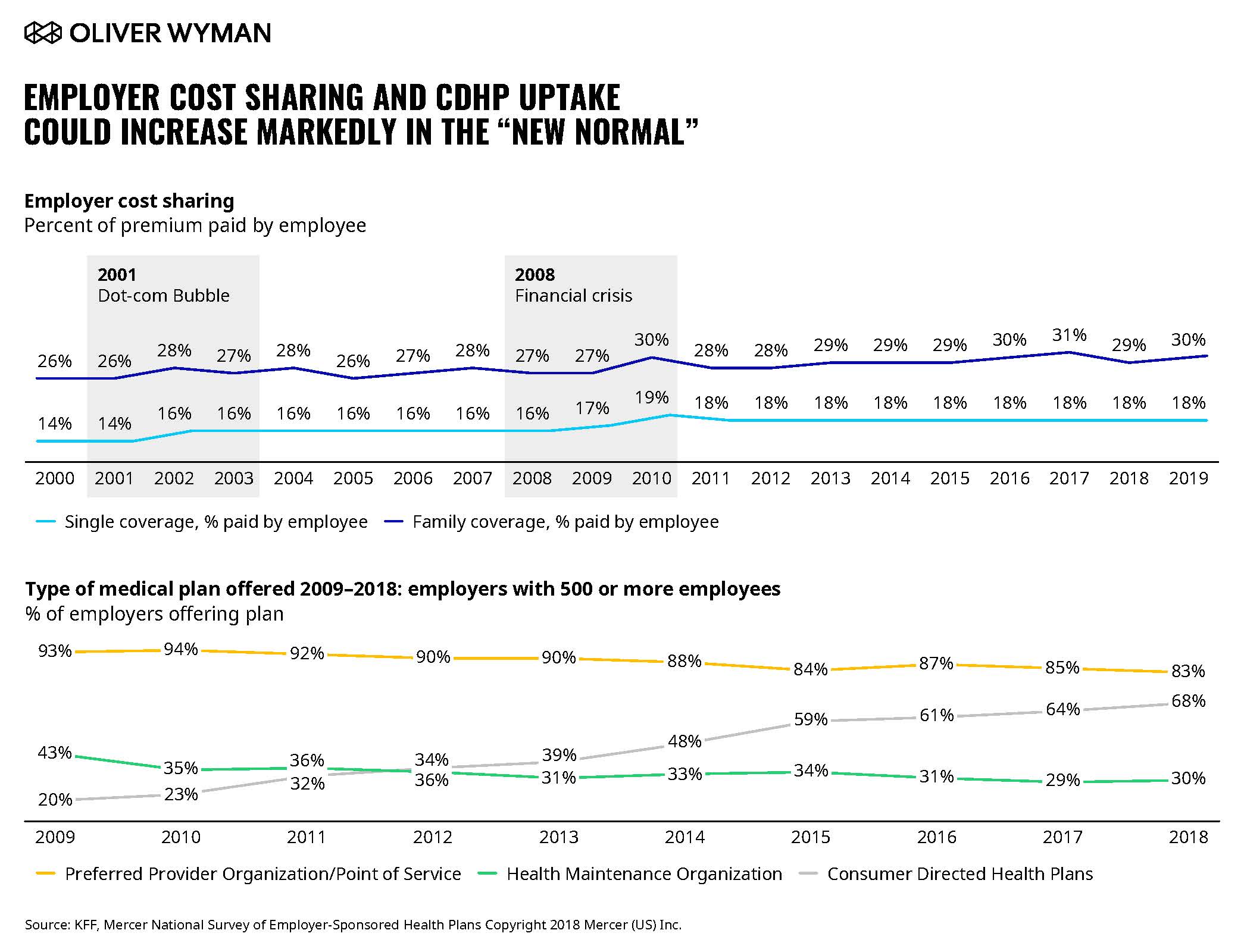

1. Expect a resurgence of Consumer Directed Health Plan (CDHPs), with even higher deductibles and further cost-sharing. CDHPs recently reached their zenith. In 2019, 58 percent of covered workers were employed by companies offering a CDHP. And, over 30 percent were covered by such plans. That number was once expected to decrease in 2020.

Regarding the 2020 outlook before the COVID-19 outbreak, more companies were expected to offer Preferred Provider Organization (PPO) plans this year. (And more employees were expected to choose PPO plans, as, well). Those plans are largely locked in for this year.

PPO plans – which have more expensive premiums but more predictable out-of-pocket costs – similarly offer flexible strategies that aren’t compatible with Health Savings Accounts (HSAs). Firms might want to pay for care prior to a deductible being met, for example. Or, they may choose to eliminate employee charges for specific kinds of services, advised Tracy Watts from Mercer. Examples of these strategies could include direct primary care arrangements in which physicians are paid a monthly fee to provide care at no cost to the employee, or employer-subsidized telemedicine programs.

The proposed elimination of the Cadillac Tax further encouraged the pendulum swinging back to PPOs. According to National Business Group on Health, if you look at last October’s open enrollment numbers, only a quarter of employers were planning to offer CDHPs as the sole offering. This number is down 14 percentage points from two years ago. But these PPO trends, with their increased choices and flexibility, will all likely reverse back to CDHPs as a result of the “Corona Effect.” Look for a surge in CDHP uptake for 2021.

2. Expect continued telemedicine explosive growth. One significant (and quite interesting) employer strategy before the pandemic – especially with smaller to mid-market sized firms – was the offering of telemedicine services along with CDHP at no extra cost to the employee as a utilization incentive and to avoid dipping into required deductibles. This strategy was beginning to pay off. According to Oliver Wyman research, once someone has tried telehealth services, they generally start to prefer them over many traditional in-person services.

In 2020, there may be over 1 billion virtual visits nationwide, with the vast majority attributed to COVID-19 care. General medical visits are expected to surge to 200 million, up from an original estimate of 36 million.

As consumers massively utilize telemedicine during this crisis via an era of “forced innovation,” expect telemedicine to be a core part of the offering (including for behavioral health) going forward, with employees taking on a greater burden of the costs of these services.

3. Further penetration of and the emergence of new medical supplemental products. Oliver Wyman research on employers and brokers shows increased importance of ancillary and voluntary products to help consumers protect themselves financially and meet employees’ increasing and diversified holistic “well-being” needs.

For at least one in three employers in the small to mid-market (and even larger proportion upmarket) – and importantly, an ever-increasing number of sophisticated brokers – conversations about medical supplemental products are no longer relegated to the last ten minutes of the benefit strategy or simply ceded to enrollment firms. Instead, they are now increasingly considered as a coordinated, integrated component of the overall health benefits approach.

To that end, we’re now seeing an emergence of true “gap” plans designed to cover multiple medical expenditures (both routine and catastrophic) as companions or “linked” plans to core medical offerings. In addition, traditional ancillary (like dental and disability) and voluntary medical supplemental offerings (like critical illness and accident) are embedding product components and linked benefit/claims structures that allow for more robust and enhanced coordination of care, payment of benefits, and administrative ease.

Also, other new voluntary offerings reflect people’s greater focus on financial security and well-being. These facets will appeal even more to certain employee segments when they begin operating in the new normal. These offerings include caregiving support (like offering stipends, work from home flexibility, and discounts for vetted in-home services), well-being offerings in areas of mindfulness, sleep, stress, and nutrition, and financial services in areas like budgeting, end-of-life planning, and student loan repayment.

If you’ve happened to notice a sudden surge in virtual health services (like meditation sessions to relieve stress) recently, you’re not alone. The good news is most well-being related services can be delivered seamlessly virtually, which will fit well as low-cost offerings that will appeal to consumers in the new normal without significant costs to health plans.

On that note, when it comes to matters of the physical body, other voluntary or partially employer-sponsored programs like heart health, diabetes, and chronic pain are also being ramped up and offered digitally with enhanced technology options and consumer-friendly approaches. Expect this surge to continue well into our new normal, especially given consumers’ pre-COVID-19 burgeoning hunger for a new kind of healthcare experience.

4. Family and Medical Leave Act. The Family and Medical Leave Act of 1993 (FMLA) entitles eligible employees to take 12 weeks of unpaid, job-protected leave. Those who are eligible are covered employers with over 50 employees. This leave is reserved for specified family and medical reasons with continuation of group health insurance coverage under the same terms and conditions as if the employee had not taken leave. In recent years, more states have layered on additional family medical leave benefits including financial remuneration, further complicating the claims and administrative processes. And now the Coronavirus Aid, Relief, and Economic Security Act (CARES Act) provides further benefits for employers with under 500 employees related to COVID-19, like taking leave if a child’s school or care provider has closed their doors due to COVID-19. Even pre-COVID-19, carriers have been promoting absence management and compliance/admin services related to FMLA along with state-specific FMLA and short-term disability insurance coverage. We expect further focus here and evolution of hybrid and caregiving-like offerings as administration and coverage becomes more complex along with greater utilization of such products and services in the new normal.

5. Expect more Individual Coverage Health Reimbursement Arrangements (ICHRA). According to pre-coronavirus estimates, up to 5 million employees were expected to shift from employer coverage to the ACA exchanges due to ICHRA. We thought that number to be aggressive based on the pre-COVID-19 competitive employment market. Post pandemic, that number could also serve as a way for employers to “responsibly detach” themselves from costlier, direct insurance provision in a more uncertain, less competitive employment market – literally “passing the buck” to the individual exchanges.

6. To combat premium volatility and overall uncertainty in the fully-insured market, expect further growth in self-funded plans, or level-funded plans, in the smaller end of the market. Currently, 21 percent of small group and 26 percent of employers with 50-199 lives respectively are in either a self- or level-funded plan. Going forward in unchartered waters with potentially volatile and high premium growth, these types of plans provide stability with a back-stop (stop-loss insurance) to protect employers financially.

7. More government regulations will help employers get back on track, impacting mix shift and product offerings. Mini-med plans, for example, could return for those requesting and receiving waivers from ACA requirements. Additionally, there could be multiple government incentives for small businesses to offer benefits or promote more heavily revamped Small Business Health Options Program (SHOP) exchanges (depending on November election results, the nature of this legislation could vary significantly).

8. Direct-to-carrier distribution. We estimate a potential uptick in direct contracting with carriers for small group and middle market, bypassing the broker distribution channel. Currently, only about seven percent in these markets engage in direct contracting with carriers. But, this rate could increase as carriers and employers look to save costs, and technology / enhanced web marketing makes it easier to reach potential customers. We’ve already seen commission rate declines in the small group sector, with over two-thirds of the market being compensated on a flat fee Per Employee Per Month (PEPM). (Note that commission rates decline during recessions.) Add potential carrier partnerships with benefit/admin platform players and direct to carrier could increase further. In the smaller end of the market, Professional Employer Organizations (PEOs) will have a greater presence. This may be particularly true in the sub-100 lives market. PEOs will be looking to expand outside their traditional target customer zones. Increase in informal “quasi” partnerships with brokers are likely as well, to help each other capture additional revenue streams.

9. As we edge ourselves into a new normal, brokers will still be, by far, the greatest influencer of benefits buying decision-making for smaller employers. Some are partnering with benefit administration players, along with carrier partnerships/ownership. Increased digitization and a contracted insurance market may impact broker margins and therefore employment. We’ve already seen an enormous wave of consolidation via retirements and merger & acquisition (M&A) activity. Less tenured brokers will experience even higher turnover. But brokers are resilient and will continue to enhance these services to prove their worth in these uncertain times.

10. Increased carrier churn is likely in the future. During the crisis, there may be a spike in one-year extensions for 2021 insurance, as groups cannot handle the admin load of running new Requests for Proposals (RFPs). And much of the 2021 pricing and features are close to being locked in, potentially stifling near-term innovation. For the 2021 and 2022 plan years, employers will be pressing brokers even harder to find value deals. And brokers will be looking to carriers to provide the innovative products the new normal demands.

For more information, we invite you to read our full series, “Is There a New Normal in Commercial Health Insurance?” (Part 1),“The Potential New Normal in Insurance Products” (Part 2), and “What A New Member Mix Means for Payers” (Part 3).