Is There a New Normal in Commercial Health Insurance?

Editor’s Note: The following article is part of an ongoing series offering our strategic advice and expertise on what healthcare industry stakeholders should do immediately in response to the rapidly evolving novel coronavirus (COVID-19) pandemic. This is Part 1 of a three-part series. Read “The Potential New Normal in Insurance Products” (Part 2) here, where we discuss product and distribution implications amidst our “new normal” and will share an updated model output. In "What A New Member Mix Means for Payers” (Part 3), we explore what recovery scenarios of the future may look like. This article was last updated on May 6, 2020. Since publication of this article, the national unemployment has spiked to 25 percent as of April 8 (defined as the number of jobless with and without unemployment insurance).

We live in unprecedented times where nothing is normal. Times Square is empty. Sports are canceled. Toilet paper has practically become currency. Uncertainty looms. And Wall Street hates uncertainty.

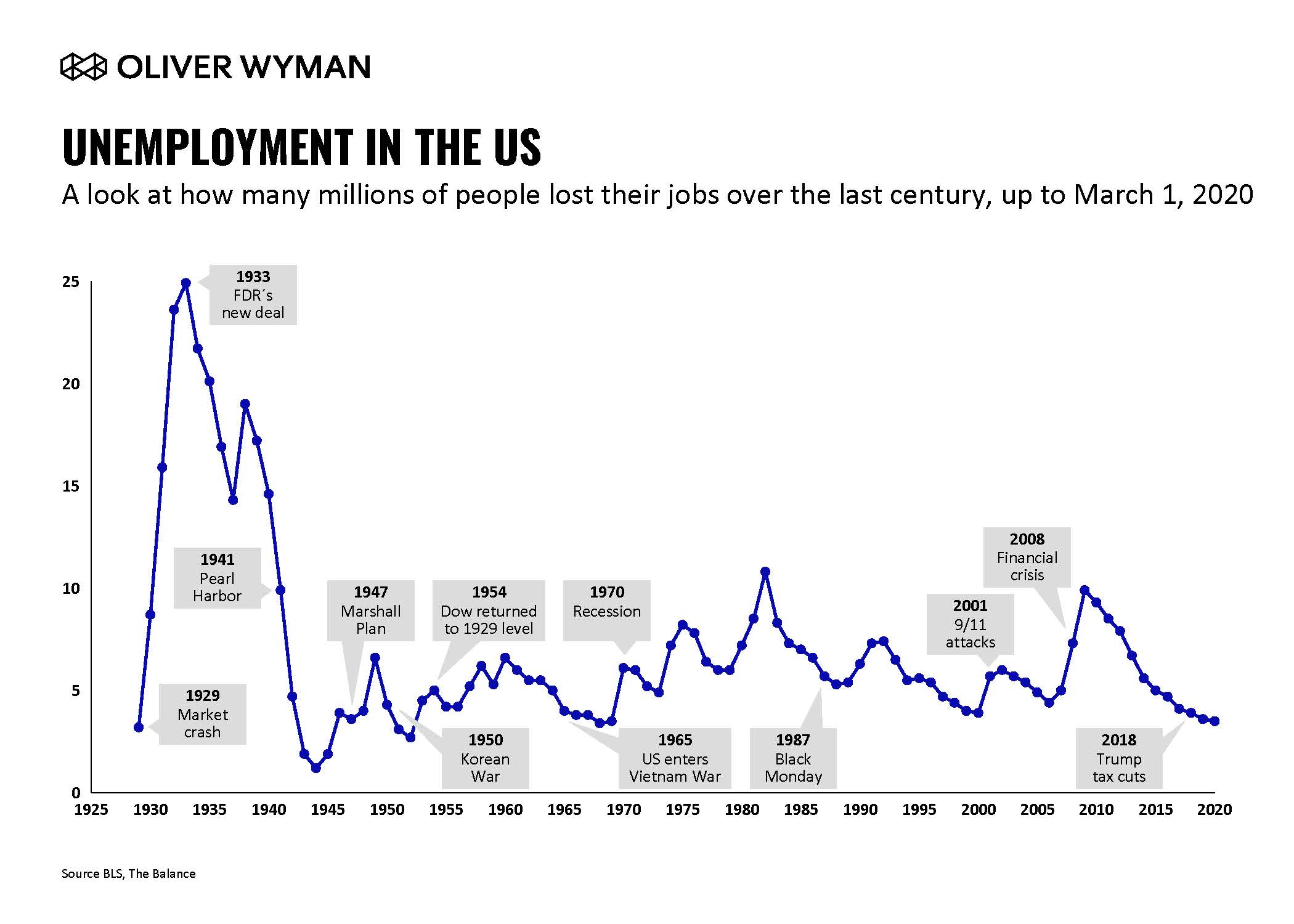

In the past, global equity markets have powered through viral outbreaks. But this time is different. The US Department of Labor cited a record-breaking 6.6 million unemployment claims filed last week. This number is nearing the number of jobs (7.5 million) lost over three years during the last financial crisis.

Not since 2008’s Great Recession have markets tumbled so fast. As of April 1, the Dow sunk from a record high of nearly 30,000 to nearly 20,000 – losing a third of its value in less than 30 days. How bad it will get, and how long it will take to recover is, again, uncertain.

“This is a unique situation. We have nothing comparable to look back on.”

As more people either lose their jobs or become furloughed without pay until further notice, a few questions remain: What is the future of employment and health insurance covered lives? How many of the 160 million covered lives – nearly half of all Americans – will drop off employers’ rolls and switch to the Affordable Care Act (ACA) exchanges, go on Medicaid, or become uninsured? How many Small Group employers will drop coverage altogether? What will be the business shift and revenue impact on payers be? What does this mean for potential new products, required sales, and service model realignment? Will the government step in and heavily subsidize the Consolidated Omnibus Budget Reconciliation Act (COBRA), like in 2009? Will there be an eventual return to status quo coverage levels? Or will tomorrow’s business mix represent a “new normal?”

Expect an Evolving Healthcare Insurance Mix

We may move from 50-year low unemployment of 3.5 percent at the beginning of March, to somewhere between 9 percent and 30 percent by year’s end.

Our preliminary modeling describes this output in more detail further in this article in terms of mix shift and carrier revenue impact. Since estimates change daily, we have utilized unemployment rate ranges, the key lever. Our assumptions are based on current and speculated future employment conditions, those industries and employer segments hit hardest, and emerging legislative moves (such as the CARES Act).

What’s also unprecedented territory is the commercial mix shift. Factors include income levels and qualifications for Medicaid/The Children’s Health Insurance Program (CHIP) this year, which vary by state, and the timing of when someone loses his/her job. The relief package passed by Congress last Thursday morning extends unemployment benefits an extra 13 weeks, which will impact the growth of Medicaid and the level of subsidy received on the ACA exchanges in 2020.

Small business loans may have an impact, too. There is also speculation of premium holidays for Small Group customers to prevent coverage drops. In future rounds of support, we may see Congress enact a COBRA subsidy, for instance, as they did during the financial crisis.

Making Decisions Today Based on Yesterday’s Great Recession

During the Great Recession, 7.5 million jobs were lost over three years, with 2010 unemployment peaking at around 9.5 percent. Goldman Sachs estimates we will hit 15 percent unemployment by the end of the second quarter (but with a potential steeper “V” shaped recovery by end of the year).

Between 2008 and 2011, the workforce dropped by 5 percent, or by about 7.5 million lives over three years. Interestingly, health insurance offer and participation rates during this period remained remarkably consistent across group sizes, from the high 90s for employers with over 200 people to around 47-50 percent for smaller group employers, according to KFF data.

Since the Great Recession, health insurance offer rates have remained high for large employers, declining only slightly for Small Group (by about 3 percentage points), due mostly to the ACA’s onset and continued insurance cost increases. Since 2000, including during the Great Recession, premium increases have averaged around six to seven percent per annum. Also, the growth of self-insurance as a percent of total lives covered has been flat since 2010 at about 60 percent of the workforce.

"This would be the first recession since the ACA went into effect, so we are in somewhat uncharted territory in terms of what might happen in a recession under both the ACA marketplace and the Medicaid expansion."

But, here in 2020, things look much different than they did in 2008. For instance, there’s now potentially much higher unemployment happening across the board. Small businesses are being hit particularly hard, and quickly. We are currently seeing big layoff spikes with a potentially steady increase throughout the remainder of the year.

And, whole industry sectors, from airlines to hospitality to restaurants to retail, are being wiped out. Even if there’s pent up demand (as some politicians speculate) we believe consumers will be cautious and budget-conscious (don’t schedule that November conference yet). Typically during past recessions, recovery time took two to three years, even in major events like the 2008 mortgage crisis. This time around, there is some hope for accelerated recovery, but as many voices touting a prolonged escape.

Consider also that after 2011, the overall status quo was largely unchanged. This time, “new norms” could be established, like less business travel, more digital learning, and the like. For example, Zoom’s market cap is currently eight times more than some of our biggest airlines. Silver linings exist. But the implications for how consumers interact with healthcare going forward, and how they’re covered, could be pronounced.

Commercial Lives’ Insurer Impact

To kick things off, an unemployment spike could prompt a major drop in insured lives. We could see over 40 million jobs lost in the next six months, if you believe the March 30th 32 percent unemployment projection from the St. Louis Fed. Those hardest hit will certainly be in the small group sector.

Speaking of small group, for the first time in 20 years, we could see a significant drop off in offer rates by small group insurers. In our recent small group employer research conducted just before the COVID-19 outbreak, we saw strong resiliency in the small group sector across industries. Many respondents said that in a “recession,” employers would protect benefits, even foregoing bonuses and increasing cost-sharing. But, COVID-19 is an entirely different magnitude.

We will see a significant uptake on the ACA exchanges and Medicaid. There is currently discussion, however, of subsidized COBRA coverage like during the 2008 recession (employees pay the whole amount currently), which could dampen the uptake of individual and Medicaid coverage.

Premiums could increase significantly. In California, for example, the Covered California head recently warned of premium increases of 40 percent. That could be a shot across the bow. The Department of Insurance (DOIs) could, for instance, push back and/or the Feds could increase the subsidy (kicking the can down the road for taxpayers). In the meantime increases could certainly be greater than the historic six to seven percent, forcing a further jump in the uninsured.

Cost shifting could resume and intensify. We saw a bump in cost-shifting during the last recession (from 27 percent of the total premium for family coverage in 2008 to 30 percent in 2010), for instance. But the cost burden has been constant in the past several years as employers were reluctant to push too hard here, especially in a booming economy with low unemployment. Look for that to increase across the board during this pandemic era.

On that note, the gig economy has been relatively steady and flat in recent years. The number of gig workers could increase based on a new work-from-home, flexible workforce economy. This also means a further increase in individual, non-subsidized coverage.

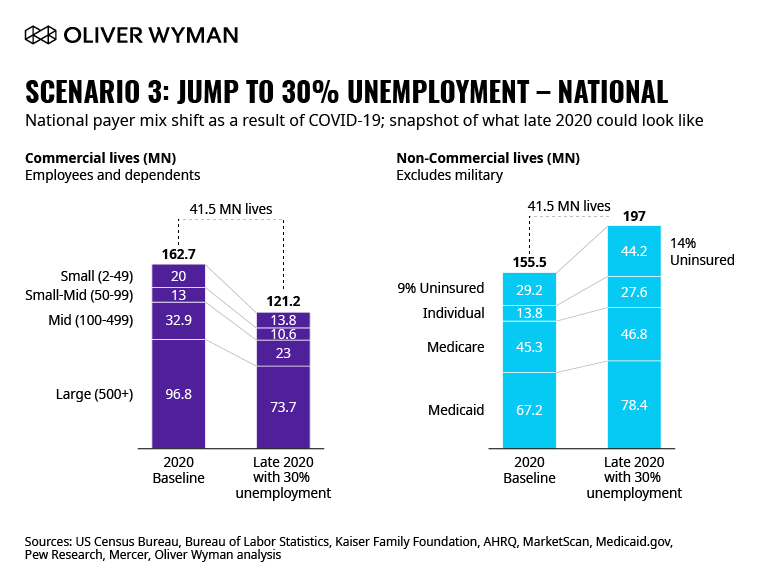

Three Scenarios of Unemployment

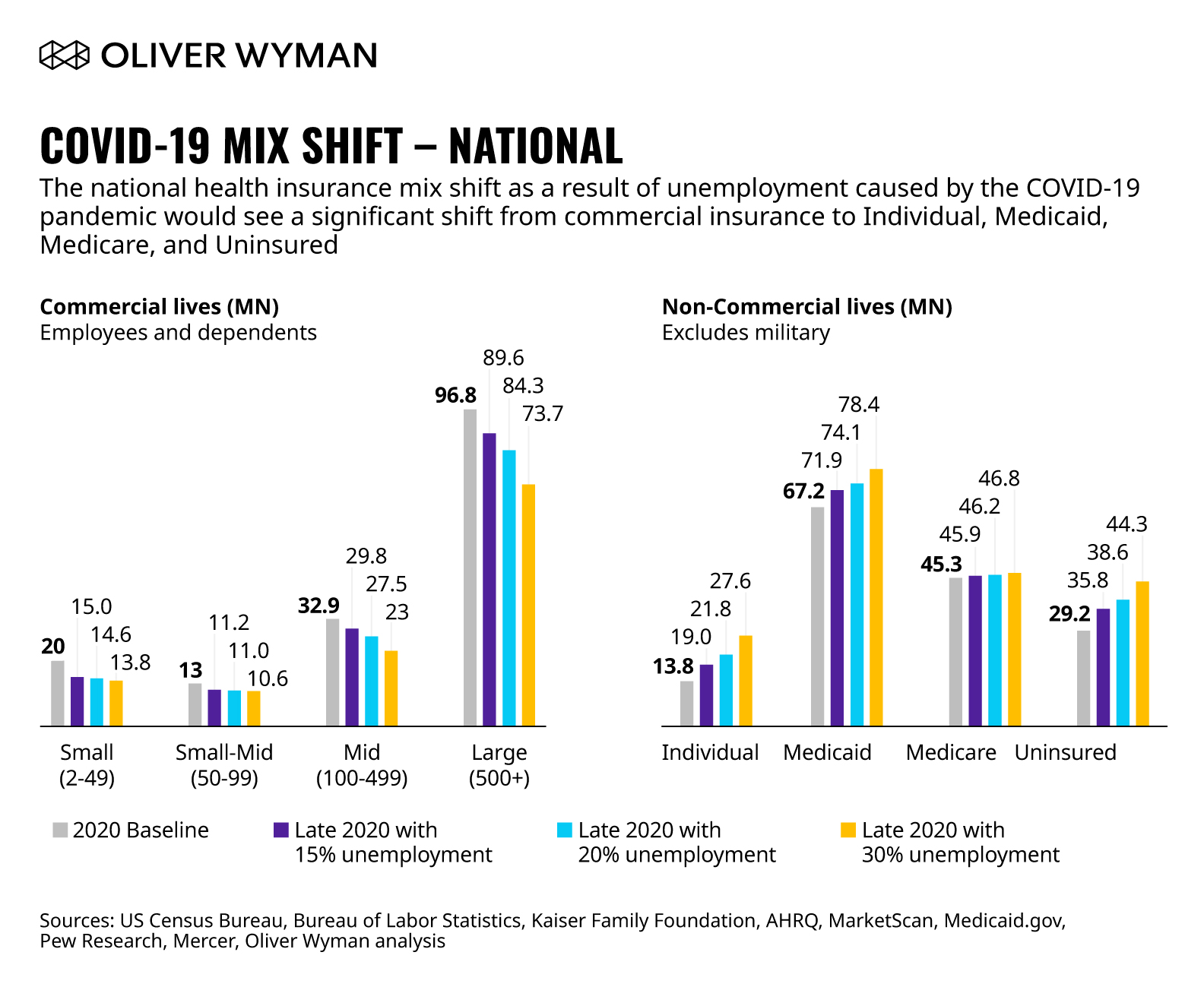

When predicting revenue impact on the greater health insurance industry, expectations may not meet reality. As lives shift out of the employer segment, Administrative Services Only (ASO) lives are shifting into fully insured segments in the Individual and Medicaid markets, meaning overall market-wide premium revenue may increase in higher unemployment scenarios. What matters then is each payer’s access to the now-growing Individual and Medicaid segments, and profitability by segment, which will likely show the risks payers face with this mix shift.

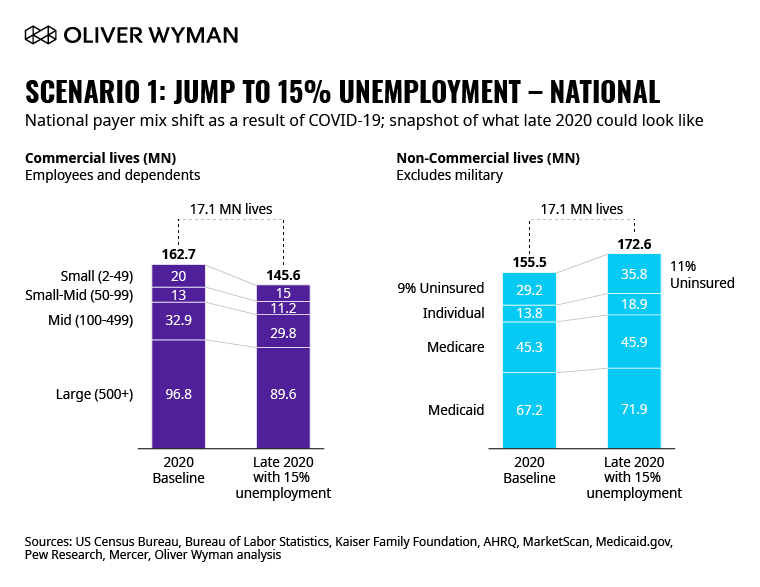

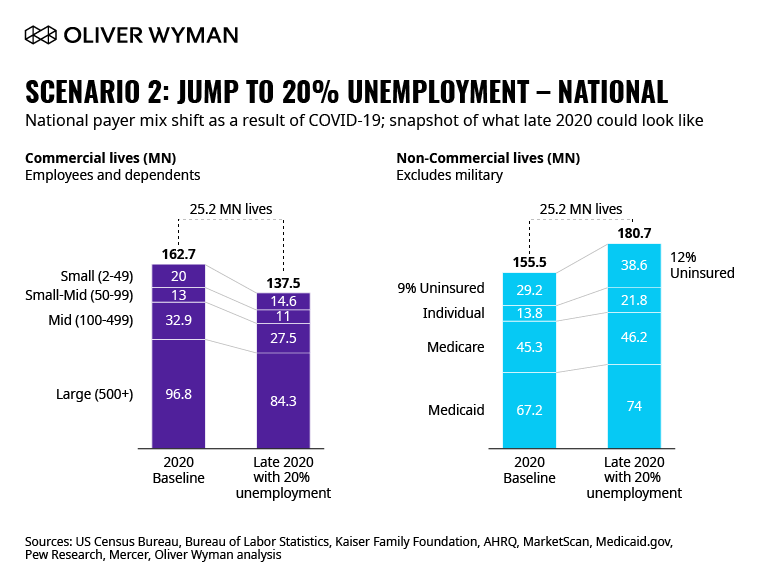

As highlighted above, we have built a model to track the impact of the COVID-19 crisis on the payer mix, as well as the corresponding revenue / top-line impact, for the payer industry, nationally. Think of this model as a snapshot in time of how insured lives could shift in three unemployment scenarios (10 percent, 20 percent, 30 percent) by the end of 2020 as a result of the COVID-19 pandemic. We chose late 2020 to model because this is the time after existing furloughs. The model takes into consideration the CARES Act relief programs, but before any legislation that impacts 2021 open enrollment decisions would be in effect. We also assume an ongoing recession with a traditional recovery time of several years, meaning unemployment will still be high in late 2020.

What Does This Mean?

As is clear from the charts above, we are seeing tens of millions of lives migrating out of the commercial market and into the individual and Medicaid segments, as well as forgoing insurance. This means payers who are heavily weighted towards commercial lives – particularly those with a greater portion of small group lives that are more likely to be impacted by the recession – are at risk of seeing significant membership loss. On the flip side, those with exchange and/or Medicaid businesses could see a heavy influx of members this year. For those, the keys to success will be capturing those members as they shift, and also finding a way to be profitable in those segments.

Regardless of how you read the above output, its impact is significant. Current pundits estimate unemployment could rise as high as 30 percent as a result of the COVID-19 pandemic – to put that in perspective, unemployment only reached 10 percent in the Great Recession, and 25 percent in the Great Depression. With such high unemployment rates, employees – and their dependents – who are currently getting their insurance through their employers are increasingly going to shift to the individual market, Medicaid, their spouse / other parent’s insurance (if available), or go uninsured. Children, of course, would be eligible for CHIP.

Note that, in our scenarios, the uninsured rate goes from 9 percent to 11 percent, 15 percent, and 18 percent in Scenarios 1-3, respectively. The uninsured rate in 2010 was 16 percent, but that was pre-ACA. So, we consider this model relatively conservative regarding how high the uninsured rate could go, assuming the ACA individual market is there to catch a significant chunk that otherwise would have gone uninsured.

The results of this member mix shift for the payer industry overall are not necessarily bad from a revenue perspective. As lives shift out of the employer segment, ASO lives are shifting into fully insured segments in the individual and Medicaid markets, meaning overall market-wide premium revenue impact is mitigated in higher unemployment scenarios. What matters then is each payer’s access to the now-growing individual and Medicaid segments, and profitability by segment, which will likely show the risks payers face with this mix shift.

Of course, the mix shift and revenue implications of the anticipated unemployment rates for health insurers are ever-evolving as Congress considers new legislation each day the crisis continues. We will continue to update our model as new legislation and data become available.