Health Insurer Financial Insights Vol. 3

Editor's Note: The following is a summary of findings from Oliver Wyman's "Health Insurer Financial Insights, Volume 3."

This article is about market profitability and capitalization trends for public and non-public health insurers, their claims experience through the first half of 2020, and insights into how health carriers are reporting the impact of COVID-19. Our aim is to keep you abreast of key market trends and dynamics that impact health insurer financial results and profitability.

2nd Quarter 2020 Year-to-date Statutory Financials: Individual, Group, Medicare, and Medicaid Markets

We summarize the reported profitability trends of carriers with statutory financial information through June 30, 2020. We also summarize enrollment and loss ratio trends in the individual, group, Medicare, and Medicaid markets. Overall, reported pre-tax margins increased in for the first half of 2020 to 5.9 percent versus 2.6 percent in 2019 with decreased loss ratios due to the impact of COVID-19 lockdowns.

.png)

2nd Quarter 2020 Reported Claims Experience

We compared the reported per member per month (PMPM) incurred claims in the second quarter of 2020 to expected claims based on the first quarter of 2020, and reported PMPM claims and typical historical growth patterns from the first to the second quarter to highlight the impact of COVID-19 on developing claims experience. The lower than expected reported claims in the second quarter of 2020 are clearly visible in the chart. This reduction is attributable to reduced utilization during the COVID-19 pandemic.

.png)

We summarized the reported data by major lines of business: individual and group comprehensive, Medicare Advantage, Medicare supplemental, Medicaid, and dental. Across all lines of business, the reported PMPM claims in the second quarter of 2020 were about 11 percent lower than expected, or ($38) on a PMPM basis.

The difference in the reported and expected change in reported PMPM claims from the first to the second quarter of 2020 ranges from about nine percent for Medicare Advantage to 42 percent for dental. In column six of the table, the reported less expected claims difference is the lowest for Medicare Advantage (9 percent) and Medicaid (10 percent) and the highest for Medicare supplement (18 percent) and dental (42 percent). In the comprehensive individual and group lines of business, the reported to expected differences are slightly higher than the average at about 13 percent and 14 percent, respectively. The differences by lines of business indicate that COVID-19 has a larger impact on dental than on major medical and Rx services provided with comprehensive coverage.

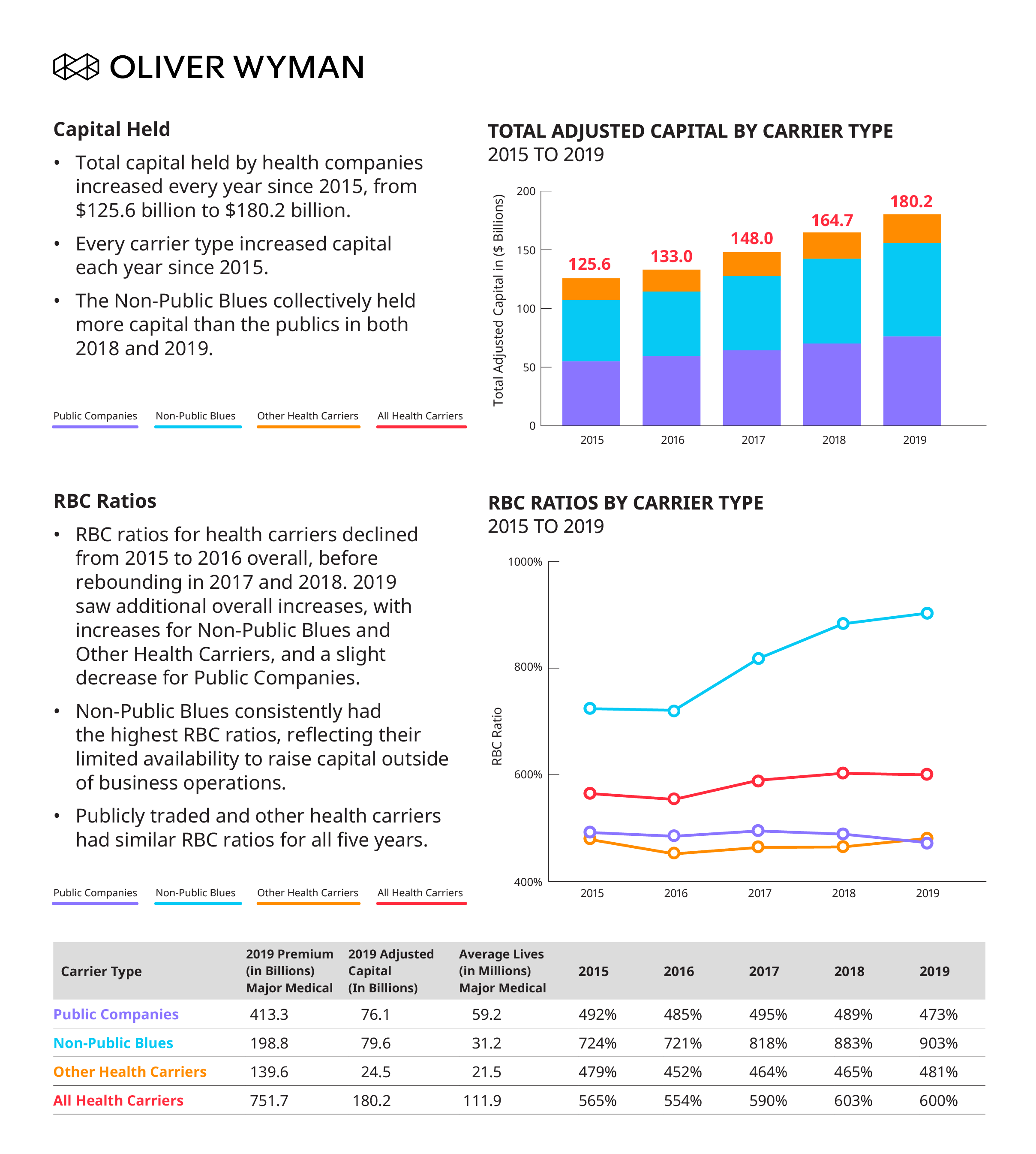

Market Capitalization: Statutory Capital/Risk-Based Capital (RBC) Trends

Market capitalization measured by Total Adjusted Capital (TAC) increased due to small increases in the size of the market (measured by premium), and very little total change in RBC ratios. Overall, public companies saw minor decreases to their RBC ratios in 2019, while non-public Blues saw increases in both TAC and RBC ratios.

Public Companies' Financial Performance

Public companies continue to perform well. We reviewed the profitability for the insured blocks of business and noted that margins remained strong, as loss ratios improved in 2020's second quarter due to COVID-19.

COVID-19 Impact Carrier Insights

The first confirmed case of COVID-19 in the United States was reported on January 20, 2020. Since that date, the virus has spread rapidly and driven dramatic changes to the healthcare landscape. Second-quarter earnings calls provide some insight into how health carriers are viewing the impact of COVID-19 on healthcare costs, utilization patterns, membership, and how they are assisting their customers during this difficult period.

Direct Costs

The costs associated with COVID-19, according to organizations' second-quarter earnings release call transcripts, labor statistics, and press releases, include those for testing and treatment associated with COVID-19-related diagnoses.

- Anthem: To date, they have paid $500 million associated with COVID-19 related diagnoses

- Centene: Through the end of June, they have paid approximately $550 million associated with COVID-19 claims

- Humana: Projected annual COVID-19 testing and treatment costs of $600 million

- Molina: Just over 4,100 hospitalizations with an average inpatient episode cost of $9,000, plus the cost of outpatient and other professional services

Utilization

Generally, COVID-19 began to impact utilization run rates in the second half of March 2020. Utilization further declined in April before seeing a slight rebound in May and approached normal levels in June based on carrier estimates.

- Anthem: Aggregate utilization was 40 percent below expectations in April, 20 percent lower in May, and recovered to 90 percent of baseline in June

- Centene: Volume began to return in May and June was virtually a normal month – with the recent surge in the virus, there appears to be some decline in utilization in July

- Cigna: Utilization was 30 to 35 percent lower in April, 20 to 25 percent lower in May, and closer to normal in June at approximately zero to five percent lower

- Humana: Decline in medical utilization of at least 30 percent during the last two weeks of March and through most of April. In late April and throughout May, utilization began to rebound. In June, it was approximately 10 percent below normal levels, excluding COVID-19 utilization. In July, the non-COVID-19 inpatient utilization remained flat to June, but COVID-19 testing and treatment costs were a bit higher than June.

- Molina: Significantly lower utilization in cost categories representing approximately two-thirds of total spend with utilization levels increasing slowly as the quarter progressed.

- UnitedHealth Group: At the lowest point in April, inpatient care – inclusive of COVID-19 related care – was about three-quarters of baseline, whereas outpatient and physician services fell to roughly 60 percent of normal levels. In June, inpatient care recovered to nearly 95 percent. Outpatient and physician services were tracking above 90 percent. These national trends have continued thus far in July, even as certain states are seeing short-term deferral of services where there are elevated levels of infection and hospitalization.

Membership

During the second quarter, the pandemic drove the unemployment rate to a high of 14.7 percent in April. This rate decreased slightly throughout the rest of the quarter ending at 11.1 percent. The shift in enrollment from commercial to Medicaid markets was lower than expected. However, those in the industry seem to believe there may be a larger shift once the increased unemployment benefits from the CARES Act (The Coronavirus Aid, Relief, and Economic Security Act) expire.

- Anthem: Attrition in commercial business has been less than expected to date. However, attrition is likely to accelerate when federal assistance expires.

- Centene: In April, they raised 2020 revenue guidance by $6 billion, including $4 billion in COVID-19-related membership growth. This has been reduced by $0.5 billion as new membership is now expected to peak in November instead of August. The midpoint of the projected year-end unemployment rate is 10.3 percent.

- Molina: Medicaid membership increased sequentially by 152,000 members in the quarter, a five percent increase, due to the suspension of redeterminations. It's believed unemployment-related enrollment has not yet materially accessed managed Medicaid. Through the first three weeks of July, Medicaid membership continued to grow by about 30,000 members.

Customer Assistance

Health insurers used a variety of methods to provide relief to customers, including premium credits and the waiving of cost-sharing for COVID-19-related costs. Some carriers also chose to accelerate payments to their provider partners who have experienced cash flow issues.

- Anthem: Provided one-month premium credit, ranging from 10 to 15 percent to its individual and employer group customers, in addition to a 50 percent credit for those in their dental plans.

- BCBS of Massachusetts: On August 5th, they announced $101 million in premium relief and anticipated rebates to customers and members. This brings their total commitment to $217 million (including $116 million that it has invested to support members, customers, clinical partners, and the community). Credits will be applied in September for FI employer groups and members including under-65 direct pay and Medex members. This will total 15 percent of their May premium. Before the end of 2020, Medicare Advantage members will have a one-month “premium holiday."

- Cigna: They are waiving all cost-sharing for COVID-19 testing and treatment and for Medicare Advantage in individual and family plans. They are additionally waiving cost-sharing for in-office and telehealth visits for primary care, specialty care, and behavioral health.

- Humana: Constituent support will amount to around $2 billion by year-end.

- Molina: Refunds amounted to $75 million pre-tax and related to the states of Ohio, Illinois, California, South Carolina, Mississippi, and Washington.

- UnitedHealth Group: They are waiving all consumer COVID-19 diagnostic and treatment costs, accelerating $2 billion in needed funding to care providers, providing over $1.5 billion in direct consumer and customer assistance, including premium forgiveness and suspension of member cost-sharing, to help people manage their health conditions.

For more information on the above findings, read the entire third edition of "Health Insurer Financial Insights" here.