After two years of turmoil, the aviation industry appears to be poised for a decade of growth. But unlike the last decade, which enjoyed steady annual increases in demand, the next 10 years are apt to be filled with a multitude of challenges that will test the industry’s resilience.

COVID-19 continues to torment airlines and aerospace as well as the global economy in general despite effective vaccines. While a significant portion of domestic air travel demand around the world has recovered and the fleet is growing again, the unpredictable nature of COVID-19 and its variants remains the industry’s biggest immediate obstacle to business as usual. The rapid spread of Omicron at the end of 2021 set in motion a variety of complications for the industry from absenteeism in the workforce, to government travel restrictions, to disruption of the supply chain, to name a few.

There is optimism that the industry has turned the corner and is now on an upward trajectory — but the next 10 years will be filled with a multitude of challenges that will test the industry’s resilience unlike ever before.Brian Prentice, Partner

There is optimism that the industry has turned the corner and is now on an upward trajectory — but the next 10 years will be filled with a multitude of challenges that will test the industry’s resilience unlike ever before.Brian Prentice, Partner

Even so, as we enter 2022, there is cautious optimism that the industry has turned the corner and is once again on an upward trajectory, thanks to widespread dissemination of vaccines, government stimulus, and pent-up demand for travel — at least in developed economies. By the early part of 2023, global demand for domestic travel is expected to reach and exceed its 2019 pre-pandemic peak. From there, the outlook is for steady growth through the rest of the decade at rates that even exceed expansions in gross domestic product.

Worldwide, the business and international travel segments, on the other hand, will take longer to recover, restricted by corporate and government policies unlikely to be fully lifted until COVID-19 transitions into an endemic disease. But it was not just restrictions that took a bite out of corporate travel.

Videoconferencing and a mounting recognition that people can conduct business without being face to face has had an impact. In the foreseeable future, sluggish business travel recovery is apt to put a cap on both airline profitability and growth, but the potential for lower long-term corporate demand exists.

For international travel, the biggest impediment has been and will be the disparity between cross-border rules and vaccination coverage. Globally, a slow recovery in this segment will limit the number of widebody aircraft in the fleet for years.

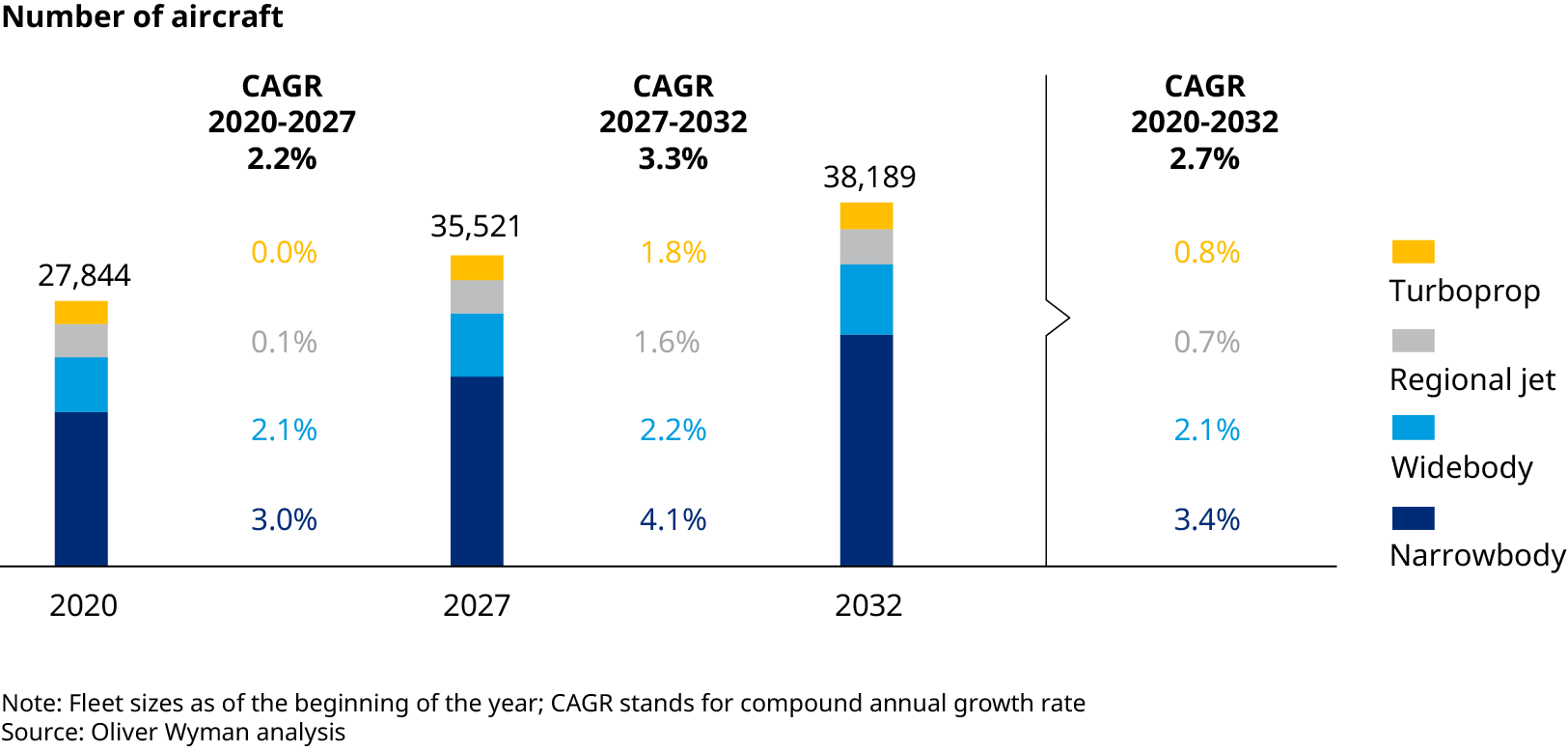

At the beginning of 2022, the global fleet was the same size as it was in 2017, and it is not expected to top its January 2020 apex of almost 28,000 until sometime in the first half of 2023. By 2032, the fleet is expected to eclipse 38,100 aircraft, a compound annual growth rate (CAGR) of 4.1% between January 2022 and the beginning of 2032.

Because of the slower return of international travel, most of the fleet recovery will be in narrowbody aircraft, which will make up about 64% of the fleet by 2032 versus 58% in January 2020. While narrowbodies are expected to recover to pre-pandemic levels by midyear, much of the increase initially will be from aircraft being brought out of storage or the delivery of aircraft in manufacturers’ inventory. Before COVID-19 struck, the industry was struggling with the 2019 worldwide grounding of the 737 MAX — more than 400 of which had been built but not delivered at the time the pandemic shut down air travel in 2020.

While most of the fleet is a story of recovery, cargo is a story of growth. A 17% increase in shipments in 2021 over 2019 — thanks in part to COVID-related online shopping — pushed the cargo fleet to expand during the pandemic. In 2021, the number of aircraft dedicated to cargo grew 3%, and the conversion of passenger aircraft to freight use broke records.

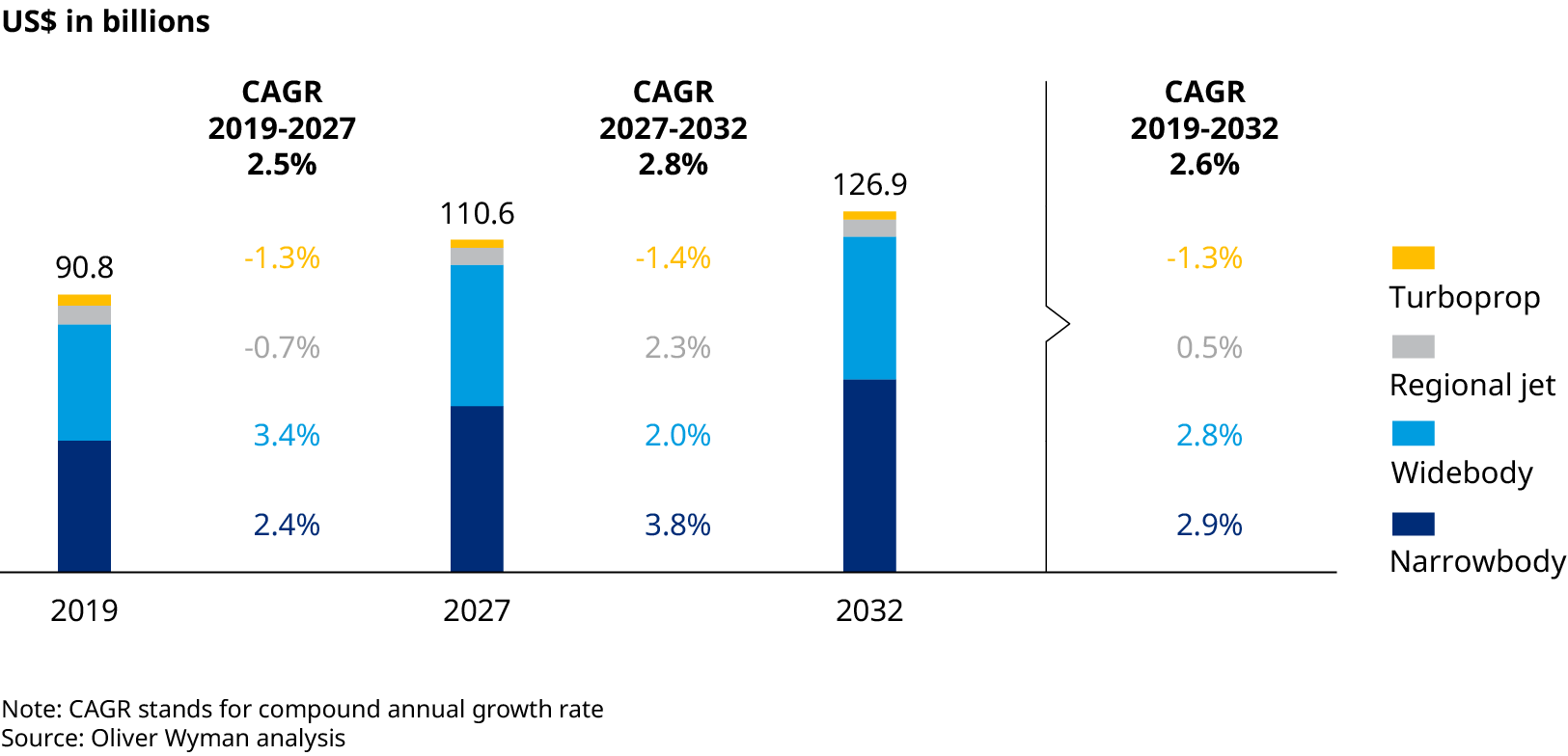

For the maintenance, repair, and overhaul (MRO) sector, the market is being redefined by a fleet in transition, in part because of higher numbers of retirements of aircraft due to enter a period of intensive MRO expenses. MRO demand should recover to pre-COVID levels by 2024, but annual growth in the second half of our 10-year forecast period will be 2.8%. By 2030, MRO demand is expected to reach $118 billion, 13% below the pre‑COVID forecast of $135 billion.

The slower growth projections won’t apply everywhere around the world. For instance, the active China-based fleet and its MRO demand had already exceeded pre-pandemic levels by the end of 2021. Other regions like Western Europe will not see MRO demand recover until 2025.

As unimaginably bad as COVID-19 has been for aviation, the challenge of the next decade may be almost as disruptive. The industry needs smart strategies to get itself in a better position by the 2030s.Brian Prentice, Partner

Another trend that will reshape the MRO landscape is a potential push toward onshoring of capacity — a direct response to the impact of COVID-19’s unforeseen stranding of some assets with quarantines and its continuing disruption of supply chains. While some of the impetus is expected to diminish as COVID-19 fades, airlines and aerospace manufacturers are likely to want a decent amount of capacity that cannot be taken out of the mix by trade wars or sudden travel restrictions. That translates to domestic maintenance providers.

Beyond COVID-19, there are additional impending risks on the horizon that portend some degree of disruption for the industry.

The first is a labor force potentially too small to support aviation’s anticipated growth. Prior to the pandemic, the industry was already looking at a potential shortfall mid-decade in the number of key aviation workers — pilots and aviation mechanics chief among them. At the time, the pressing problem was baby boomers reaching retirement age and not enough candidates to take their place. The pandemic has exacerbated those demographic trends by encouraging early retirements among airline and aerospace workers uncertain about the career prospects in a sector that COVID-19 almost entirely shut down for months.

Likewise, two years of pandemic also is likely to have discouraged many would-be pilots and mechanics from entering the industry. With demand lagging, the industry hasn’t had to fully confront the problem yet, but that won’t be the case for much longer. Over the next 20 years, Boeing estimates, the industry will need 612,000 new pilots, 626,000 new maintenance technicians, and 886,000 new cabin crew members.

Another challenge facing the industry is climate change. Currently, aviation accounts for about 2.3% of total carbon dioxide emissions — still dwarfed, for instance, by road transport and other economic activities. But the anticipated transition to electric vehicles over the next 10 years is likely to cut road transport’s share of total emissions from transportation and potentially raise aviation’s — an industry without an immediate alternative to fossil fuels. That may increase pressure on the industry and even result in efforts to limit commercial flying.

Despite the fact that aerospace manufacturers have been relentlessly driving for more fuel efficiency almost since the industry’s inception, there is no existing or obvious technological solution for substantially cutting emissions — at least not over the next decade. While research and development are underway on the use of hydrogen or electric engines to power aircraft, the commercial production of such revolutionary aircraft for commercial flight is probably 15 to 20 years off.

Since the potential for more efficiency gains on traditional jet engines appears somewhat limited, the most effective tool immediately available is sustainable aviation fuel (SAF), made from non-fossil feedstocks such as used cooking oil and waste animal fat. While SAF can produce 80% fewer emissions than conventional jet kerosene-based fuels like Jet-A1, currently less than 1% of the fuel consumed by aviation is SAF. Most of the biggest airlines have pledged to increase that percentage to 10% by 2030, but even if sufficient capacity was built in time to produce the necessary SAF, that percentage would still not fully offset the anticipated expansion in air travel. A fuel mix of at least 15% SAF by 2030 would be needed to just keep the industry at its 2019 level of carbon dioxide emissions — far from the halving of global emissions called for at the recent COP26 climate conference in Glasgow, Scotland.

The other problem is SAF’s economics: SAF is three times more expensive than conventional jet fuel for airlines and yet less profitable to produce than the renewable diesel used for road transport and ships. That makes it unattractive to both users and producers. Only substantial government subsidies or tax incentives could level the playing field to encourage sufficient airline consumption, investment in SAF production, and ultimately a reduction in the price difference with conventional fuel.

As unimaginably bad as COVID-19 has been for aviation, the next challenge may prove almost as disruptive unless smart strategies are employed today to better position the industry for the 2030s. While aviation is almost guaranteed to keep expanding over the next decade, its ability to carve out profits and remain sustainable will be much more uncertain, given these challenges.

About the Global Fleet & MRO Market Forecast

The 2022–2032 edition of Oliver Wyman’s Global Fleet & MRO Market Forecast Commentary represents our more than two-decade commitment to the understanding and assessment of the commercial airline transport fleet and the associated maintenance, repair, and overhaul (MRO) market outlook. The commentary is the go-to resource of aviation executives—whether a manufacturer, operator, or aftermarket provider, as well as for those with financial interests in the sector through private equity firms and investment banks.

This year’s research focuses on the aviation industry’s recovery from COVID-19, subsequent growth and related trends affecting aftermarket demand, maintenance costs, technology, and labor supply after a devastating 2020. The outlook reveals significant challenges the industry faces as it develops and expands its recovery and rebound plans.

Aviation's 2022 Recovery Isn't as Robust as Expected

Thanks to a series of exogenous shocks, the anticipated recovery for aviation is not as robust as expected. By January 2023, we now anticipate the fleet to be 1% smaller than the original forecast of around 27,600 aircraft. MRO spend in 2022 will be 6% less, at just under $74 billion. In 2023, MRO spend will be 2% higher.