How the Chinese economy and Ukraine war can affect aviation

Every year Oliver Wyman puts together an analysis of the growth in the aviation fleet and spending on maintenance, repair, and overhaul over the next decade. Once a year was sufficient for the Global Fleet and MRO Forecast — that is, until 2020.

In 2020 and 2021, COVID-19 prompted us to provide frequent updates to keep the industry apprised of the pandemic’s impact on air travel and aerospace. With COVID increasingly in our rearview mirror, we didn’t plan on updates in 2022. This was to be a year of comeback for aviation, but thanks to a series of exogenous shocks, the anticipated recovery is turning out not to be as robust as expected.

After COVID-19 temporarily disabled global commerce in 2020 and 2021, the world’s economy was battered again in 2022 by the Russian invasion of Ukraine, which caused energy prices to spike and created shortages in an array of raw materials, including titanium. This was compounded by unexpected COVID lockdowns in China that led to a slowdown in the world’s second-largest economy and more supply chain disruption. Meanwhile, aviation’s rebound was stifled by widespread labor shortages, particularly in North America and Europe, that prompted flight delays and cancellations.

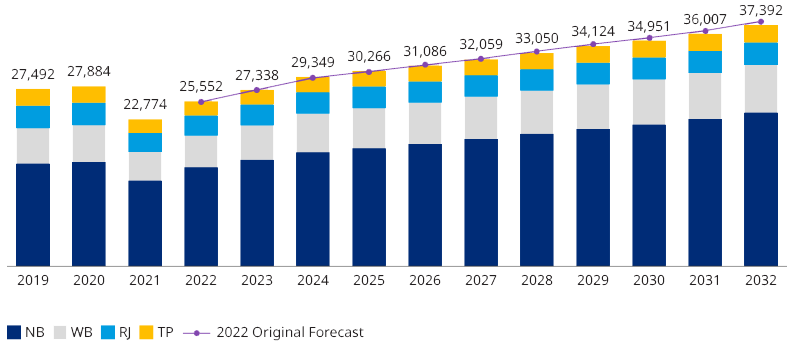

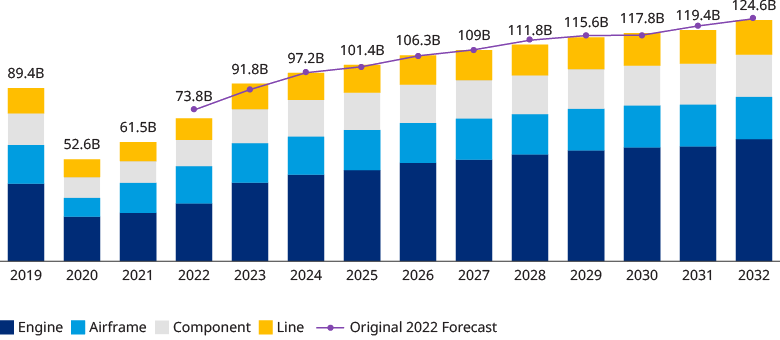

As a result, Oliver Wyman is providing the latest update to our Global Fleet and MRO Forecast 2022-2032 to reflect these unexpected setbacks. By January 2023, we now anticipate the fleet to be 1% smaller than the original forecast of around 27,600 aircraft. MRO spend in 2022 will be 6% less, at just under $74 billion. In 2023, MRO spend will be 2% higher. Over the decade, the growth in both fleet size and MRO demand will trend 1% to 3% less than originally forecast.

Fewer aircraft produced

Driving the small contraction is lower narrowbody production than expected, weaker than anticipated growth and fleet utilization in China, and slower regional jet and turboprop recovery. Forty percent of 2022’s drop in MRO can be attributed to cutbacks in China, Russia, and Eastern Europe.

Because supply chain delays and labor shortages have made if difficult for aerospace manufacturers to ramp up production after COVID shutdowns, production rates for the A320neo and 737 MAX have been 10% to 15% below initial expectations. Deliveries are being pushed into 2023 and 2024.

Ukraine-related sanctions are slowing production on the Russian-built Superjet and MC-21 aircraft, with expectations for little to no production through 2026. The Russian fleet has shrunk 15%, while the rest of the Eastern European fleet has grown 3%.

China’s slowdown

China’s COVID lockdowns and weaker economy are also factors in a less vibrant aerospace forecast. Reinstated lockdowns from the Chinese government have severely limited travel demand. Year to date, China’s domestic revenue passenger kilometers (RPKs) are down 45% versus 2021 levels, according to data from the International Air Transport Association.

China accounts for 15% of the global fleet and 12% of the global MRO market. The size of the Chinese fleet remains 6% above pre-COVID levels thanks to an impressive rebound in 2021, but between January and July 2022, it only grew 1.1%.

In addition, Chinese operators have cut utilization of in-service aircraft. Available seat miles are down 15% from 2021. Lower utilization means reduction in maintenance demand, leading to a 9% decrease in 2022 China MRO spend in our revised forecast.

Another possible sign of slowdown in China’s aviation market: Chinese airlines have 430 MAX on order, including 100 that are already built. The completed aircraft remain undelivered because Chinese regulators haven’t recertified the MAX after its 2019 grounding. The United States, Europe, and other major markets recertified the MAX in 2021, leaving China as the only big market not to bring the aircraft back into service.

Slower recovery for regional jets

The recovery in the regional jet and turboprop fleets has been significantly slower than anticipated as well. The revised forecast projects the size of the regional jet fleet to be 6% down to 3,240 and the turboprop fleet 8% lower at 2,270 in 2023.

Regional jet and turboprop fleets are still only 80% to 90% recovered whereas, narrowbody aircraft have surpassed their pre-COVID levels. Globally, available seat miles (ASMs) for jets with fewer than 100 seats are 74% of their 2019 levels; ASMs for aircraft with more than 100 seats are at 83%.

Over the 10 years covered by the fleet forecast, all regions are within 0.5% or less of the original MRO spend projection. The only exceptions are Eastern Europe including Russia, which is projected to be down 6.4%, and Latin America and the Caribbean, now expected to be 2.4% lower. Between 2022 and 2032, North America MRO spend is now projected to be 0.2% higher and Europe 0.1% higher.

Oliver Wyman is continuing to monitor developments in the market and will release our annual full forecast and commentary in early 2023 for 2023 through 2033.