Medicare Advantage Strategies for Payers in a Pandemic

Editor’s Note: The following article is part of an ongoing series offering our strategic advice and expertise on what healthcare industry stakeholders should do in response to the rapidly evolving novel coronavirus (COVID-19) pandemic.

By 2030, 20 percent of the US population will be over 65 years old. Consequently, Medicare will become a predominant source of health insurance coverage in the US. As health plans prepare for an uncertain post-COVID-19 future, the ability to effectively operate in the Medicare Advantage space will strongly shape payers’ long-term strategies. For many payers, Medicare Advantage is likely to drive future growth and profitability.

The over-65 population presents a unique set of considerations for the healthcare system, including a higher prevalence of chronic conditions, limited financial resources in retirement, and increasing overall life expectancies (among other factors). As a result of the pandemic, additional concerns will affect seniors’ greater healthcare-related decisions – from insecurity around healthcare access to greater price sensitivity.

COVID-19’s heightened impacts on vulnerable senior populations have been evidenced through disproportionately high infection rates, more hospitalizations, and higher fatality rates. A much higher percentage of those with COVID-19 who are senior citizens have passed away compared to those with COVID-19 who are decades younger and have passed away.

The Future of Medicare Advantage

As seniors adapt to the current pandemic environment, they will likely alter their buying and utilization behaviors, from spending more time shopping around and comparing benefits to forgoing choice and flexibility for higher quality and affordable plans that ensure certainty of coverage. Given these idiosyncrasies, payers with membership in Medicare Advantage (as well as those interested in entering the market) should assess how health plans can most effectively structure their Medicare Advantage offerings to support the senior population.

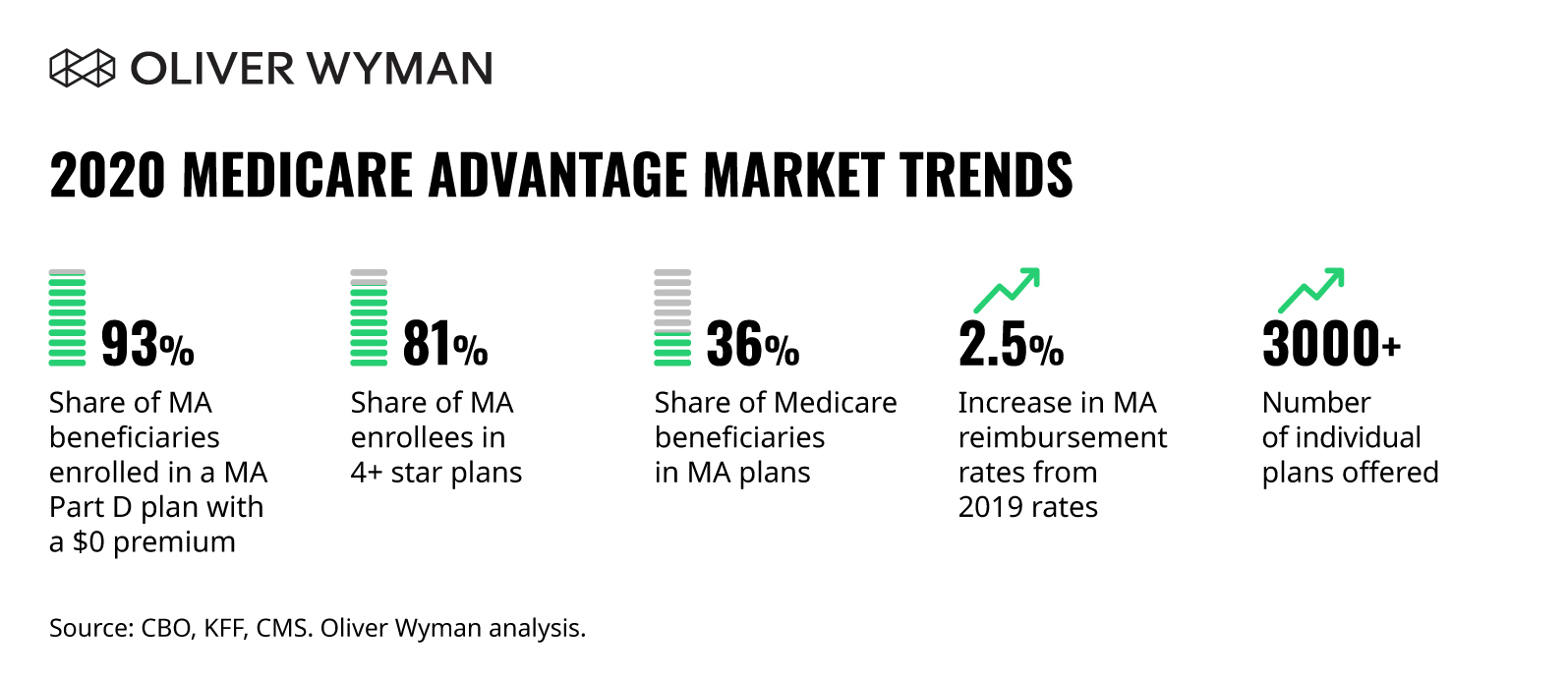

As of last March, over 60 million individuals were enrolled in a Medicare program – with nearly 25 million of these members in a Medicare Advantage plan. In the wake of the crisis and its associated economic fallout, these numbers will almost certainly keep rising. Healthcare plans can bolster their Medicare Advantage offerings to provide affordable and high-quality care at a time when seniors are increasingly turning to the federally subsidized healthcare program for coverage. And, health plans can prioritize their members’ needs while also dedicating resources to a segment likely to provide reliable returns amidst an uncertain healthcare market.

Before the crisis, Medicare Advantage enrollments were growing rapidly. And these plans had taken on a larger role in the Centers for Medicare & Medicaid Services’ (CMS’) Medicare program.

A wide range of COVID-19 response options exists – including lowering enrollment, mitigating risk exposure, and exiting the Medicare Advantage market entirely. Yet, most health plans’ optimal course of action will be to maintain a competitive product portfolio and double-down on their Medicare Advantage offerings to further capture market share.

Particularly for those health plans with existing Medicare Advantage plans, this means staying the course on quality while adapting to changing consumer purchasing behaviors and price sensitivities. Despite the removal of requirements to submit 2020 Healthcare Effectiveness Data and Information Set (HEDIS) and Consumer Assessment of Healthcare Providers & Systems (CAHPS) data, health plans should continually strive for excellence in their Star Ratings by prioritizing provider (like C04 – Improving or Maintaining Physical Health), pharmacy (like D08 – Getting Needed Prescription Drugs) and service (like C25 – Customer Service) interactions to maintain and enhance members’ experiences.

Plans should also strategically optimize medical costs to ensure affordable care. For example, focusing on inpatient hospitalization utilization, high-value diagnosis-related group (DRG) reviews, and emergency room visits analysis among other categories will help build a continuous cost containment culture.

Additionally, plans should consider altering benefits, focusing on high visibility benefits such as low physician copays and specific supplemental benefits that greatly influence buying behavior. This will encourage retention and member acquisition while ensuring sales and marketing reinforce messaging about plans’ value propositions and low costs to attract membership. Payers that strengthen their Medicare Advantage products will perhaps be better positioned to recognize long-term financial and member loyalty gains.

The Evolving Medicare Advantage Market

Oliver Wyman has previously explored how the COVID-19-induced surge in unemployment will result in member mix shift, uncertain product implications, and adverse financial impacts for non-Medicare segments. Medicare membership, however, depends on the aging population. And with 10,000 people nationwide turning 65 every day, the Medicare population growth trajectory is projected to continue unabated. The pandemic is likely to induce an increase in projected Medicare enrollees due to the likely influx of both disabled retirees and individuals retiring earlier than planned.

Within the Medicare program, Medicare Advantage will experience an accelerated rate of growth in the number of members across Medicare Advantage plans, doubly benefitting from the increased membership population described above, as well as increased penetration of the CMS program (including the share of total Medicare-eligible lives). Additionally, we predict some members will migrate from Medicare Supplement plans (Med Supp or Medigap) to Medicare Advantage plans as price-sensitive seniors become more willing to sacrifice breadth of offerings for lower premiums and overall out-of-pocket expenses. That being said, other considerations – such as provider network, product types, and overall consumer experience – will continue to be important for attracting and retaining members.

Considering COVID-19’s Potential Long-Term Implications

Although the current pandemic will not significantly impact future Medicare enrollment, there will be noticeable impacts to the system in 2021 and beyond. Assessment of Stars ratings based on Healthcare Effectiveness Data and Information Set (HEDIS) and Health Outcomes Survey (HOS) measures will likely face significant disruption. Also, the calculation of risk scores for the 2021 pricing year will be difficult given the unusual circumstances. And it is to be seen how CMS reimbursement benchmarks for future periods will be impacted by this year’s disruption. Additionally, overall budget pressures will undoubtedly impact federal programs’ operations.

We may see an increased concentration in the provider market (as some provider segments face insolvency), as well as increased utilization of elective services due to pent-up demand and provider efforts to improve their balance sheets. Additionally, the pandemic has unexpectedly facilitated the use of digital health in a senior population previously viewed as generally being more resistant to novel care delivery models. Medicare Advantage plans in a post-COVID-19 world will likely need to address the senior population’s increased utilization and comfort with remote care by providing access to telehealth and other digital health technologies.

Overall, Medicare Advantage is likely to be strengthened because of the attractiveness of lower premiums over Medigap or employer-sponsored coverage, the value placed on plan sponsorship, and the appeal of consistent provider cash flow. However, health plans should be cognizant of potential losses resulting from a rebound in elective procedures in the future, as well as concurrent non-performance on risk scores.

Activating a Winning Strategy

These considerations should be top-of-mind as your health plan builds out its Medicare Advantage offerings:

- Define value proposition and establish presence: Determine your health plan’s value proposition in the Medicare Advantage market. (What is your “North Star?”) Examples include zero-premium plans, superior supplemental benefits, networks that include popular providers. Then, identify opportunities to expand within existing markets, as well as to enter into new markets. While the attractiveness of Medicare Advantage markets varies considerably based on the market, it remains materially more attractive compared to other segments of the health payer portfolio.

- Focus on the member: The member should be central to your plan and offerings. Align benefit design with patient needs, and provide services aimed at elevating the consumer experience by simplifying the healthcare process.

- Maintain quality of care: Membership will be increasingly driven towards plans offering high-quality healthcare services. While there will be limited quantitative levers due to uncertainty around Stars ratings, continue to focus on quality long-term.

- Manage utilization and medical costs: Employ interventional models of care and develop value-based care partnerships that build outward from the highest-cost patients to create impact.

- Activate sales and marketing channels: Enable sales and marketing channels to proactively outreach members and engage in conversations about future benefits, as well as comprehensively understand member priorities and needs.

Medicare Advantage represents certainty in uncertain times for health plans. Smart payers won’t miss out.