In the aftermath of the global financial crisis, the world entered a prolonged period of declining interest rates known as the “Low for Long” era. The Reserve Bank of Australia cash rate consistently declined throughout the period, bottoming out at 0.10% in November 2020 in response to the pandemic.

This paradigm shifted with the onset of rapid interest rate hikes in 2022, heralding a New Monetary Order. With the first major rate tightening cycle in more than 20 years upon us, it is natural to question how the financial sector and broader economy will be impacted. To understand this, we need to revisit how the Low for Long period has shaped the Australian financial sector and the provision of credit.

Navigating the New Monetary Order — scenarios and impact

While we do not attempt to predict the future, we consider four scenarios to explore how these uncertainties might evolve, and investigate the impact of the New Monetary Order:

Rates and inflation slowly return to normal levels

This "soft landing" would be marked by a benign credit environment, with robust underlying growth of the economy and no significant change to competitive pressures in the lending market.

high rates cause a sharp economic downturn

Deteriorating credit quality and slower growth would spread from higher-risk areas into core home and small- and medium-sized enterprise (SME) lending.

rates and inflation remain higher for longer without causing an economic downturn

private debt fill structural lending gaps

In this scenario, superfunds, asset managers, and global private equity firms would fill structural lending gaps in more specialized lending segments and play a central role in funding Australia’s climate transition.

How Australian banks weathered the global financial crisis

Australia’s financial system has been shaped by two key dimensions since the global financial crisis: monetary policy and regulation, which together created a slightly different experience through the Low for Long period for Australia compared with other advanced economies. Accommodative monetary policy, more conservative lending policies from retail banks, high net migration, and a commodity boom helped Australia avoid a recession following the crisis. As a result, Australia did not reach the near-zero cash rates experienced in other jurisdictions until the COVID-19 pandemic.

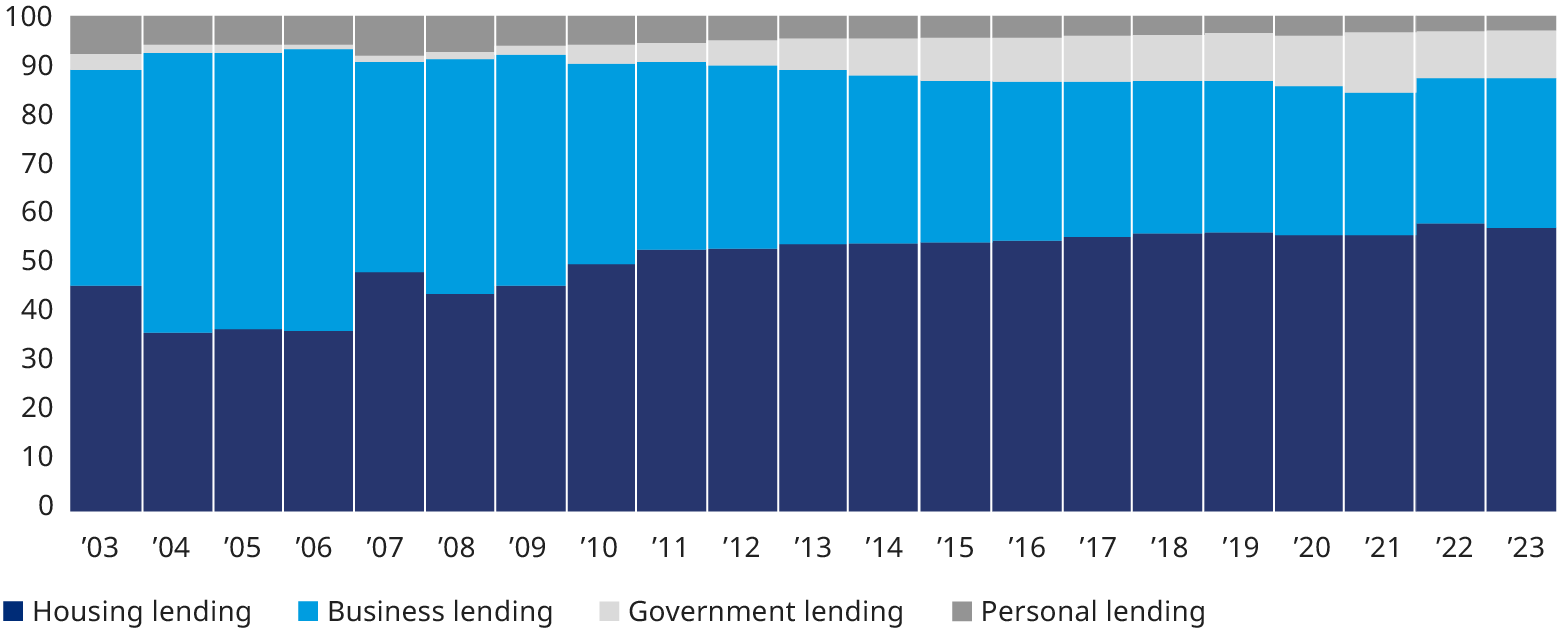

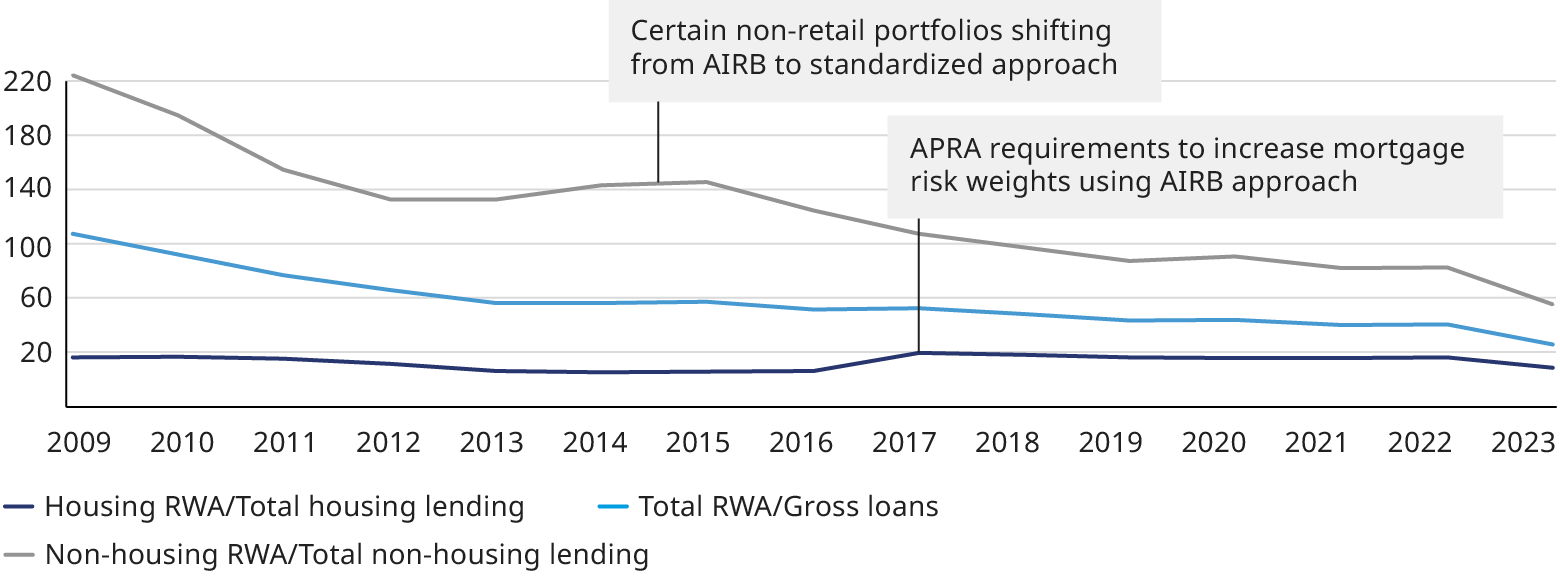

These regulatory changes, combined with monetary policy and other factors, played an important part in reshaping bank balance sheets. Banks doubled down on mortgages, which grew to about 60% of total loan assets, while reducing exposure to riskier portfolios such as commercial real estate and unsecured consumer lending. This portfolio movement shows a steady decline in risk weights since 2009.

Australian banks increase deposit funding during Low for Long

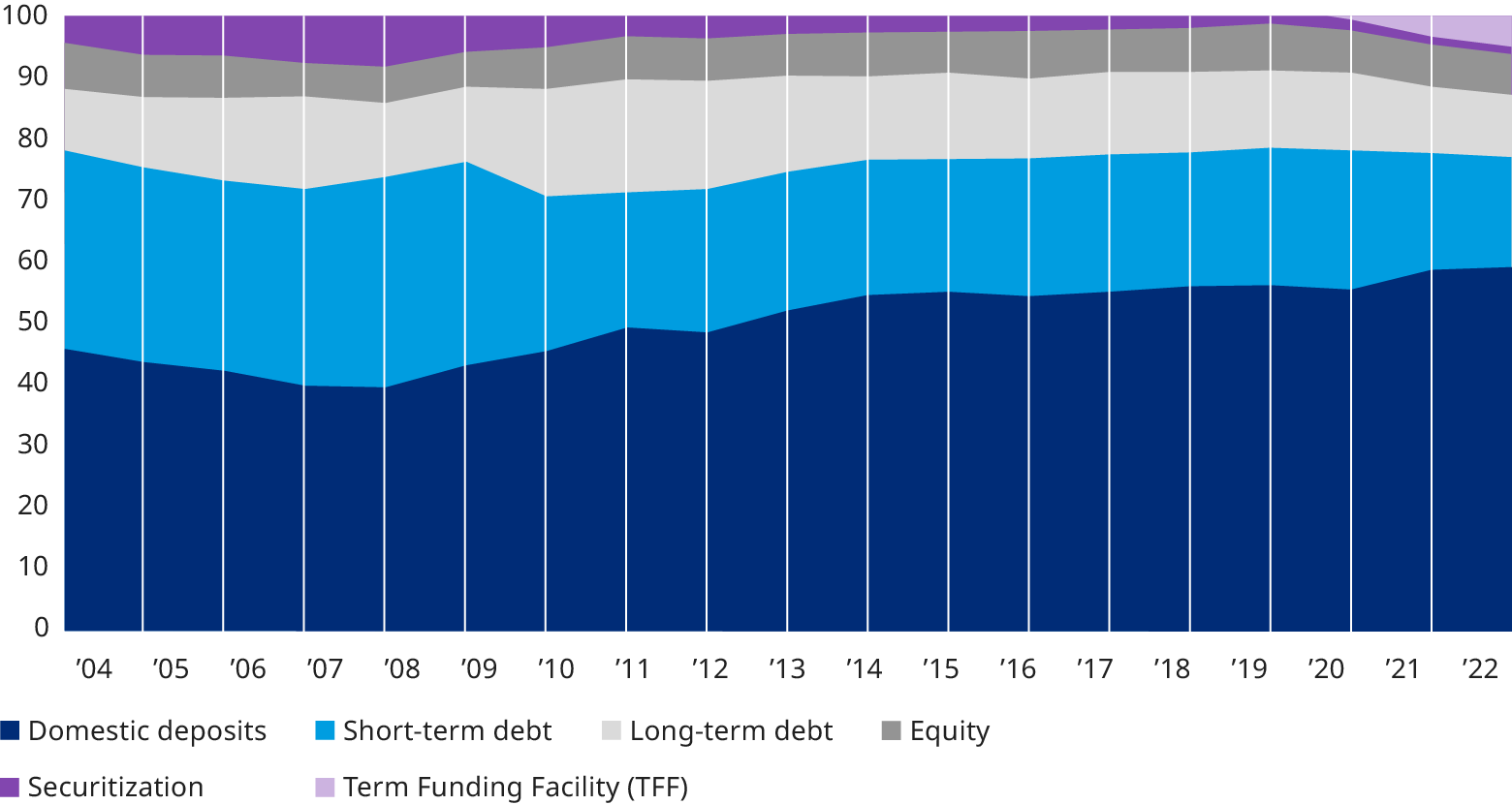

Since the global financial crisis and especially during the COVID-19 pandemic, there has been a significant increase in bank deposit funding, caused by regulatory changes and aided by monetary policy, which led to significant growth in domestic savings. The introduction of the liquidity coverage ratio was first proposed in 2010 and came into effect in 2015. The net stable funding ratio was proposed in late 2009 and became fully implemented in 2018. These regulatory changes in response to the crisis encouraged banks to reduce their short-term wholesale debt funding and replace it with increased deposits. Deposits now comprise 60% of bank funding, up by a third from 2008. Given the stability of deposit funding, this supported balance sheet growth.

In a rising rate environment, there is uncertainty over whether this level of deposit funding will continue. The cost of deposits will increase, and availability may decrease if savings rates turn negative. Australia’s household savings ratio, defined as savings relative to income, has been on a steady decline from its pandemic-era peak of 20.7% and fell to 3.2% in July 2023. Deposit stability is another factor that will receive increasing attention. In response to the Silicon Valley Bank collapse in the US, Australian Prudential Regulation Authority (APRA) has published a consultation paper on liquidity requirements for small banks. APRA has also signaled that liquidity is a broader priority, though its impact on funding profiles remains to be seen.

Banks are facing profitability pressures — growth sources are unclear

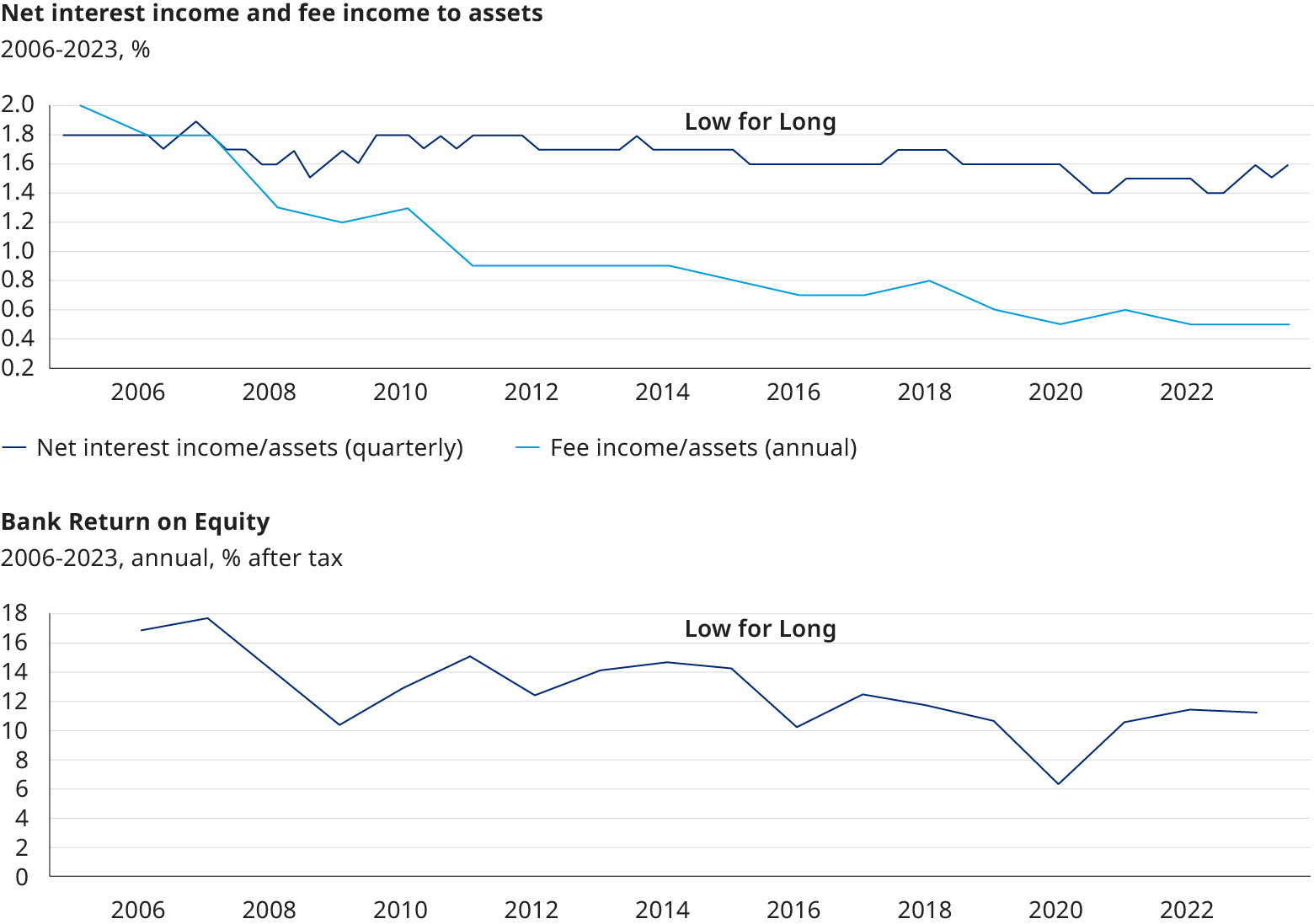

During Low for Long, major banks in Australia used their structural advantages to double down on highly profitable home lending — a prudent strategy in a period when they could at times achieve a home lending return-on-equity (ROE) of more than 30%. But such returns were a global exception. They have since been eroded by higher capital requirements and intense competition, supported by the rise of mortgage brokers, which now account for around 67% of mortgage flow, up from 48% in 2012. During 2022 and 2023, competition in the mortgage market finally boiled, with many banks and analysts commenting on mortgage returns being at or below the cost of capital.

Banks’ non-interest revenue as a ratio of assets has also been on a continuous decline over the past two decades, exacerbating a fall in bank ROE. Much of this decline can be explained by stagnating sector fee income in absolute terms during a period of strong asset growth. Following the Banking Royal Commission, banks chose to exit high-yielding wealth management and insurance businesses. They also lost market share in fee businesses such as payments, merchant acquiring, and foreign exchange to financial infrastructure, technology, and services firms. Another contributing factor may have been the relative decline of wholesale banking, which tends to have a greater proportion of fee income.

The Australian financial system has been significantly reshaped over the past 15 years, with regulation making the system safer. Australian consumers and businesses expanded their borrowing from the global financial crisis period until 2022, causing bank balance sheets to balloon. However, with a New Monetary Order underway, the tide is turning fast, and banks are under pressure. Where majors retreated from portfolios, other lenders have established a stronghold that will be hard for majors to dislodge as they search for growth.

Uncertain times and new actors in the credit sector

There are two key uncertainties we consider as we enter this new credit cycle. The first is how the economic environment will unfold. The second uncertainty is how the competitive landscape will respond. Australia’s credit market looks and works differently now from previous periods of rising rates in three key ways: foreign banks are a bigger force in corporate lending than any of the majors; leading non-bank lenders will be able to weather a downturn better than in previous cycles; and superfunds and assets managers are breaking into private debt, with vast pools of private capital at their disposal.

Exploring the impact of Australia's New Monetary Order

Australia and other developed economies around the world are on a path into unknown territory regarding monetary policy. The New Monetary Order presents a set of unique challenges and opportunities to financial institutions that will require them to reactivate long-forgotten muscles and develop new ones. While the forces that will shape the New Monetary Order in Australia are already visible, the playbook is still being written each day. It will look different from the playbook of the past decade.

As for every new era, this one will create winners and losers. The sooner leaders start to act, the better their chances are to emerge on top.