Since its proposal in 2015, the Guangdong-Hong Kong-Macau Greater Bay Area (Greater Bay Area, or GBA) has been envisaged as China’s innovation and opening-up hub. With the border re-opening, we expect the Hong Kong-Guangdong cooperation to scale up and deepen further. The integration and connectivity of the Greater Bay Area have also been supported by the continuous upgrading of the manufacturing sector in the Pearl River Delta area, favorable policies such as 30 Financial Measures of Qianhai, and infrastructure in place such as Shenzhen Data Exchange. The economic powerhouse is poised to usher in a new wave of acceleration in intra-regional collaboration and cross-border trade.

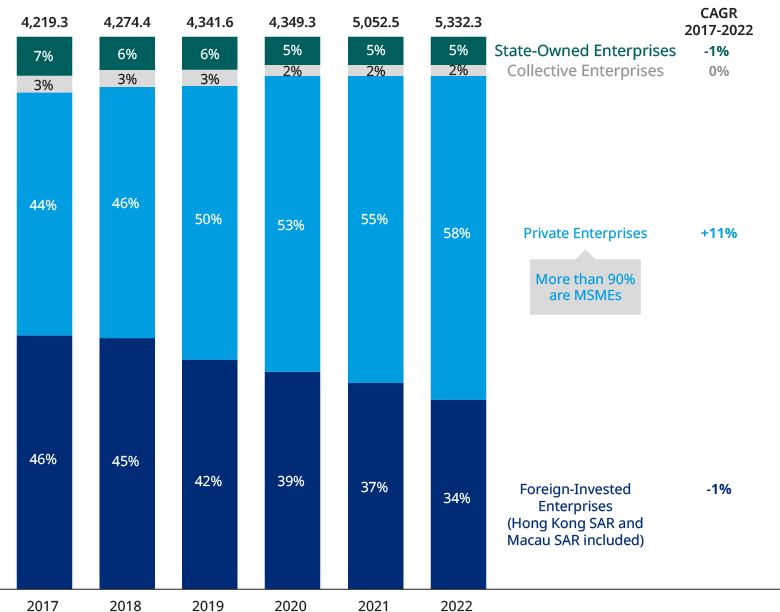

Micro, small, and medium-sized enterprises (MSMEs) are the primary momentum for cross-border trade in the Greater Bay Area. The private sector, predominantly MSMEs, accounted for 58% of the total exports of the nine mainland GBA cities in 2022, a rapid uptick from 44% in 2017. MSMEs are paramount in optimizing the region’s industrial structure and facilitating China’s dual circulation strategy.

Note: Export value estimated as a percentage of Guangdong Province’s total export value, over 95% of which is attributed to the nine mainland cities in the Greater Bay Area between 2017 and 2021.

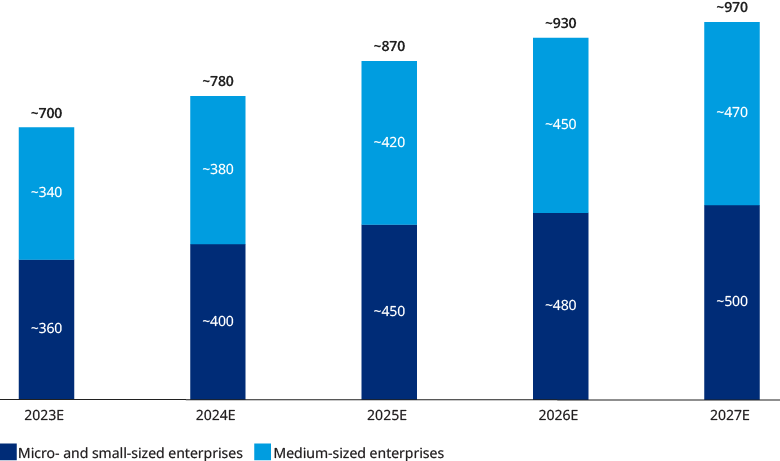

Yet, many MSMEs face operational challenges in turnover, foreign exchange, payment and settlement, emerging markets expansion, and digital transformation, translating to a massive demand for cross-border financial services, including foreign exchange, financing, payment, and business empowerment. Take financing as an example. The potential need for funds for export trading MSMEs in mainland GBA is estimated at ¥700 billion in 2023 and is expected to reach ¥1 trillion by 2027.

Moreover, our study indicates diverse trends for MSMEs business models in the manufacturing and trading sectors in the GBA. Financial institutions (FIs) in the GBA should capture this enormous market by providing diversified financial services for MSMEs, in which customer profiling is the trump card to come out on top.

Focusing on product offerings and target customers, we map out a two-pronged winning strategy for FIs.

First, by leveraging data analytics, FIs can launch offerings on both asset and liability sides to address the typical needs of varied MSME personas in cross-border finance.

- Asset: For MSMEs that have established separate entities in Hong Kong and mainland China, FIs can adopt data analytics in the credit-screening process and extend joint credit to allow for flexible allocation of transboundary capital.

- Liability: FIs can empower MSMEs with data analytics, risk management, and other capabilities and deliver tailored capital management services. For example, FIs can help companies better forecast foreign exchange fluctuations and manage cash flow. They can also help MSMEs lower costs and improve efficiency for cross-border payment and collection by utilizing e-payment channels.

Second, FIs can focus on two high-growth customer segments — companies expanding in emerging markets and high-tech startups — and offer a complete set of financial and non-financial service solutions to foster growth.

- Emerging markets MSMEs: FIs can liaise with ecosystem-wide partners to render a package of services, encompassing local account opening, legal affairs, tax, and capital management, to accompany MSMEs that are actively expanding into emerging markets such as Southeast Asia and the Middle East to get off the ground and thrive.

- High-tech startups: Long-term growth funds and non-banking services are called for to incubate high-growth or high-potential high-tech startups that still need to be scaled or profitable.

Despite the presence of some banks in cross-border finance within the GBA, the current coverage of traditional banks for MSMEs is still limited, partly due to the high cost of services, limited credit screening capabilities for MSMEs, and the uncertainty of transboundary data transfer. Nevertheless, FIs can close these gaps by adopting digital solutions. Digitalization can also help FIs improve their customer relationship coverage in Guangdong and Hong Kong, enhance their credit risk management and service efficiency, and establish an ecosystem to empower MSMEs cooperatively. FIs can thus better fulfill their roles in catalyzing inclusive finance and fostering the real economy across the Great Bay Area.

This article was jointly developed by Oliver Wyman and WeBank.

Additional contributor Christina Bi, engagement manager at Oliver Wyman.