The financial services industry is, at one level, a story of stability over the last decade

First and foremost, there hasn’t been a major financial crisis since 2008. This is a far cry from the experience of the previous 20 years, when a crisis of reasonable scale hit the financial system every four to five years.

This greater level of resilience has allowed the financial system to play the shock absorption and policy transmission roles for which it is at least partially underwritten by governments and societies in three major ways:

COVID-19 turned out to create far lower credit losses than planned for. The financial system played an important role of economic shock absorber, with excess capital able to absorb a high projected level of economic losses that did not come to pass, allowing financial services companies to write back up much of what they had written down.

In the war in Ukraine, the financial system has acted as the primary instrument of economic sanctions policies, shutting off Russia from most cross-border and international financial interaction with the West, and absorbing or managing actual losses in the financial system without any major signs of contagion risk so far.

On climate, financial services firms are playing a leading role, making ambitious net zero commitments and beginning to pour huge investment into helping corporate and retail customers to achieve their own net zero transition plans over the coming years.

Exhibit 1: Total financial services shareholder value

Based on market cap, USD TN, Jan 2000-Jan 2022

Incumbent financial institutions believe they have at least sufficiently caught up on digital transformation. Many have significantly increased the quality of services through mobile apps to close the gaps in customer service and retain their customers, and have digitized some internal processes to make operations more efficient.

The economics in the industry are improving: Profit levels are up in banking in many parts of the world, heavily challenged capital markets businesses have had a good couple of years, and strong asset values have generally continued to power wealth management and insurance. Looking ahead, rising interest rates will have beneficial effects on net interest margins.

By no means are we calling the end of financial crises. The build-up of leverage in the economy after a decade of cheap money is concerning, and as most banks look at the future scenarios, stagflation — low economic growth combined with underlying inflation — is a very challenging possibility for economies and could spark credit deterioration. Yet the evidence is that the financial system is in better shape than at any time in recent memory to manage and continue to support economic growth.

Yet where growth and value creation are taking place is anything but stable

The shifts in valuation for participants in the industry point either to significant misallocation of capital or to a much more significant shift in underlying value taking place. Our analysis of value is conducted in late May 2022, already after the significant sell-off in some big tech and fintech stocks and valuations over the course of early 2022.

Exhibit 2: Financial services valuation change

Top 20 firms, 2011 vs. May 2022, US$ TN

The three categories of firms we think of today in Financial Services are:

Incumbent banks, insurers, and asset managers: These are companies that manage balance sheets and are largely focused on risk intermediation. The top 20 firms have grown by about 70% over the last decade, undershooting their earnings growth of 105% as higher capital requirements have weighed on valuations.

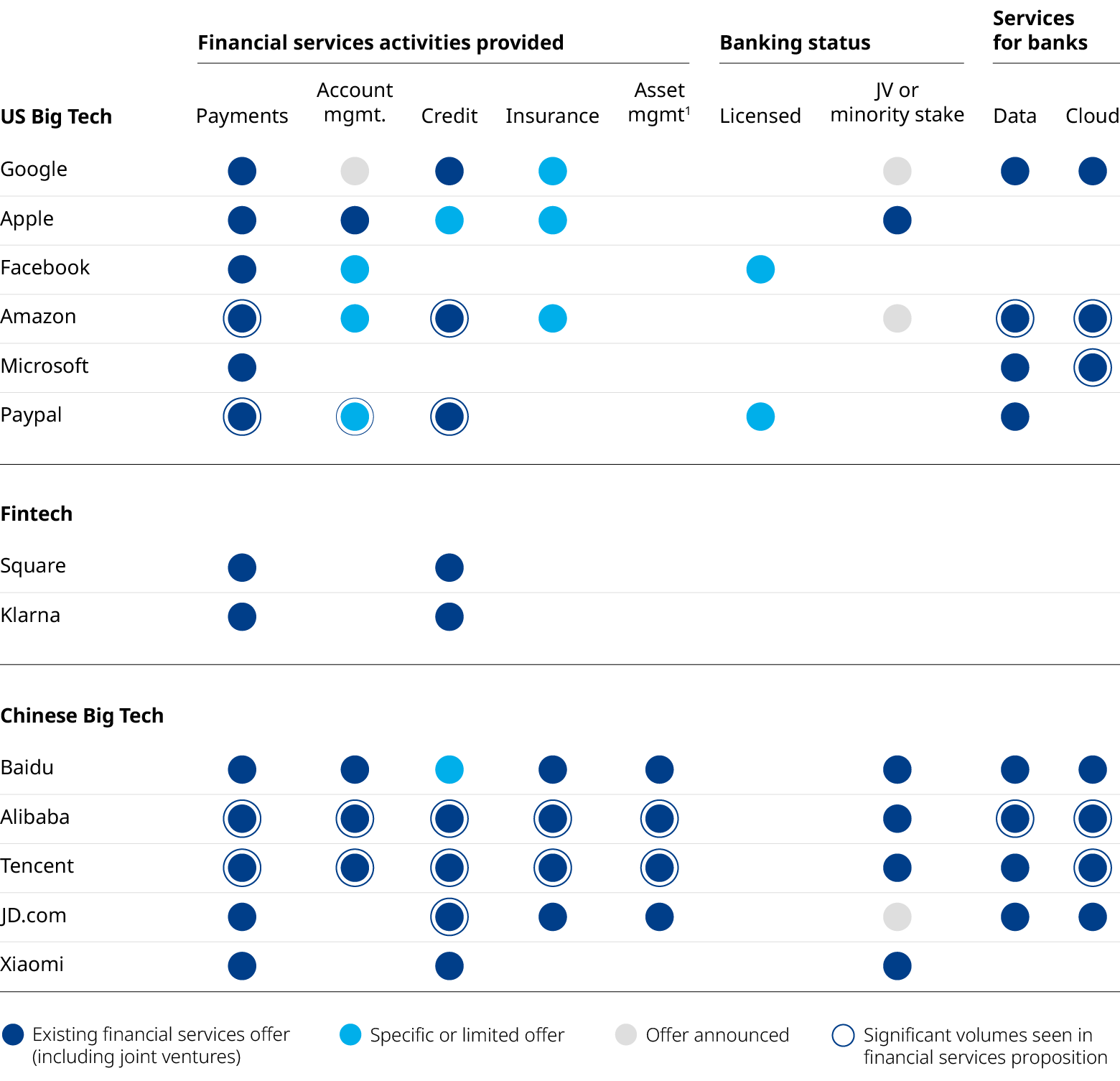

Big tech and merchants: These are distributors that are either manufacturing or embedding financial services in their offerings. The merchants are a wide group ranging from online retailers to auto firms to telcos. Big tech companies are the newest players however, growing value by 405%, even adjusting for the major devaluation in 2022, and outstripping earnings growth — which at 230% was still significant. Of course, only a subset of the value growth is related to financial services but this is increasingly meaningful as we show in Exhibit 12.

FITs. This is a category we use to describe a wide range of firms focused on infrastructure, data, and technology related services in financial services. Some of the data providers such as S&P and market infrastructure firms such as the CME are mature, nevertheless growth has been high at 330%. The payments and technology firms have seen explosive growth at 480%, and already-prominent firms like Mastercard, Visa, and Amex are now huge, as are newcomers like PayPal and Square. Finally, in this category we also have privately owned fintech firms including digital asset firms, almost none of which existed 10 years ago.

While the top incumbent firms in the industry have delivered about $1.3 trillion in new value in the last 10 years, the listed FITs firms alone have delivered $1.7 trillion of value growth, added to which is the value created in private capital and in big tech and the merchants’ activities in financial services. In total we estimate even after the technology shakeout in 2022, the top firms outside the incumbents have delivered more than $3 trillion of new value in financial services.

Financial institutions built extremely lucrative business models to serve these needs. Risk pools were created and value was extracted through risk management over time and via diversification. In fact, managing and holding pools of risk were so lucrative that ancillary services like custody of money and reporting through bank accounts were provided for free, and others, such as payments, were essentially positioned as a low-cost add-on or “part of the service.”

Exhibit 4: Growth of banking revenue and balance sheets

2010-2021 Compound annual growth rate (CAGR)

Over the last 15 years, we estimate, the customer penetration of new products and services anchored in creating and managing pools of diversifiable risk has slowed in most of the world, with the main exception being some emerging markets and parts of Asia. More dramatically, the cost of this balance sheet-intensive business in terms of capital and infrastructure costs, compliance costs, and regulatory costs has rocketed — largely in reaction to a series of crises, most notably the global financial crisis.

Just as the relative value and speed of growth momentum of risk intermediation services has waned, the value of technology and data services is rapidly increasing, in myriad ways. Some of these services involve the evolution of risk intermediation toward services that help customers better understand their own risk profile and reduce it. For example, instead of providing a general price on car insurance, companies can use far more accurate data to help customers reduce the chances of having a car crash and therefore the amount and cost of insurance required. Or a bank can use analysis of customers’ spending behavior to help them avoid credit charges or even default. In some instances banks, particularly in Asia, are starting to use social media data to improve underwriting and offer better terms to good credit customers.

Many of the potential new services are very different from traditional financial offerings. Instead of providing an account balance, for example, a bank can advise customers on whether they are overpaying for energy services, or whether their spending patterns will create a problem when it comes to their kids’ education costs in 10 years. Instead of just processing their payment, a payment provider can inform them where they might have accessed a cheaper product, or refer them to a physical location nearby where they can go to look at future alternatives. The list goes on.

Incumbent banks and insurance companies have been building these offerings for years now — just not at all quickly enough relative to the range of other new entrants taking market share in the most lucrative parts of the value chains.

The new financial services industry emerging

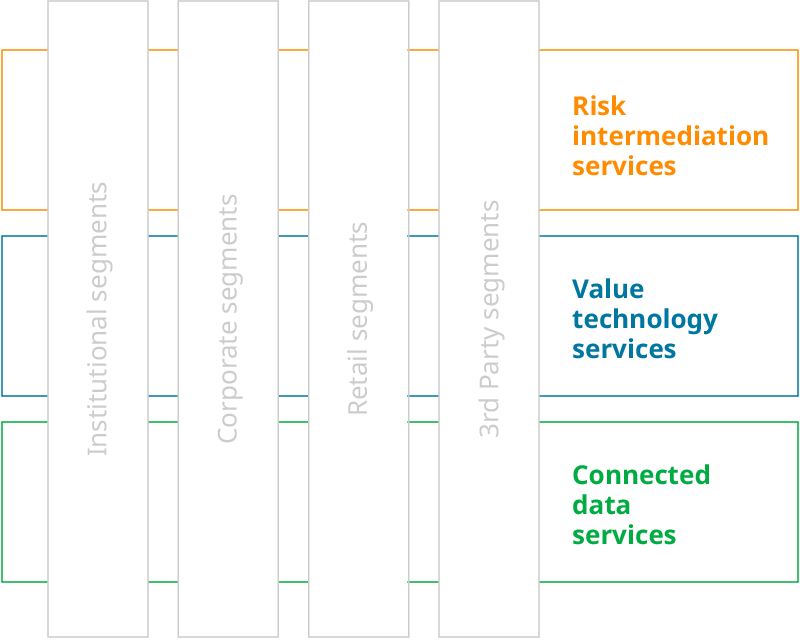

So financial services is expanding and growing in all sorts of ways, attracting capital from many sources and garnering more and more involvement from big tech. There are opportunities galore, but the nature of these opportunities has changed. We break out the emerging industry into the following service segments:

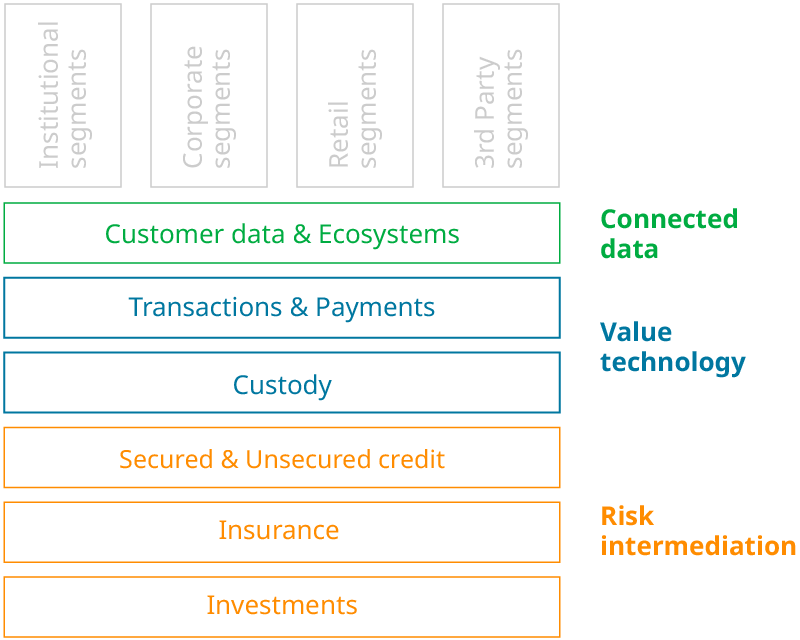

Risk intermediation services. We define this as any service that involves matching those who have money with those who need it, while the provider takes some financial risk along the way — be that credit risk, market risk, interest rate risk, and so on. Of course this is the core of the incumbent industry, risk intermediation services are now extremely high capital intensive, and with ultra-low interest rates for a decade they have been in low-growth mode. No doubt the shift to rising interest rates will change this and lead to better returns for risk intermediation services, but the penetration of risk intermediation services with customers is mature if not saturated, so the growth is akin to a rising tide lifting all boats, not new value creation as defined by new services to new customers.

Value technology services. We define value-technology as technology that is being used to deliver a new service to an end customer, rather than just improving an operation or function. The industry has experienced a 10-year explosion in growth in payments and transaction-related services, most of which were garnered by merchants including big tech companies such as Alibaba, Amazon, and Ebay, as well as new players like Paypal, Square, and Circle. Focus is now shifting toward monetizing new technology such as digital assets, tokens, and decentralized finance. At the same time, both incumbents and new players are looking for winning models in wholesale services such as through banking as a service (BaaS) and insurance as a service (IaaS).

Connected data services. We define these as services that rely on using data or connecting different sources of data to create value for customers, such as helping customers manage their financial health or making it easier to manage logistics, real estate, mobility, health, and so on. Initiatives like open banking have not yet led to the sort of data-sharing explosion envisaged, but the acceleration in growth in wallets, financial life coaches, embedded finance, and so on all show that the potential from connected data services is being realized.

Exhibit 5: A wider set of financial services now, with very different economic profile

It is important to note that we believe the expansion in the nature of financial services is based on new data and technology and evolving customer needs and expectations, and as such will continue. Likewise, the faster growth in new capital-light businesses driving greater potential for value-accretion to the winners in providing these services will continue. What is far less certain is precisely who will win in delivering these services.

Compelling customer service and customer trust — where value and valuation meet

Services take root only when customers find them compelling. The high growth in value technology and connected data-related services are driven by providers offering customers something they find valuable, that improves their business effectiveness or their lives, and that they are willing to pay for. In B2B financial markets the high growth in market data services is largely because the providers have integrated data into desktop and workflow in ways that make financial analysis, trading, and investing far more efficient. In B2C markets the extraordinary expansion in new payments accounts, as shown in Exhibit 6, is because providers are integrating payments into frictionless and mobile services at the point of purchase that provide real-time information back to customers through much more accessible apps.

Exhibit 6: Growth in traditional US bank accounts vs. payment provider accounts US$ MN

Customer trust is hard to value, but there is little doubt it is playing a core role in how the financial services industry is evolving, and where value and valuation emerge. Some of the shift we have seen over the past decade has roots in the global financial crisis, when the incumbent financial system took a significant trust hit. At this point in time, trust in big tech is under significant pressure, and volatility in instruments like digital assets is posing trust questions. These dynamics could prove central to how the landscape evolves in the coming years.

Exhibit 7: Revenue and revenue growth from leading listed FITs firms

Valuations will oscillate, particularly in unproven business models, and we have seen a lot of this already in 2022. But underlying customer value is being created in both connected data and value technology services, and where compelling services and customer trust combine, winners will emerge.

Change in services, change in landscape

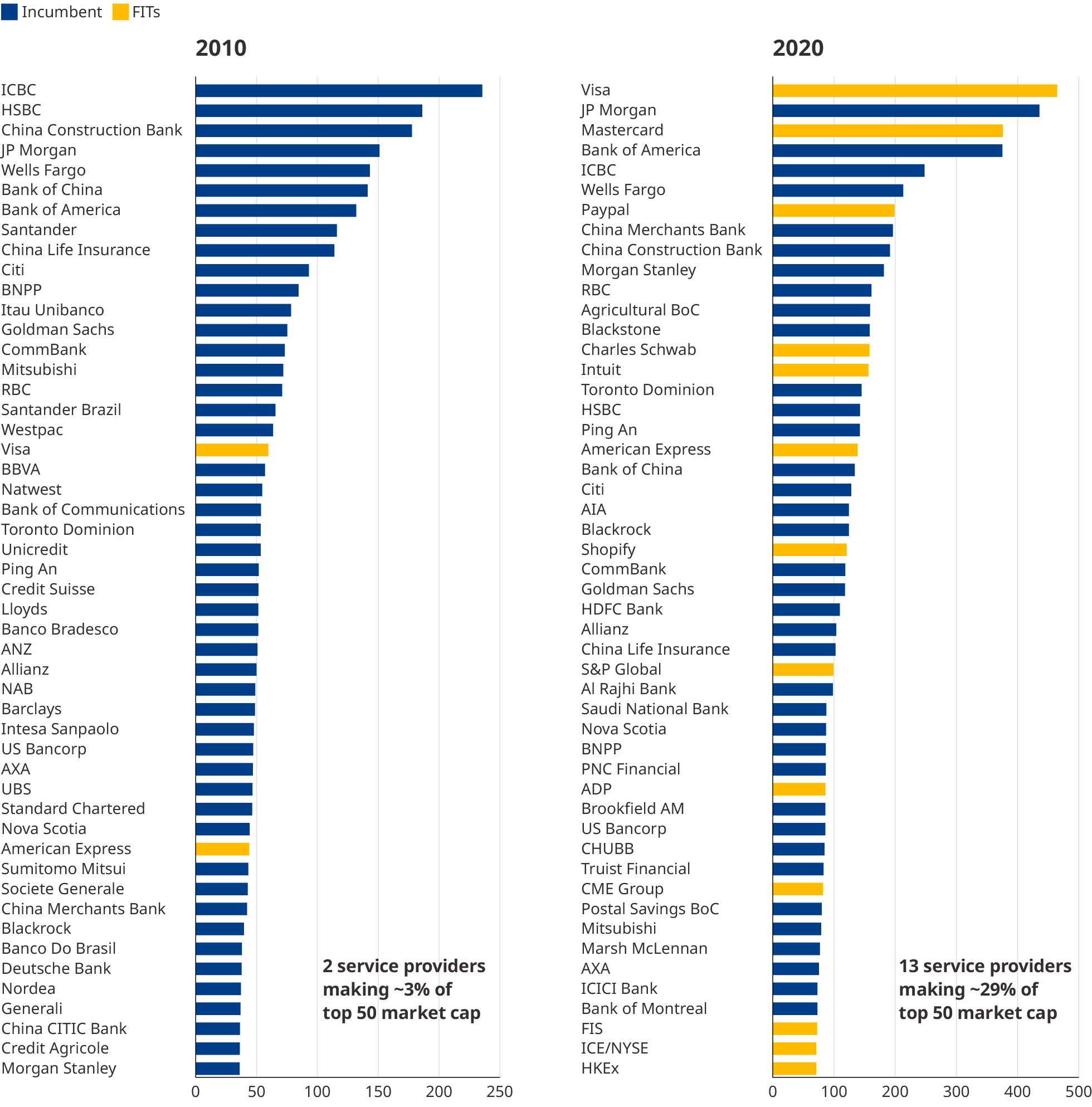

As the value in technology and data related services has increased, this shift has resulted in many new competitors thriving. As we show in Exhibit 3, the list of the top 50 firms in financial services in 2010 included only two that were not incumbent banks, insurers, or asset managers. Today that is getting close to a third by number and market cap. This list also excludes big tech and other large merchants, such as Walmart and Walgreens, that are now extremely active in financial services.

Likewise, in 2010 the industry largely looked like a set of banks, insurers, and asset managers with a set of technology and service suppliers. Today this is a far more complex picture. Ecosystem co-opetition is the new landscape, where firms sit in each others’ value chains in simultaneous partnership and competition. It’s worth noting that this not just about the relationship of incumbents with big tech and with FITs firms. There are equally fascinating dynamics in the relationship between big tech and FITs; witness the much commented-on shifts in the relationship between Amazon and Visa in recent years.

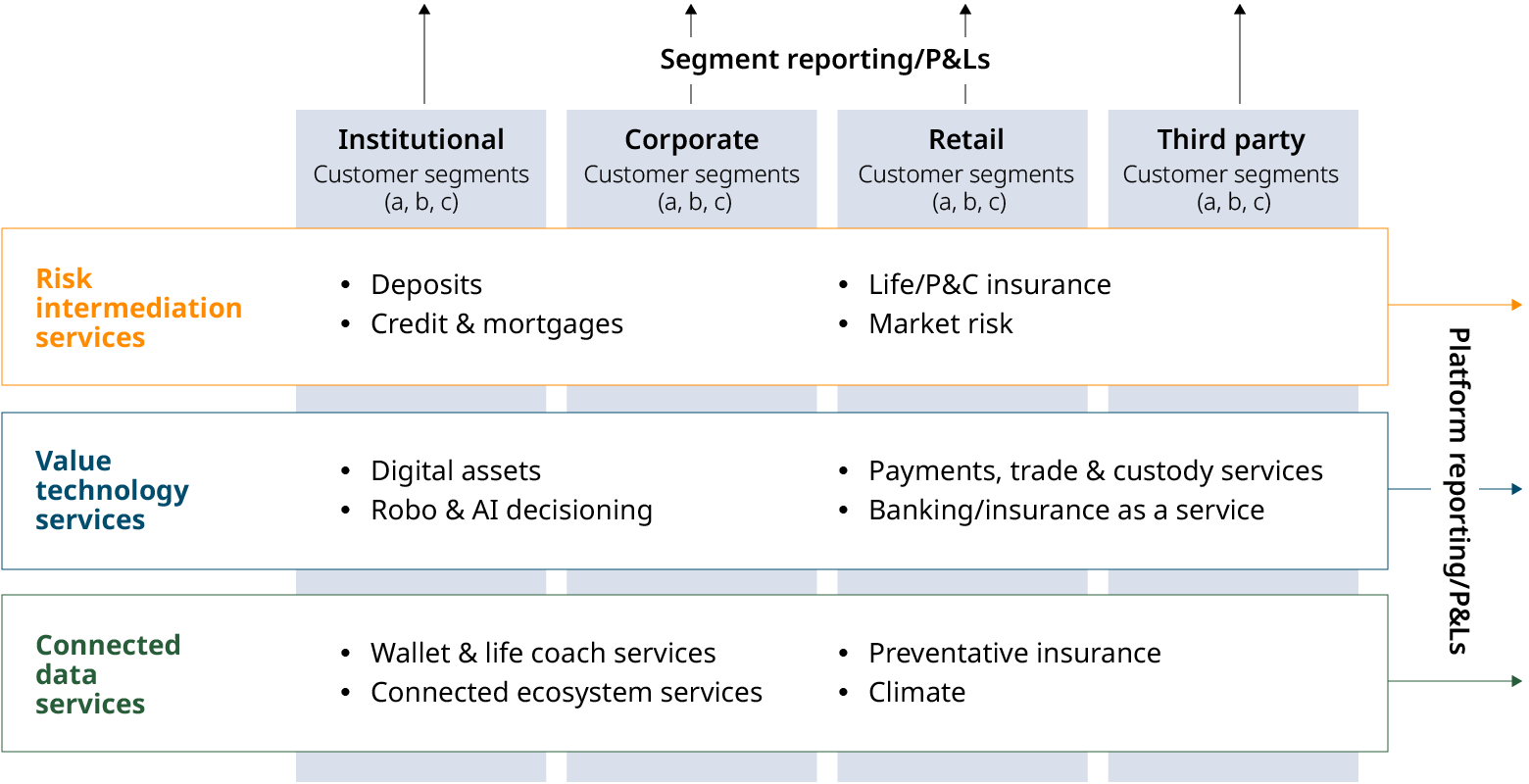

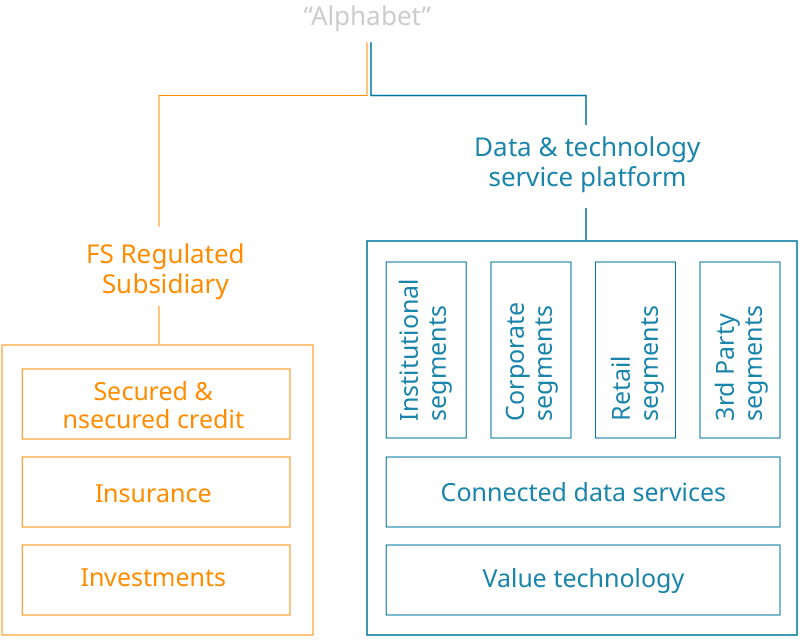

The result is a very different financial services industry from just a decade ago. At that point our most relevant segmentation would have been between global banks, regional and local banks, insurance companies, and asset managers. But Exhibit 8 shows what is arguably a more telling segmentation today.

Exhibit 8: Reframing the financial services industry

The fascinating question is how this plays out over the next decade, and this is far from certain because it depends both on market conditions and on how policy and regulation evolve. We lay out four possible scenarios:

1. Continued expansion with incumbents becoming utilities

Continuing the path of the last decade, where more of the capital-light technology and data services get picked up by FITs, big tech, and merchants — likely with consolidation of the fintech industry into a smaller number of bigger winners, with the incumbent banks/insurers/asset managers significantly limited, utility like, to provision of risk intermediation services.

2. Market-driven rebalancing

A shift in market conditions drives a rebalancing of the system, for example prolonged high interest rates, combined with a severe market correction in technology valuations as we saw in the dot-com crash — all of which would likely drive consolidation of incumbents with small-to medium-sized FITs firms and support incumbents regaining ground in connected data and value technology services.

3. Policy-driven rebalancing

Policy and regulation are designed to put greater constraints on more of the firms growing quickly in data and technology services, including in digital assets. China is certainly an important case study in this regard, where the explosive growth in fintech and big tech in financial services has been curtailed over the last two years, rebalancing the system, at least to some extent, back toward the incumbents.

4. Trust-busting crisis

Dramatic loss of trust tends to come out of significant crises, and in the past most of these have been financial crises, where leverage bubbles burst. However, as financial resilience has improved and privacy concerns increase, the likelihood grows that cyber or privacy breaches could be the next big trust crisis, with a lot of possible new weak points in the system now.