This report was commissioned by the European Banking Federation (EBF) and represents the view of Oliver Wyman as independent experts that do not necessarily represent those of the EBF or its members.

Since the Global Financial Crisis (GFC), significant steps have been undertaken to strengthen the EU’s banking regulatory framework. The strength of the EU banking system has allowed banks to weather the cataclysmic impact of the COVID-19 crisis relatively undamaged. Banks helped backstop the economy, leveraging fiscal support measures of unprecedented scale and the accommodative monetary policy regime of the last decade.

Despite its strength, the EU banking sector today is not earning its cost of capital, while US competitors have returned to pre-crisis profitability levels. This has been driven by an economic environment of comparably poor growth in the Eurozone, late policy responses to the Eurozone debt crisis, high fragmentation, lack of scale in a context of rising minimum cost of doing business, and a long period of negative interest rates that depressed banks’ earnings in a period where they had to strengthen capital buffers.

Today, there are still structural obstacles to bank consolidation across the Eurozone, preventing banks from realising synergies across markets. The Banking Union will remain incomplete for the foreseeable future. Political and regulatory restrictions remain that prevent the emergence of universal bank business models spanning across borders, in particular requirements that impede liquidity transfers within the Banking Union.

Furthermore, the EU’s capital market union remains underdeveloped, preventing the creation of a securitisation market. Persisting market fragmentation, due to the lack of convergence of insolvency rules among other issues, hampers cross-border investment within the EU and dampens funding from outside. This happens at a time when more financing, including equity, is needed to overcome geopolitical, environmental, and digitalisation challenges.

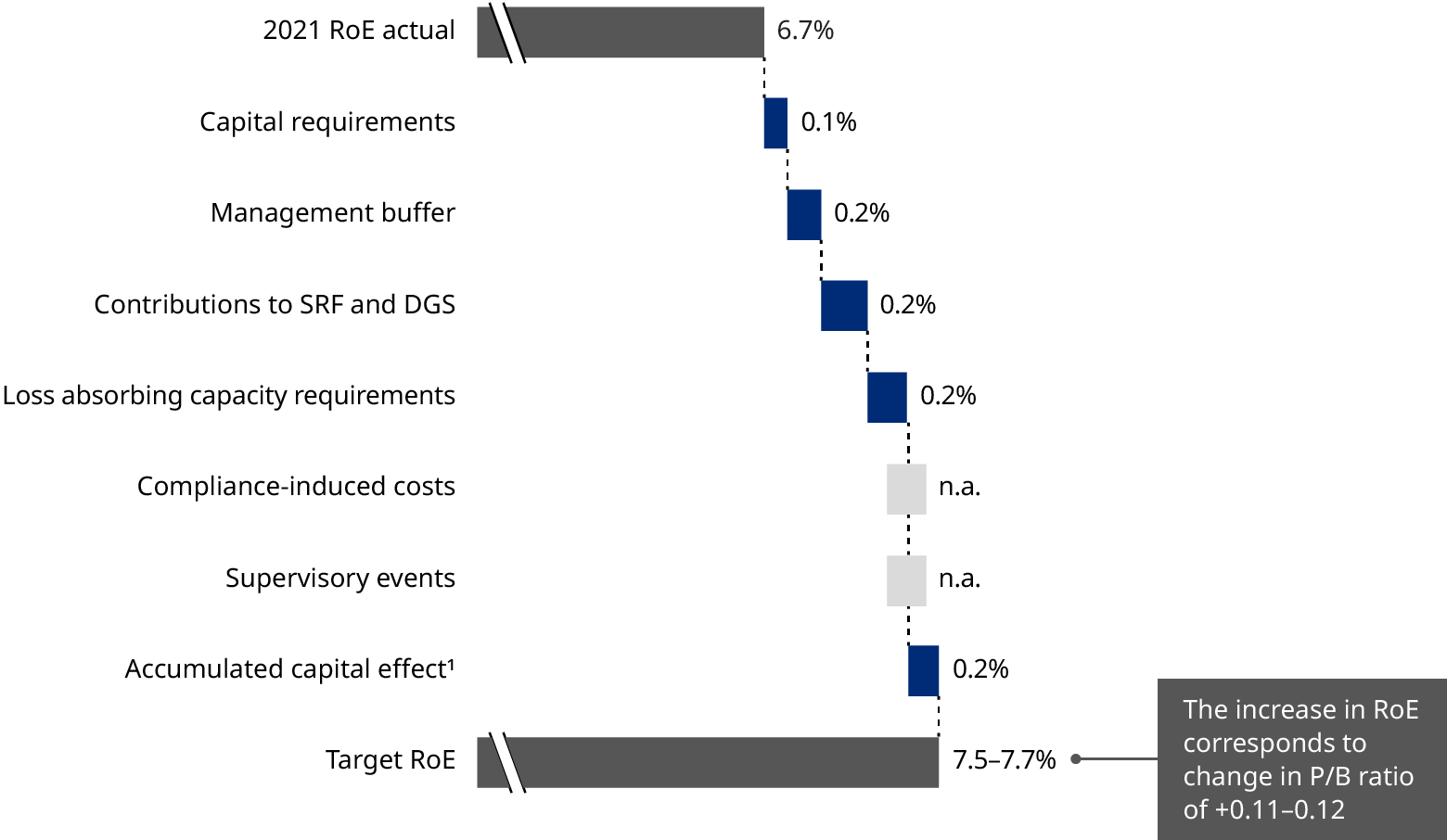

Despite a globally coordinated “level playing field,” differences remain across economies in how rules effectively work and how they are implemented. The incremental difference in regulatory-induced cost at EU banks compared to US peers can explain 0.8-1.0 percentage points of the return on equity (RoE) gap.

The EU’s approach to determine capital requirements is more complex, gives regulators wider discretion and might be perceived as being less transparent. The resulting uncertainty is one of the reasons that EU banks tend, on average, to hold surplus capital. Additionally, on average and considering that samples are not directly comparable given differences in business models and market structure, EU banks face higher capital requirements than US peers: 10.6% versus 9.9% for Common Equity Tier 1. In addition, future requirements related to the full implementation of Basel III and climate-related capital surcharges are expected to penalise EU to a larger extent than US banks.

Further, EU banks face almost twice as high contributions to deposit and resolution funds at EU and member-state level compared to US peers, while requirements on bail-in-able capacity are 3.9 percentage points higher than in the US. Despite a gradually mutualised safety net, cross-border access to the European market remains limited for EU banking players.

A review of current capital requirements and supervisory processes could, in a hypothetical scenario, provide capacity for €4-4.5 trillion additional bank lending, provided that policies and measures are put in place to ensure that viable borrowers have growth opportunities that support additional borrowing demand. Additional lending could also support the financing of the green and digital transitions, and more generally investments in strengthening the competitiveness of the EU economy. Further, this would create additional opportunities for investment in areas such as consolidation and digitisation.

The Oliver Wyman expert panel for the study included Christian Edelmann, Élie Farah, Til Schuermann, Stefan Schwengler, and Davide Taliente.