Part 2 in a series

In the second of a series of articles, we examine the implications of rising interest rates on U.S. GAAP and statutory financial reporting for life insurers, highlighting potential tailwinds from a stable increase and headwinds from a sharp increase. We further provide insights into how insurers can leverage asset liability management (“ALM”) programs and interest rate risk hedging practices to favorably position themselves in a rising interest rate environment.

Key highlights:

IMPACT ON LDTI – TRADITIONAL PRODUCTS

We anticipate less interest-rate-related financial statement volatility for traditional lines of business under Accounting Standards Update (“ASU”) 2018-12, commonly referred to as Long Duration Targeted Improvements (“LDTI”). Without LDTI accounting changes, companies would experience large reductions to equity as its accumulated other comprehensive income (“AOCI”) reverses as a result of rising interest rates. LDTI includes an interest rate-related adjustment for reserves in OCI to offset unrealized investment gains. As a result, OCI will be less volatile under LDTI as potentially large equity reductions attributed to rising interest rates are circumvented.

IMPACT ON LDTI – INTEREST-SENSITIVE PRODUCTS

Under LDTI, companies without hedging or strong ALM programs will report additional profits under a rising interest rate environment; however, they will also face significantly higher earnings volatility. Companies with well-matched investment portfolios and comprehensive hedging may be rewarded with reduced earnings volatility. However, companies may have opted not to hedge interest rate risk due to expensive hedge costs under a low-interest-rate environment. These companies will now have an opportunity to reconsider their cost-benefit “break-even” points to manage hedging decisions as interest rates rise.

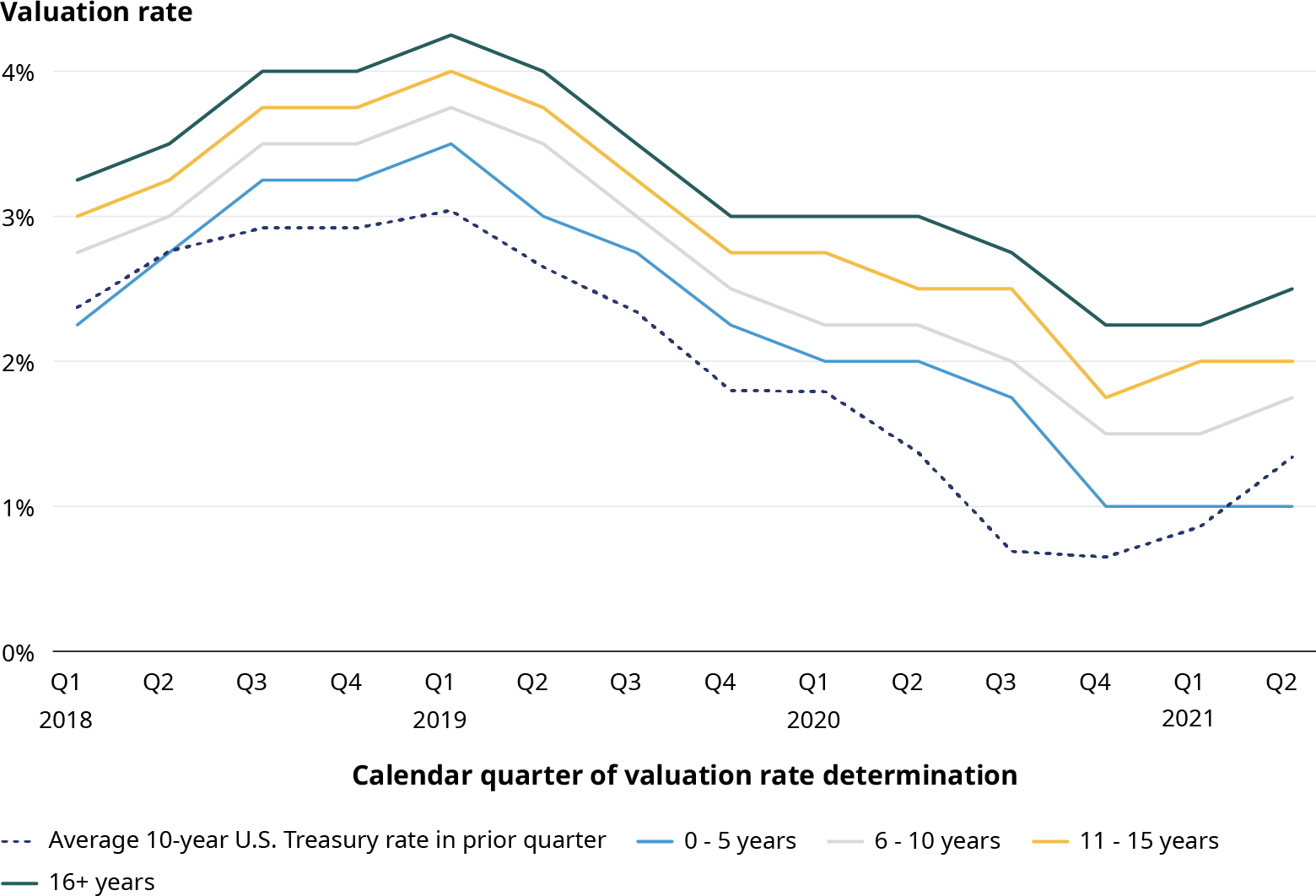

IMPACT ON STATUTORY VALUATION – PRESCRIBED VALUATION RATES

For products subject to prescribed valuation rate requirements, the impact of a rising interest rate environment would be lower statutory reserves for newly issued businesses due to the higher valuation rates used to discount future projected cash flows.

As an example, the exhibit below compares the maximum valuation rate for immediate annuities without life contingent benefits and with varying certain periods against the 10-year U.S. Treasury rate.

Rising interest rates would also drive higher projected reinvestment rates, ultimately reducing reserve and asset requirements. The net economic impact varies, subject to the level of duration mismatch in each life insurer’s ALM position.

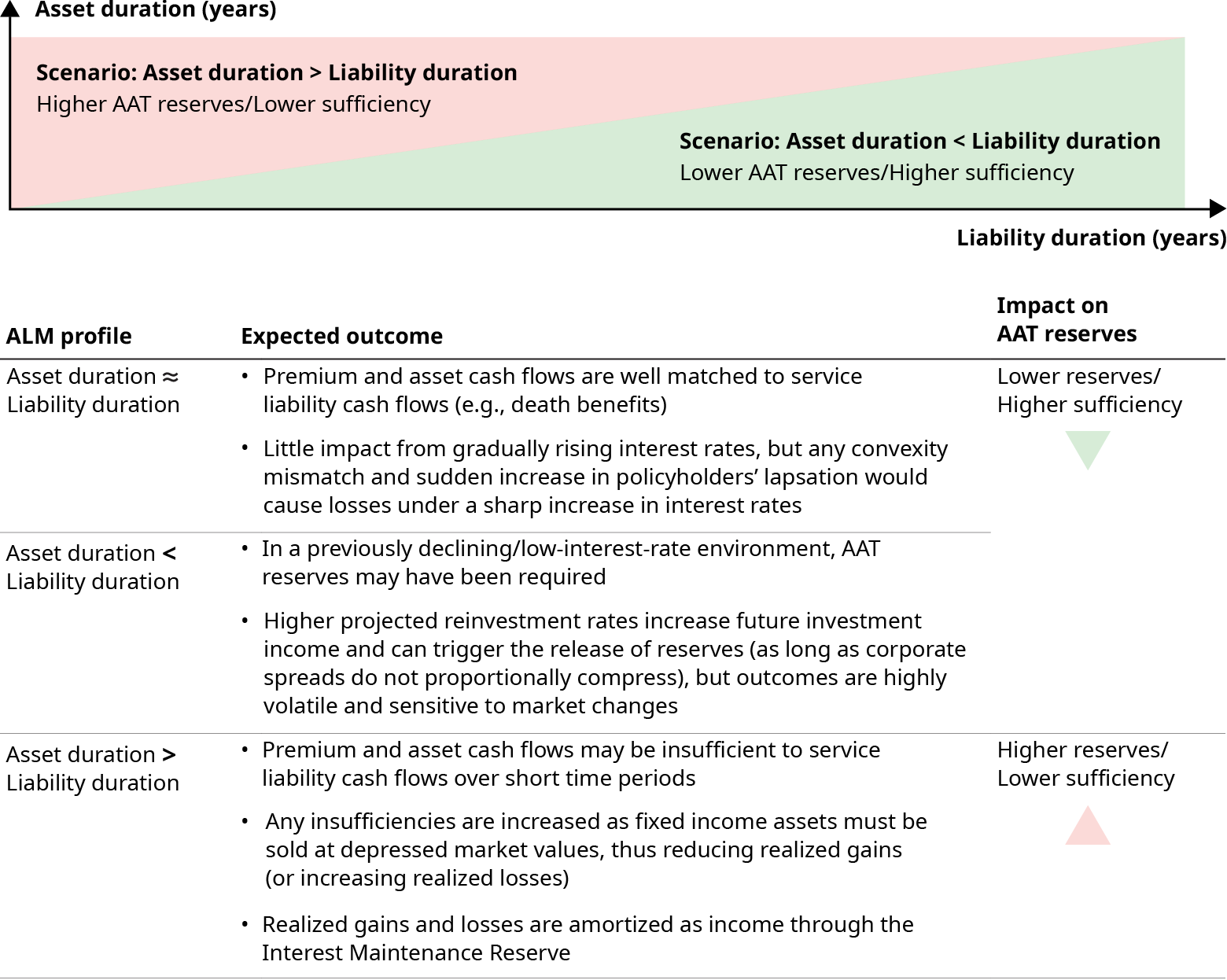

IMPACT ON STATUTORY VALUATION – ASSET ADEQUACY TESTING (“AAT”)

Life insurers perform asset adequacy testing under a selection of prescribed interest rate scenarios to determine the adequacy of assets supporting their liabilities. The exhibit below illustrates how the need for AAT reserves under rising interest rates is a function of a company’s ALM position.