This article was originally published by the Merchant Advisory Group on July 19, 2021.

COVID-19 has fundamentally changed our lives, in many ways permanently. One of the profound changes we are seeing is in the way consumers purchase goods and services: Increasingly the store is delivered to the customer rather than the other way around.

This has led to an exponential rise in delivery companies who have now expanded to serve as aggregators for many merchants. Two years ago, who would have predicted that a relative unknown grocery delivery super app would now have a 50 percent share in online grocery delivery and a valuation of $40 billion? Overall, US food delivery revenues are estimated at $130-150 billion, with online grocery representing the lion’s share at $90-$110 billion.

The valuations of delivery aggregators have skyrocketed through the pandemic. Leading players have expanded seamlessly from delivering food to a host of new categories, including prescriptions, electronics, home décor, and beyond. One of Southeast Asia’s largest consumer technology platforms, provides insights into where delivery platforms might be headed as they gain control of customer relationships. Launched in 2012, the company has evolved into a super app with everything from ride-hailing and food delivery services to financial services for the unbanked. It announced it would go public in April 2021 at a $40 billion valuation, the app has had over 214 million app downloads across the eight Southeast Asian countries it operates in and recorded $12.5 billion in gross merchandise value last year. As aggregators expand to new areas of activities; merchants with proprietary payments can expect increased competition in financial services as well.

As the user base and the functionality of these apps grow, it is important to consider how much of consumers’ share of mind and attention they are capturing. And with this share of mind and attention comes significant parts of the customer shopping and payments journey. Delivery aggregators are fundamentally re-defining the role of the payment transaction for merchants that rely on their services for last-mile delivery.

As these aggregators capture share of the customer relationship, there are distinct implications for merchants (see Exhibit 3): What is the optimal view of delivery aggregators as our “frenemy”? What will the future of payments look like in a world where the merchant increasingly does not control the checkout experience and perhaps even the payment experience? These questions become most salient when delivery platforms start to nudge shoppers from one merchant to another. For instance, certain grocery platforms actively track basket purchases and a customer purchasing vitamin C from retailer A may find a promotion for vitamin C and other products sold by retailer B in their inbox the next day.

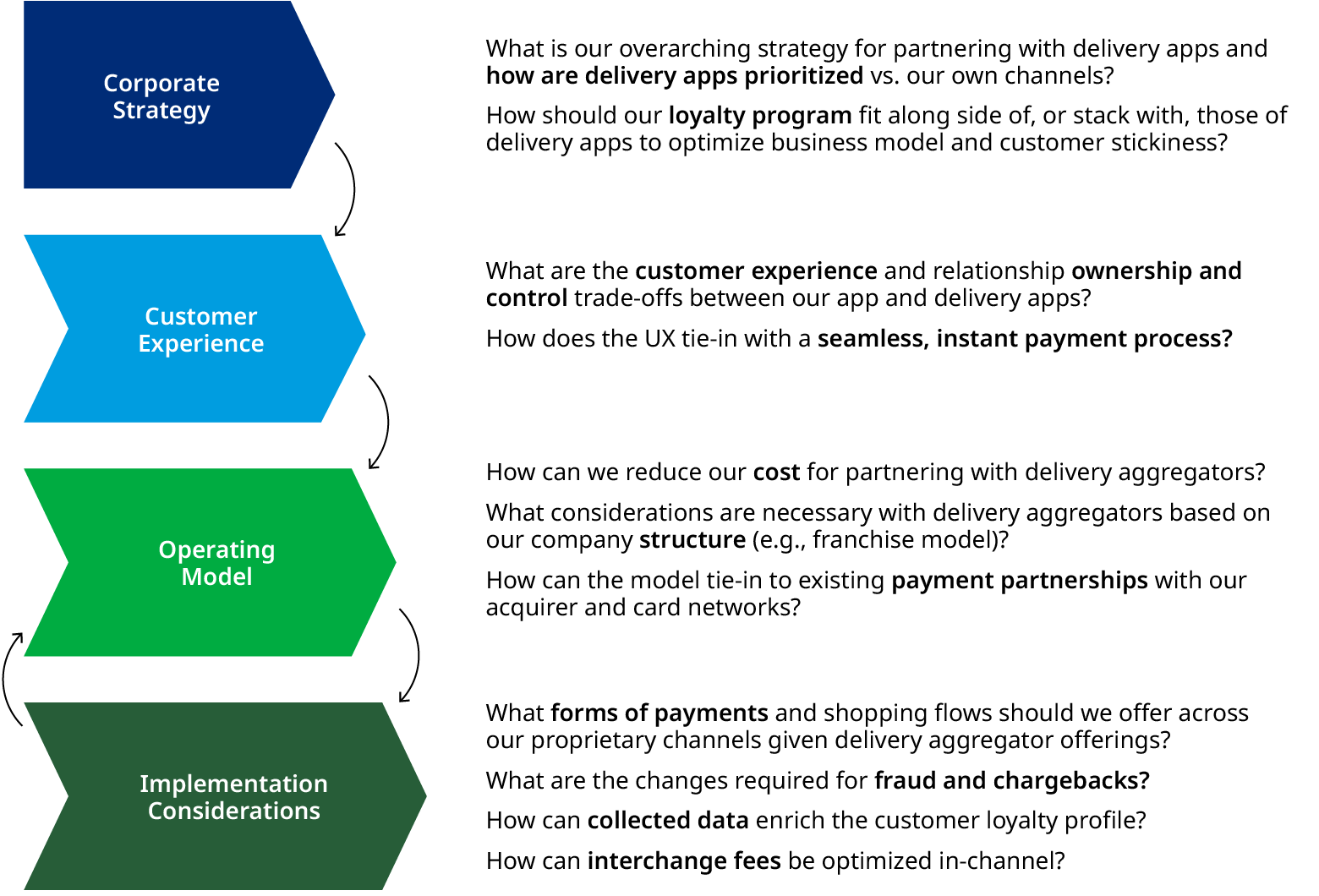

For merchants’ corporate strategy, partnering with aggregators is a delicate balancing act between driving sales and preserving strategic control over the customer relationship, of which the payment is one key component. Relying on delivery aggregators has direct implications on merchants’ revenue and multiple aspects of their payments operations. For instance, grocery merchants can expect to pay a 5-10 percent fee per transaction on delivery orders fully serviced by aggregators, directly impacting revenues. In addition, merchant payment acceptance costs can also double depending on the delivery platform. Beyond financial impact, using delivery aggregators has repercussions at each step of the online purchase customer experience.

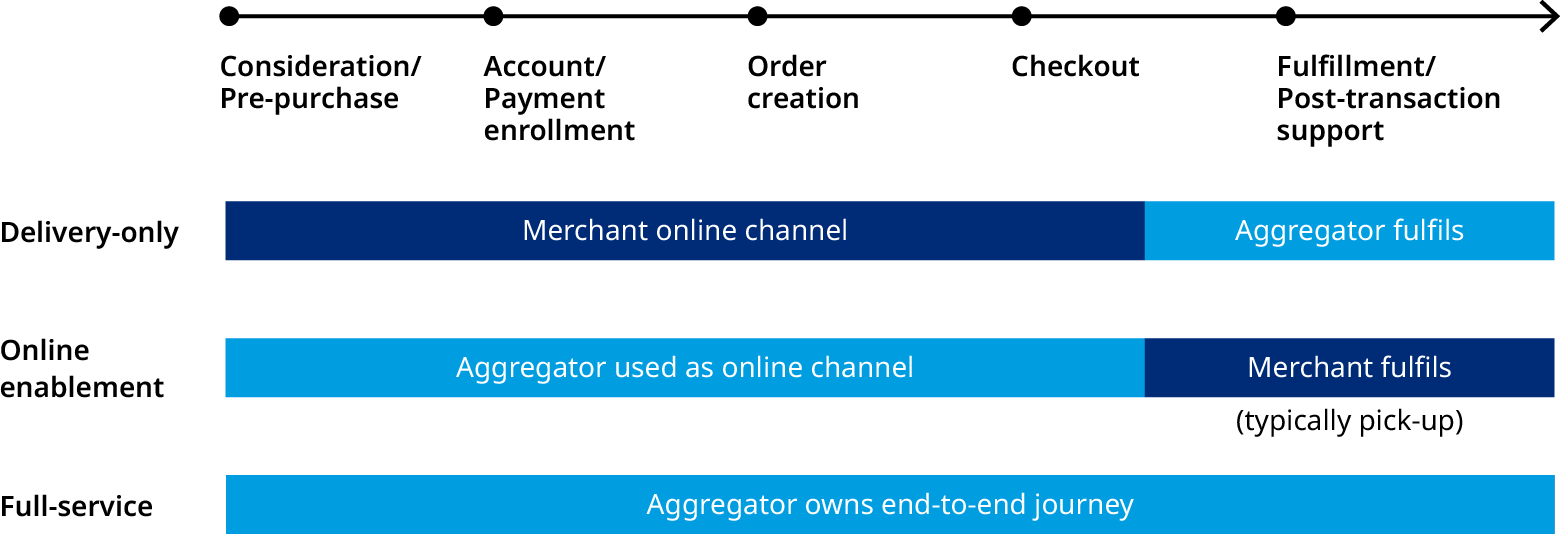

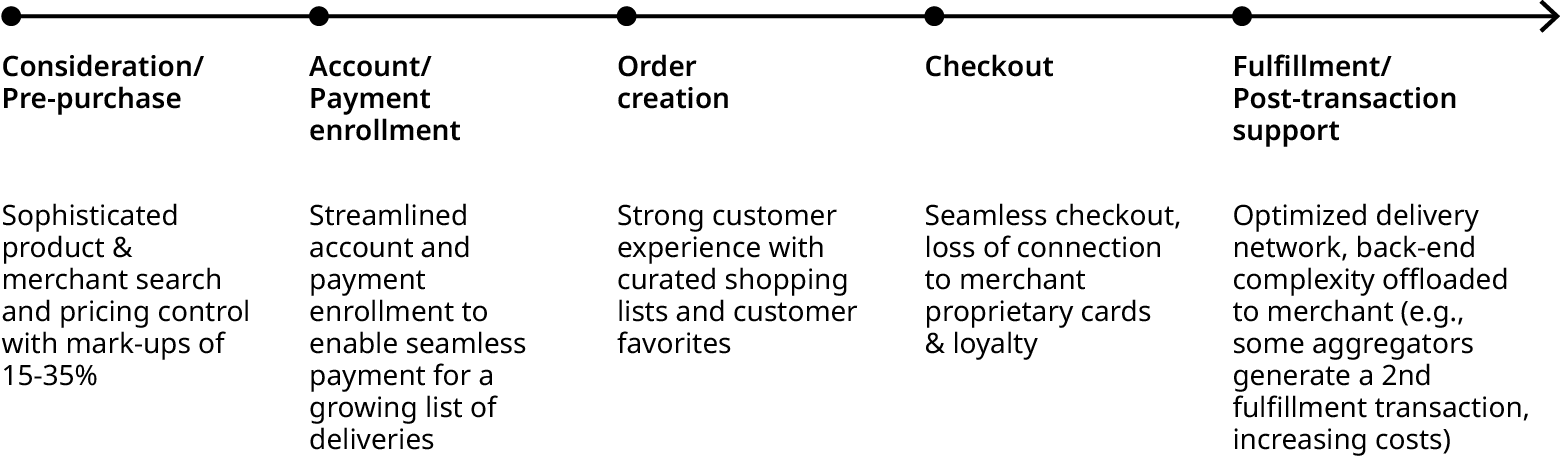

Depending on the delivery operating model selected by the merchant, the customer transaction may reside in the aggregator or in the merchant’s environment. If the checkout flow sits with the aggregator, there are several additional implementation considerations for the merchant. On the back-end, fraud and disputes need to be handled, typically through new processes and returns also need a dedicated approach. Furthermore, enabling the use of proprietary merchant-led payment methods may require new integrations and loyalty earn is difficult to offer.

Merchants also need to consider the impact of this third party led channel on their payment partner relationships that include transaction volume commitments, for instance with acquirers or card networks. For merchants, working with aggregators triggers significant strategic and operational considerations that directly impact their payments. These considerations cascade down from overarching corporate strategy to customer experience, operating model and finally implementation considerations. The strategic choices made at each step influence payments, especially costs and customer experience, considerations that are critical areas of focus for merchant payments teams engaging with delivery platforms.