It’s Time to Kick Start Commercial Top Line Growth

Roughly 160 million people get their coverage from employer group plans, making that line of business critical to an insurer’s long-term success. But carriers have been involved in a “race to the bottom” on traditional levers, engaging in RFP-by-RFP trench warfare for small share gains in a stagnant growth business line with eroding profits. This is especially true in the 60% of the group commercial business that serves self-funded employers who are eager for innovation to control their healthcare benefit costs.

To move beyond the status quo and achieve step function gains in commercial top line growth, insurers need to re-invigorate their approach. We argue that insurers need to “double-click” on the fundamental drivers to enhance core competencies (i.e. detailed analytic methods and evolved approaches across the core top-line levers) as well as be tightly coordinated and aligned across the organization (i.e. across finance, product, network, customer insights) in execution if they are going to build sustained market share growth. Only then will carriers and their partners be in position of strength to break through the status quo and help drive implementation of innovative population health models.

Stagnation

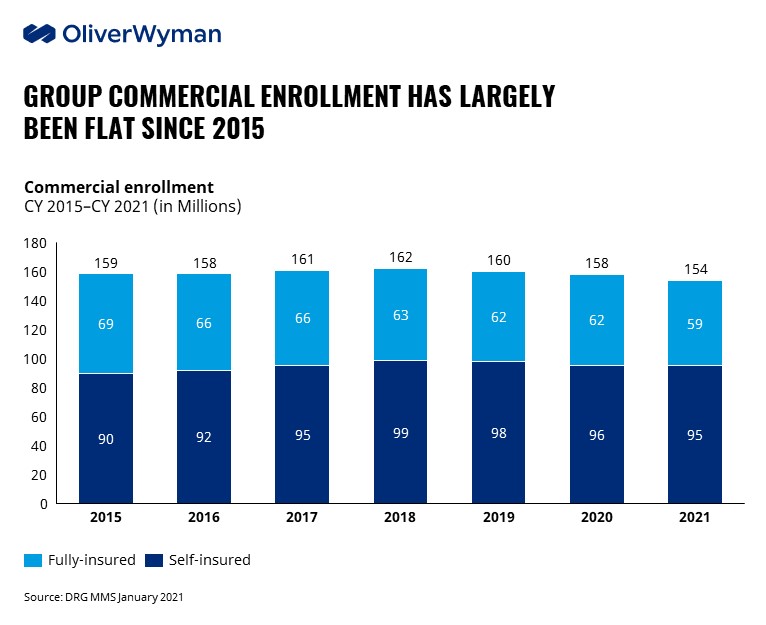

Membership and margins on commercial lines of business have been stagnant for nearly a decade, with annual pre-tax margins for self-insured lines sticking at 15% between 2012 – 2019; for fully-insured business, annual pre-tax margins hovered between 4-7% from 2016 to 2021.

There are a host of reasons why this is the case, including:

- Commercial employer covered lives are flat or declining across most segments with an aging population moving out of group coverage and into Medicare, more gig workers, and Affordable Care Act expansion

- Health benefit costs continue to outpace earnings in 2021 (+ 6.3% across all employers), putting continued pressure on employers — and their carriers - to provide affordable care

- Commercial reimbursement remains significantly higher than government rates and most hospital systems cross-subsidize to achieve profitability, creating further fully-insured commercial payor margin pressure from health systems

- Administrative services only business has grown recently and moved down market into smaller groups, further eroding overall commercial margins. And ASO margin expectations remain low to try and build membership and scale to create more market clout/buying power

- Some payers are also sacrificing margin in their commercial business to gain membership in hopes of gaining margin through other population health offerings or pharmacy rebates

- Employers are still focused on broad network access and traditional “best in breed” pricing, driving a “race to the bottom” with greater willingness to switch

- Consultants are offering their own structures and population health solutions that are now in direct competition with health plans

- Innovators and start-ups are increasingly selling direct-to-employers, creating noise but also “nipping at the heels” of plans hindering penetration of their own offerings

- “Sisyphus Effect” — new sales initiatives at lower margins offset by churn increases, exacerbated by inflation putting small group business further at risk and driving increased insurer administrative expenses

There seems to be no end in sight to the intense competitive and structural pressures all driving margins down in a no-growth market. So what can health plans do about it?

“Double Click” to Enhance and Evolve Core Growth Levers

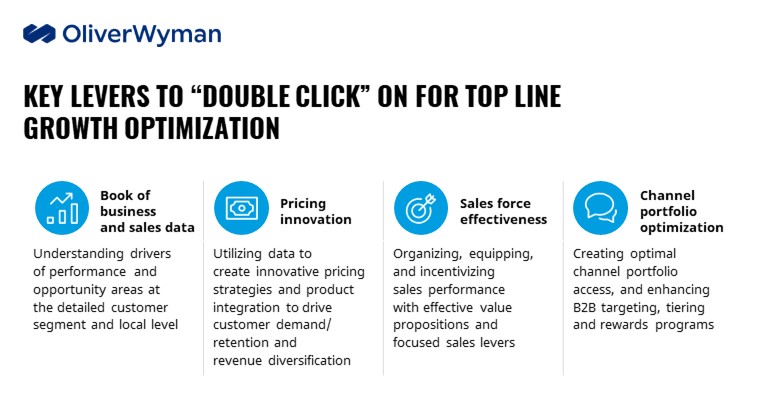

Today’s paradigm of commercial product structures and combinatorial pricing, network discounts, and basic broker incentive programs will not move the needle far enough and fast enough for health plans seeking meaningful top line growth. We’ve identified four traditional levers where insurers should throw out the business-as-normal approach and instead initiate a new playbook that better positions them for an increasingly competitive environment. Importantly each of these elements need to work cohesively around a compelling and aligned product portfolio:

- Enhanced Book of Business Insights. Many plans don’t have rigorous analysis on their book of business, drilling down into insights of where accounts are driving margin performance, where there are pockets of opportunity for further product penetration, where there are elements of the book that are at greater retention risk vs. others. Often, plans have rudimentary analytics that use only their own internal information, focus on a few KPIs, and don’t drill down into future account profiling and opportunity analysis that would allow for micro-account targeting. In addition, book of business and sales analytics need to look longitudinally at the detailed segment and market level to assess changes in close ratio, retention, margin, etc. with channel performance (see below)

- Pricing Innovation. The competitive scrutiny on ASO administrative fees has resulted in more sophisticated payers adjusting their pricing approaches as well – moving away from “combinatorial” pricing that adds several a-la-carte product prices on top of an admin base fee – to instead shift to a flat or reduced admin fee and higher monetization of plan programs through value sharing, performance guarantees, discount spreads, true product integration (versus discounts through bundling) etc. Here again having at hand the right data in a timely manner is critical, and can also lead to revenue enhancement and diversification (TPA utilization)

- Channel Portfolio Optimization. Furthermore, the changes in the distribution channel landscape require a highly strategic approach as well. PEOs, TPAs, e-brokers, insurer-owned platforms, direct to employer contracts, etc., have appeal to varying employer segments and differing clout by region. Even though these channels are relatively small volume versus the traditional broker/consultant, the lines are continually blurring also with further channel M&A and payer partnerships. One must also look at longitudinal channel partner performance at the customer segment and regional level for growth, retention/churn, sales, share of wallet across the full product portfolio and have specifically curated approaches to channel engagement and management. To have effective and reliable broker performance you need move beyond basic performance levers and bonus programs to more enhanced tiering and incent the right behaviors, and you can only do that with the right measurement systems and the right relationship with your channel partners

- Sales force effectiveness. These pricing approaches require an evolved sales organization and operational capabilities to introduce monitoring, settlement and reporting of value delivered to justify plan reimbursements. All these aspects, in addition to the proliferation of products in the group commercial space, requires an upskilled sales force that is able to execute highly consultative and nuanced sales approaches backed by compelling market messaging and high touch account servicing. Sales teams 15 years ago were selling 1-2 products and they are now selling 20 different products, with variable pricing schemes against a whole new competitor set (some of whom are also their channel partners). Revolutionizing your sales team effectiveness is a critical capability to compete.

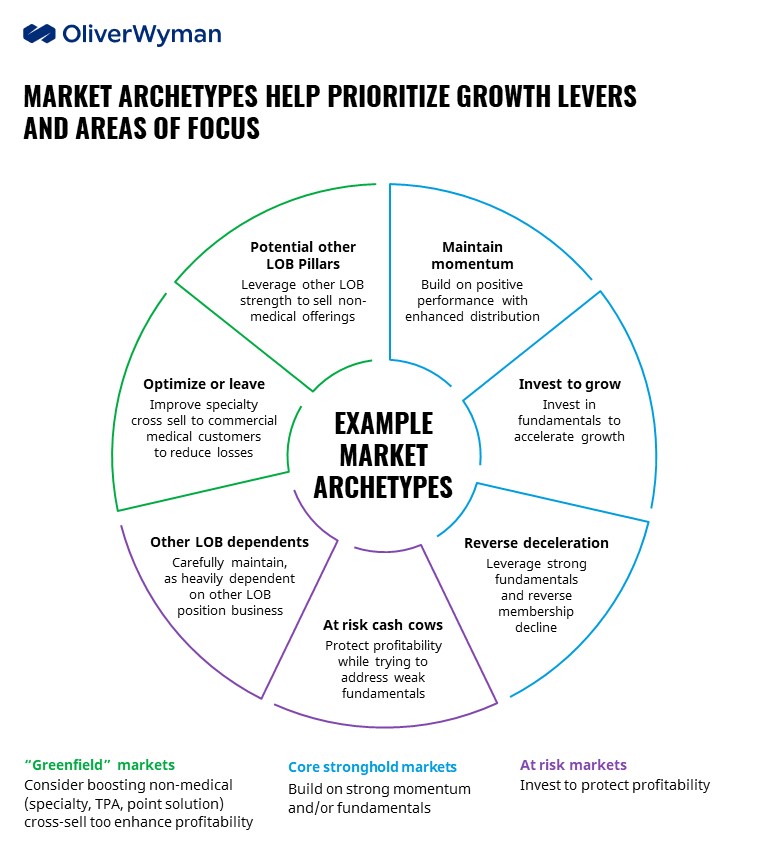

It’s important to recognize that conditions vary significantly market to market and require specific understanding of the fundamentals (network breadth and discounts, clinical performance, market share position), economics (PMPM margins, net contribution, etc.) and competitor and customer dynamics. This understanding leads to typical market archetypes which help prioritize the respective markets and to tailor top line growth strategies emanating from the detailed lever analytics.

Insights in your inbox

SubscribeCross-company Coordination is Key

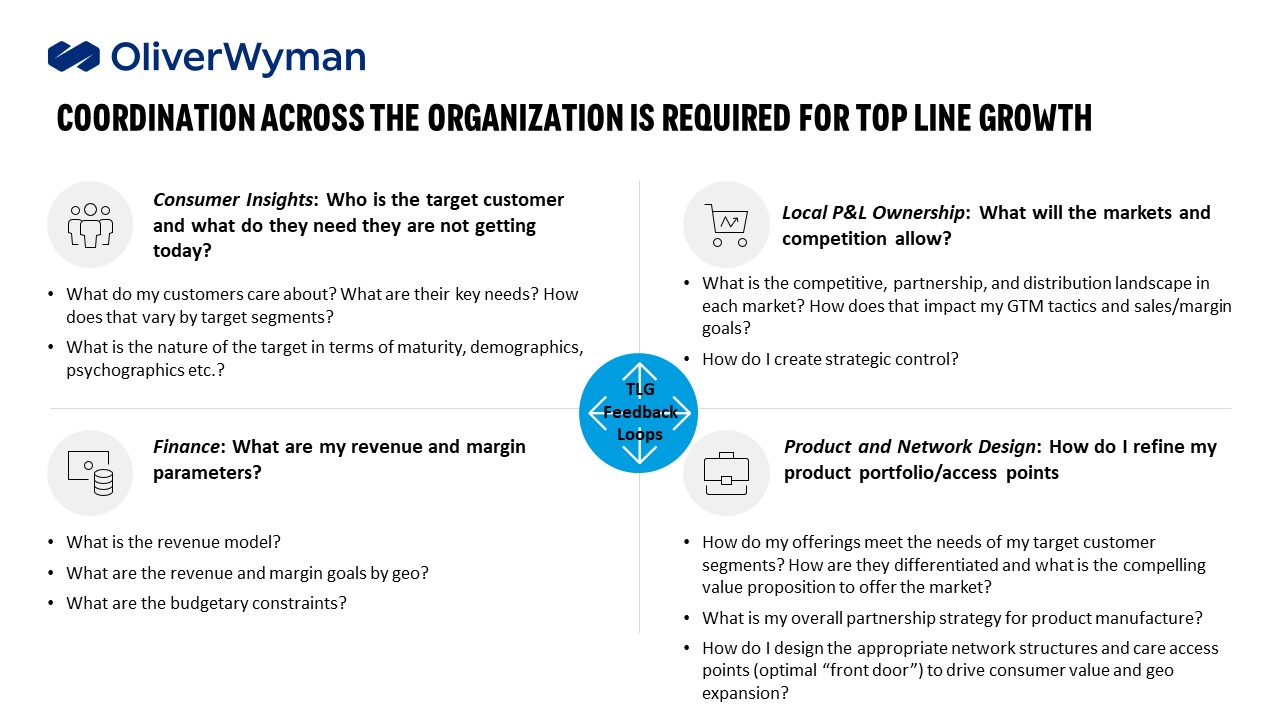

Top line growth initiatives often fail to meet expectations because communication and/or goals may not be clear or consistent across the business. For example, a market leader may be incented and driven by share growth (at the expense of margin), even though at the corporate level profit protection may be the chief financial officer’s top priority. Or product design may be developing narrow or tiered network structures that will deliver improved pricing but may run counter to specific top echelon employer requirements in-market. Or a specific market (MSA, region) may be a prime growth opportunity, but the P&L owner is directed to put resources elsewhere.

It’s imperative that the key owners of growth – finance, product design, network, P&L leader, and sales – are coordinated and have aligned incentives. This requires a consistent and clear interaction and feedback loop, where front-line local intelligence is informing corporate resources, and vice versa.

Be Relentless at Execution and Measurement

The path to top line growth is not smooth. It takes a willingness to break through the culture of complacency and stagnation. Leaders need to commit to aligning operations and building out their analytics capabilities to gain better insights into their markets. As that occurs, companies will find that they are not only able to conduct detailed analytics to uncover opportunities and close gaps, but that they can more rapidly bring innovations to the market that will drive step-function, not incremental, share and margin growth. But analytics and innovation fail if the execution and measurement is not relentless - at the local level – and properly aligned and coordinated across the entity. Only by focus, and measurement at the account-by-account level will true top line growth be realized.