Originally published in Eurofi Magazine.

The post-global-financial-crisis efforts to create a safer and more stable banking system were put to the test last year as Credit Suisse, Silicon Value Bank, Signature Bank, and First Republic all failed within the span of a few months.

Much has been written about the interlinkage of interest rate risk, bank funding, and capital in these failures. Whilst there are important lessons to be drawn in terms of deposit characterization, fund transfer pricing, and interest rate risk in the banking book (IRRBB), arguably the primary cause of these failures was the lack of a convincing business model — or management’s inability to execute on that model.

Importance of business model categorization in banking regulation

Business model analysis is a critical component within the European Banking Authority; Pillar 2 capital addon requirements are based on “a detailed analysis of the viability and sustainability of banks”.

Yet, for a long time, a simple approach to categorizing business models has been missing. As recently as 2018, the EBA authored a paper on “a novel approach to classifying banks in the EU regulatory framework”.

Business model categorization is important for two main reasons. First, it provides authorities with a benchmark for classifying institutions and supports the application of the proportionality principle to adapt capital and governance requirements to individual business models. Second, it provides shareholders with a differentiated “investment thesis” when they assess the risk/reward profile of each institution and each business model.

On the regulatory and supervisory side, more can be done to take business models into account. Different types of banks, such as local or international universal institutions, are materially different from, say, cooperative or mutual institutions. In terms of governance and organization structure, many cooperative banks put forward the principle of proportionality, since the cost of regulatory compliance can be relatively high for such institutions. Also, many have governance systems that allow clients to be elected in the governing bodies, which can make it difficult to comply with associated regulatory requirements.

In terms of capital requirements, asset mix, and shareholder structure, cooperative banks serve predominantly small- and medium-sized enterprises, and risk-weighted asset mechanisms to calculate capital requirements will result in higher capital for these institutions. In case of a deviation from minimum regulatory targets, cooperative banks might have to reduce financing capacity if direct member contributions are not forthcoming in sufficient capacity.

For a long time a simple approach to categorizing business models has been missingManaging Partner, Co-Head of Europe, Oliver Wyman

For a long time a simple approach to categorizing business models has been missingManaging Partner, Co-Head of Europe, Oliver Wyman

From an investor standpoint, the European banking sector remains challenged in terms of valuations. Despite a recent recovery, European banks trade at 60% of book value, with the spread among leaders and laggards remaining largely the same since 2021. Recognition of various business models by investors is not differentiated enough, and many banks resort to share buybacks and dividends as primary valuation-support levers.

Navigating evolving financial landscapes — the challenges and imperatives

Given the increasing correlation between the price/book ratio of a bank and its perceived strength, business model recognition is becoming increasingly important. Investors will trust bank management more to redirect capital towards business model strengthening when the models are clear and recognized by regulators.

At the same time, banking regulation and supervision need to adapt to the ever-growing importance of the non-banking financial sector and its interconnectedness with the banking system.

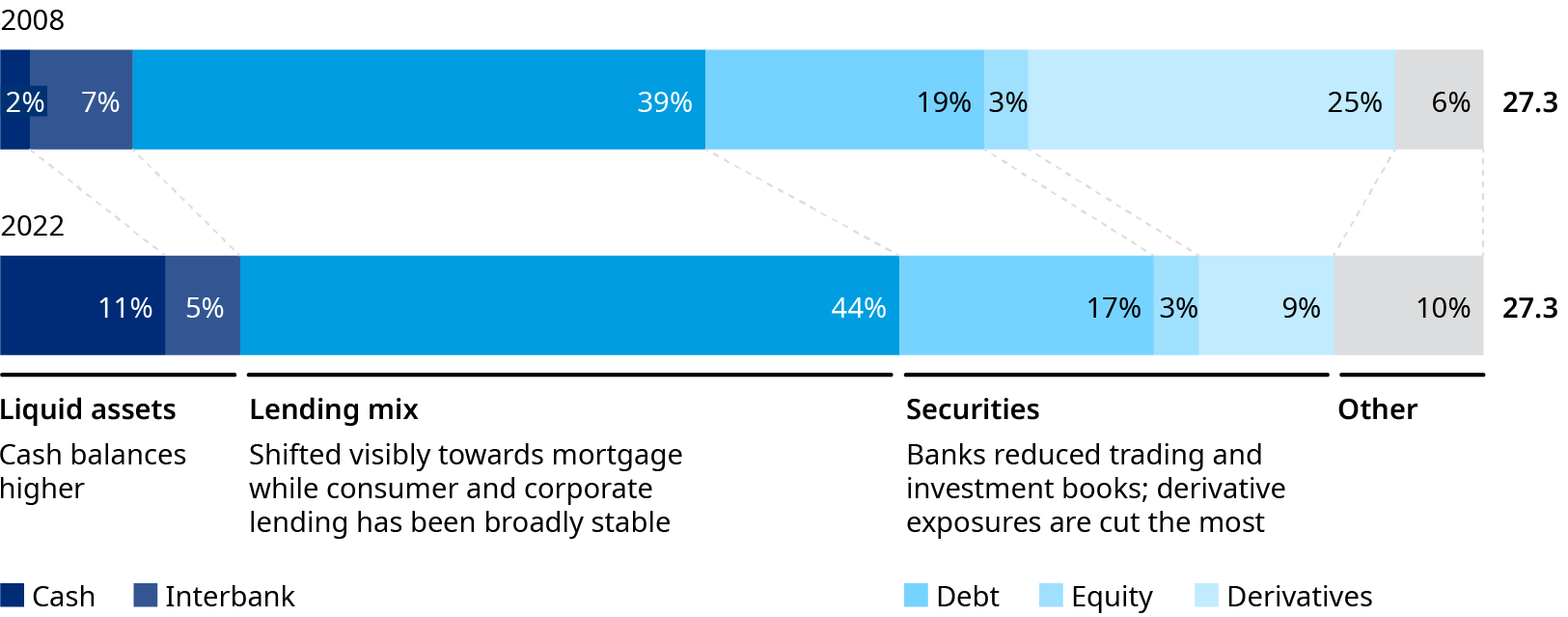

Despite the explosion of debt in the system, European Bank Balance sheets have remained stable over the past decade at 27 trillion Euros and have shifted towards mortgages and liquid assets. Return on assets has dropped as a result, impacting profitability.

Non-bank financial institutions (NBFI) have assumed a more important role as financers, gaining market share in lending from banks, often holding the riskier—and more profitable—part of the assets.

On the retail side, open banking has facilitated client information flow from financial services providers to other financial services providers but also a much broader set of institutions, including fintechs and large global tech companies. While the benefits for customers are evident, open banking could create an unlevel playing field as traditional banking players are ultimately strengthening the large tech companies’ already dominant customer data position. Thus, banking regulation and supervision should capture the services provided (such as mortgage financing, deposit taking, and advisory services), irrespective of the type of provider.

This is not an easy task — but it’s essential to support a robust, flourishing, and diversified European banking sector.

Read the original piece, here.