The drop in mainland Chinese visitors (MCVs) to Hong Kong during COVID-19 was a significant challenge to the city’s life insurance industry. However, with the full opening of the borders this year, new business activity in the first few months of 2023 shows evidence of the pent-up demand from mainland Chinese customers for Hong Kong’s life insurance, signifying an impending turnaround for the industry. To better assess the returning MCV demand, in February 2023, Oliver Wyman surveyed more than 2,000 mainland Chinese customers and further surveyed the nearly 1,000 respondents who plan to purchase insurance in Hong Kong in the next 24 months (“mainland Chinese buyers”).

Strong travel recovery and insurance-buying appetite

According to the survey, 72% of the respondents intend to travel to Hong Kong in the next 24 months and 47% are interested in buying a policy during their trip. The latter figure reaches 65% for customers from the Guangdong-Hong Kong-Macao Greater Bay Area (GBA).

Most respondents indicated they feel more inclined to purchase life insurance in Hong Kong now compared to three years ago and are eager to travel within six months. Interest is strongest for health and critical illness insurance, followed by savings and investment products, life protection, and retirement products. The surveyed buyers see Hong Kong as having a more mature and trusted insurance industry, with 58% suggesting the ability to access overseas medical resources and 56% saying a wider scope of protection coverage have become more important post-COVID-19.

Hong Kong also continues to be well-positioned as a magnet for southbound talent. The Top Talent Pass Scheme has attracted more than 20,000 applications in the first three months since launching, and 76% of the surveyed buyers also showed interest in applying.

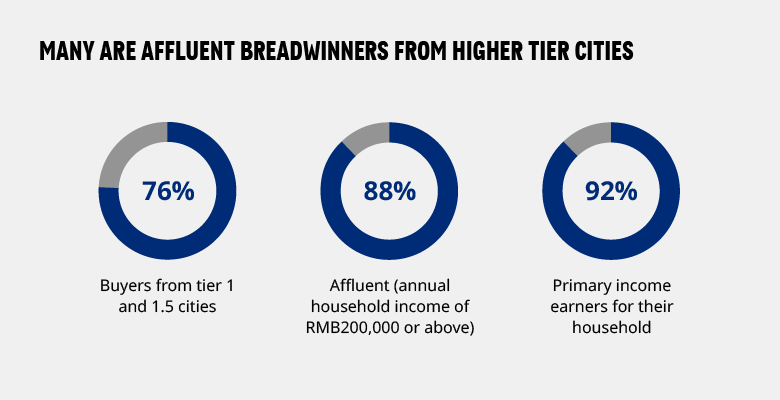

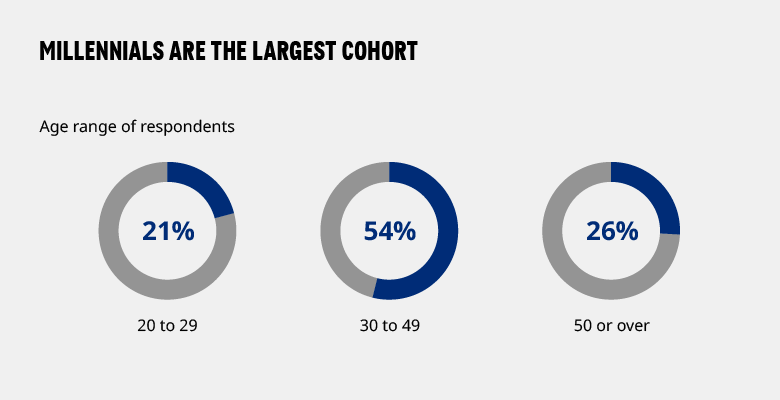

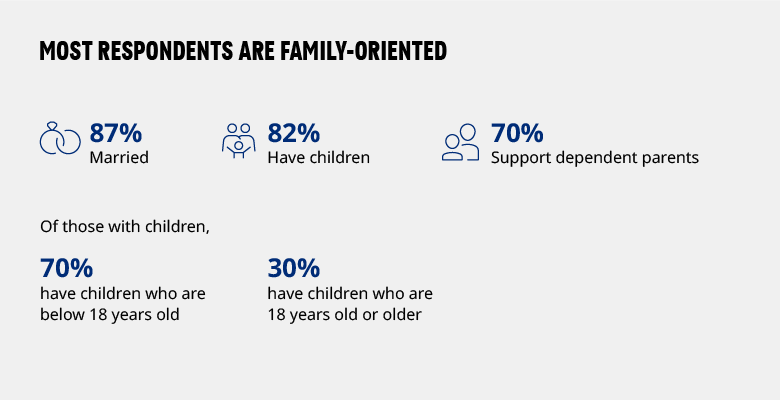

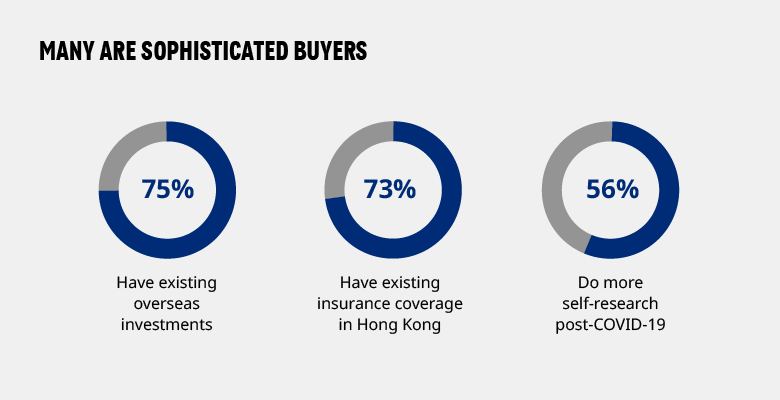

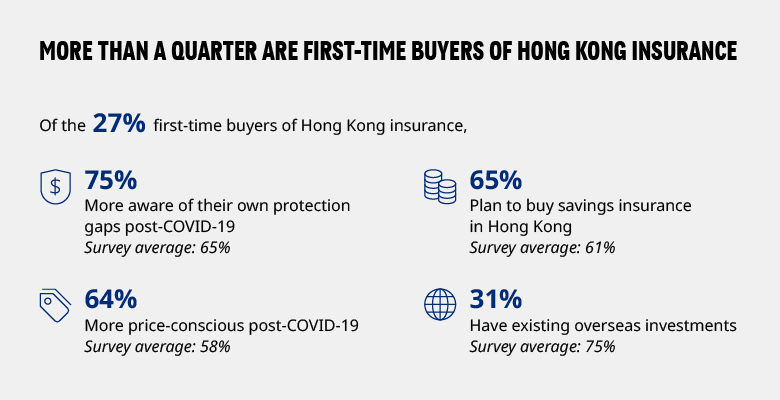

Mainland Chinese buyers’ profile, needs and preferences

Most of the mainland Chinese buyers are affluent breadwinners from higher tier cities, with millennials forming the largest age cohort. The majority of interested buyers have sophisticated buying preferences and investment knowledge, yet more than a quarter will be first-time buyers of Hong Kong insurance.

Compared to before COVID-19, the findings show several changes in the mainland Chinese buyers’ needs and preferences. About 60% of the buyers surveyed indicated an increase in concern over their life and health protection post-COVID-19. The most pressing concerns are critical illness or death, and insufficient medical funds and resources, and these risks are more worrying for younger customers. When considering health and critical illness coverage, the most critical features are disease coverage, and geographical and network coverage.

Post-COVID-19, the mainland Chinese buyers prefer products that provide long-term growth, returns with low volatility and offshore asset allocation, and 58% indicated a preference for savings products in Hong Kong compared with those in mainland China. Customers belonging to the “sandwich generation” (middle-aged adults who are caring for both elderly parents and their children) demonstrated stronger inclination for offshore investments and savings products from Hong Kong.

Of the buyers surveyed, 42% indicated they do not feel financially prepared for their future retirement and 70% indicated they plan, or are open, to living alone or at a senior home. When considering future retirement risks, mass market customers are more concerned compared to other segments. With rapid GBA integration on the back of policy tailwinds, cross-border propositions could be leveraged to alleviate some retirement concerns.

The engagement preferences of mainland Chinese buyers have also changed post-COVID-19. They are more inclined to do research by themselves and rely less on their agents and relationship managers’ recommendations when buying insurance. Only 30% of the respondents surveyed rely on these recommendations, instead viewing brand and product differentiation as more important factors for selecting an insurer.

Evolving opportunities for life insurers in Hong Kong

Despite evolving customer preferences and intensified competition, the opportunity for Hong Kong insurers is substantial. Based on Oliver Wyman analysis, the total financial wealth pool of mainland Chinese households will reach nearly $70 trillion by 2030. Within this, offshore allocation will increase more rapidly and contribute approximately 12% of total financial wealth by 2030.

Over the next decade, millennials and Generation Z will drive the growth of the city’s life and health insurance business while Generation X will transition towards decumulation. Insurers should rethink and tailor propositions to successfully address the needs of increasingly diversified customer segments.

Insurers can consider three propositions to differentiate their offerings and drive more demand.

Proposition 1: Risk protected, with flexibility

Generation Z and young millennials are more risk-aware and concerned about personal health issues and finances post-COVID-19. Modularity, which simplifies policies into fundamental building blocks and allows customers to personalize and adjust their coverage over time, may be an attractive proposition to these segments given their demand for flexibility, personalization, and value for money. Modular health offerings can lower entry barriers, ensure simpler, more transparent coverage, and enable customized benefits.

Proposition 2: Financially well, beyond insured

Post-COVID-19, there is preference for self-directed financial planning, particularly from the sandwich generation customers. To address this segment’s complex financial needs, insurers can tap into insurance-adjacent offerings and form strategic partnerships with other providers to deliver holistic financial wellness solutions spanning investment, wealth preservation and succession, financial planning and liquidity.

Proposition 3: Retire in GBA, with peace of mind

Many Hong Kong residents have expressed interest in retiring in a GBA city in mainland China, however the quality of medical care and senior support services in the GBA falls short compared to those in Hong Kong. Insurers can partner with GBA healthcare and other providers to develop a holistic solution that provides multi-city healthcare, eldercare facilities, and cross-border lifestyle and community services.

Key enablers for insurers to capture demand

There are four enablers Hong Kong insurers should consider to realizing these propositions for mainland Chinese buyers. Firstly, insurers should upskill their agents to be trusted advisors rather than transaction executors, by demonstrating discernment of customer needs and offering tailored insights and advice.

Secondly, Hong Kong insurers should identify their role and partnership approach within the ecosystems they look to participate in. By embracing themselves as orchestrators, product providers, or network connectors, insurers can focus on their core capabilities, expand customer reach and access to data, creating win-wins with other players in the ecosystem.

Thirdly, insurers should improve the disjointed cross-border customer experience. As the GBA becomes increasingly integrated, insurers who act now to minimize friction in the cross-border sales and processes now will have the edge. Insurers can localize the user experience (UX) design, embed functions into other super-apps to improve connectivity, and partner with providers with presence in both Hong Kong and mainland China.

Finally, building a winning brand is essential. Insurers should showcase themselves as a customer-centric brand. Branding strategies can be more targeted towards mainland Chinese buyers to build connection and trust.

Ultimately, Hong Kong insurers should pivot toward a customer-first approach and act now to win over the next wave of mainland Chinese buyers.