European companies weathered the immediate shock of the COVID-19 crisis far better than many expected. Revenues rebounded quickly, EBITDA margins strengthened, and liquidity remained robust thanks to unprecedented state aid and open capital markets. But as our The Crisis After the Crisis report shows, the turbulence did not end with the pandemic. Instead, late-stage effects — from soaring commodity prices to supply chain disruption — have combined with the war in Ukraine to create a new, more complex operating environment.

This next phase is not a short-lived disruption. It is a structural shift that will test corporate resilience, reshape industry economics, and force companies to rethink strategy, operations, and financing.

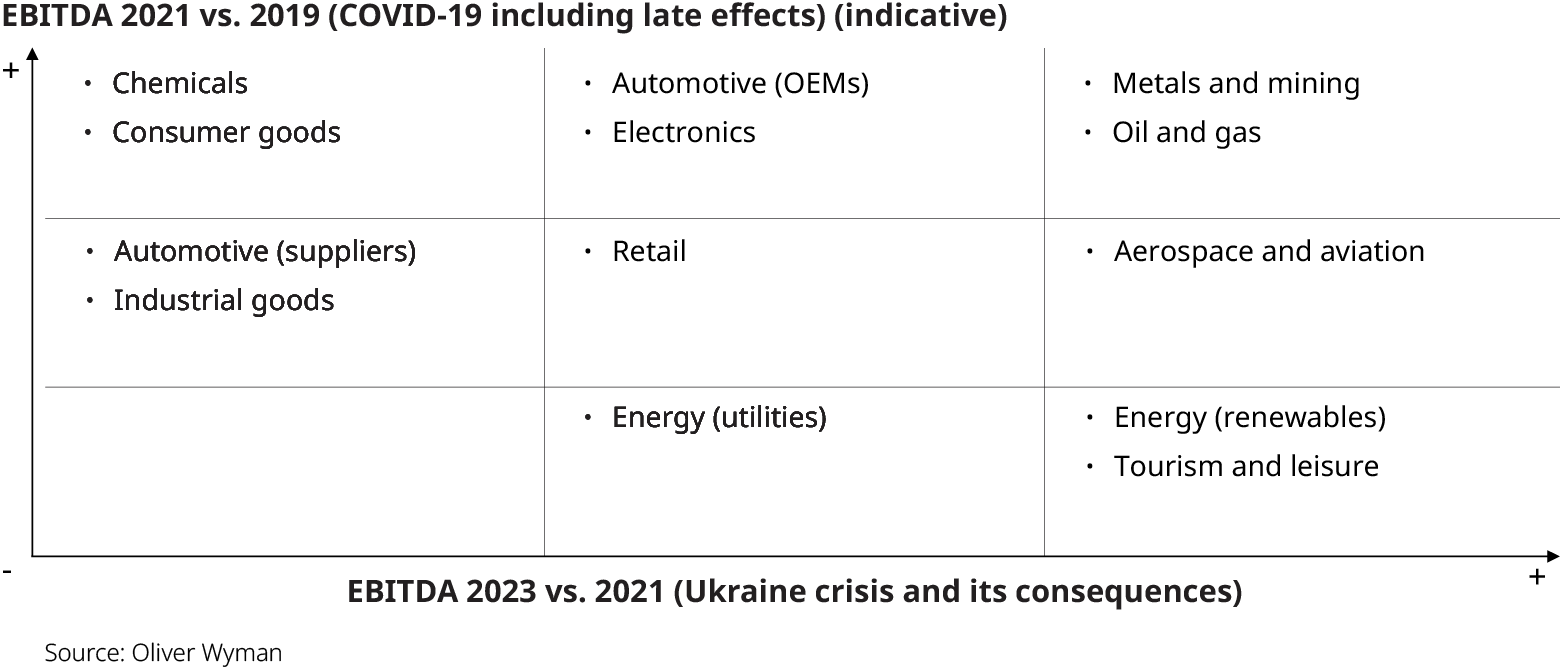

COVID-19 recovery masked deep sector differences

While the macro picture looks strong, the recovery has been uneven. Many sectors bounced back quickly: revenues in Q2 2021 were already 6% above pre crisis levels, and EBITDA margins improved by more than 300 basis points. Companies also strengthened their balance sheets, increasing cash reserves by more than 30% — outpacing debt growth and reducing leverage.

Yet beneath this aggregate resilience lies a more nuanced story. Industries dependent on mobility, such as tourism and aviation, continue to operate below pre crisis levels. Meanwhile, sectors like metals and mining saw significant growth, benefiting from strong demand and rising prices.

This divergence highlights a key theme of the report: the crisis did not hit all sectors equally, and the recovery will not either. For some industries, the pandemic’s impact is still unfolding.

Late effects of COVID-19 intensified by the war in Ukraine

The most significant challenges today stem not from demand shocks but from operational and cost pressures. Supply chain bottlenecks, commodity shortages, and skyrocketing freight rates — all legacies of the pandemic — have been amplified by the war in Ukraine.

Steel prices in Europe have risen more than 130% since 2017, and container shipping rates have increased more than 400%. Many companies lack contractual mechanisms to pass these costs on to customers, leaving margins exposed. As the report notes, “price escalation clauses are not common practice,” meaning sudden cost spikes often hit the bottom line directly.

Supply chain delays have also driven inventory levels sharply higher. Electronics companies, heavily reliant on semiconductors, saw inventories rise 32% between Q4 2019 and Q2 2021. Longer dwell times at ports — increasing from under 20 days to nearly 50 — have further tied up working capital and slowed production.

Despite these pressures, financing remains accessible. Surveyed experts rated refinancing needs and rising interest rates as relatively low concerns, indicating that capital markets remain functional and liquidity is available for companies with credible plans.

Traditional industries face the highest risk exposure

Looking ahead to 2023 and beyond, the report identifies clear differences in risk exposure across industries. Companies with global supply chains, high energy consumption, and limited pricing power face the greatest pressure on EBITDA.

Automotive suppliers, industrial production, engineering, and construction stand out as particularly vulnerable. These sectors are squeezed by rising input costs, supply chain fragility, and limited ability to renegotiate prices. At the same time, they face disruptive structural shifts — electrification, digitization, and ESG requirements — that demand significant investment.

This convergence of cyclical and structural pressures creates what the report calls a “perfect storm”. Companies in these sectors must navigate both immediate cost challenges and long-term transformation, often with limited room for error.

Utilities also face challenges, particularly around access to affordable gas and oil. However, they have more levers to pull, including shifting their energy mix toward renewables.

The report’s risk heatmap makes clear that not all industries will experience the next phase of the crisis equally. Some will continue to recover; others will face sustained headwinds.

Why investors are selective about where capital goes

Despite the challenges, the report offers a clear message of optimism: capital is available for companies that can demonstrate a credible path forward. Not a single survey respondent cited capital availability as a major concern. Banks, investment funds, and private capital providers remain ready to support companies with strong restructuring plans and clear strategies for navigating market shifts.

But capital is no longer cheap — and it will not be allocated indiscriminately. Companies must show how they will adapt to rising costs, supply chain volatility, and disruptive industry changes. Those who can articulate a compelling plan will secure the financing they need. Those who cannot may struggle.

The agenda for corporates in 2022 and beyond is clear:

- Address market changes head-on

- Adapt operations to manage rising costs and supply chain risk

- Invest in transformation to stay competitive

- Use capital wisely and strategically

As the report concludes, the crisis has become the new normal. Companies that embrace this reality — and build resilience into their strategy and operations — will be best positioned to thrive in a world defined by volatility.

Late effects of COVID 19 intensified by the war in Ukraine

The most significant challenges today stem not from demand shocks but from operational and cost pressures. Supply chain bottlenecks, commodity shortages, and skyrocketing freight rates — all legacies of the pandemic — have been amplified by the war in Ukraine.

Steel prices in Europe have risen more than 130% since 2017, and container shipping rates have increased more than 400%. Many companies lack contractual mechanisms to pass these costs on to customers, leaving margins exposed. As the report notes, “price escalation clauses are not common practice,” meaning sudden cost spikes often hit the bottom line directly.

Supply chain delays have also driven inventory levels sharply higher. Electronics companies, heavily reliant on semiconductors, saw inventories rise 32% between Q4 2019 and Q2 2021. Longer dwell times at ports — increasing from under 20 days to nearly 50 — have further tied up working capital and slowed production.

Despite these pressures, financing remains accessible. Surveyed experts rated refinancing needs and rising interest rates as relatively low concerns, indicating that capital markets remain functional and liquidity is available for companies with credible plans.

Traditional industries face the highest risk exposure

Looking ahead to 2023 and beyond, the report identifies clear differences in risk exposure across industries. Companies with global supply chains, high energy consumption, and limited pricing power face the greatest pressure on EBITDA.

Automotive suppliers, industrial production, engineering, and construction stand out as particularly vulnerable. These sectors are squeezed by rising input costs, supply chain fragility, and limited ability to renegotiate prices. At the same time, they face disruptive structural shifts — electrification, digitization, and ESG requirements — that demand significant investment.

This convergence of cyclical and structural pressures creates what the report calls a “perfect storm”. Companies in these sectors must navigate both immediate cost challenges and long term transformation, often with limited room for error.

Utilities also face challenges, particularly around access to affordable gas and oil. However, they have more levers to pull, including shifting their energy mix toward renewables.

The report’s risk heatmap makes clear that not all industries will experience the next phase of the crisis equally. Some will continue to recover; others will face sustained headwinds.

Why investors are selective about where capital goes

Despite the challenges, the report offers a clear message of optimism: capital is available for companies that can demonstrate a credible path forward. Not a single survey respondent cited capital availability as a major concern. Banks, investment funds, and private capital providers remain ready to support companies with strong restructuring plans and clear strategies for navigating market shifts.

But capital is no longer cheap — and it will not be allocated indiscriminately. Companies must show how they will adapt to rising costs, supply chain volatility, and disruptive industry changes. Those that can articulate a compelling plan will secure the financing they need. Those that cannot may struggle.

The agenda for corporates in 2022 and beyond is clear:

- Address market changes head on

- Adapt operations to manage rising costs and supply chain risk

- Invest in transformation to stay competitive

- Use capital wisely and strategically

As the report concludes, crisis has become the new normal. Companies that embrace this reality — and build resilience into their strategy and operations — will be best positioned to thrive in a world defined by volatility.

This page was originally published in July 2022.