So called “SuperApps”, digital applications that aggregate multiple services across different sectors into one-single application, have been an increasingly dominant force in Asia over the past 10 years. Examples of these include Grab, WeChat, and Alipay. Each started by addressing a singular pain point in their home market, such as rides, messaging and payments. They then expanded their value proposition to provide services from adjacent, then wholly different sectors over time and became the single dominant application through which customers would interact and consume these services on their device.

The race to build the same is starting to accelerate in Western markets. PayPal, which has announced its intention to become a SuperApp, is in the process of adding a host of new capabilities that will position themselves beyond just checkout, with in-app shopping tools and a loyalty program, crypto exchange, credit access and a savings account via a banking as a service partner.

Meta is increasingly blurring the boundaries between eCommerce, payments and entertainment with its social networking and messaging. Their experiments with WhatsApp across various global markets include in-app peer-to-peer payments, WhatsApp business accounts and a partnership with Uber which allows customers to order a ride via a chatbot without needing to open the Uber application.

While companies have publicly announced their plans to build “SuperApp” style platforms in the US and Europe, efforts in Australia are not yet as overt, despite a number of institutions seemingly putting in place the building blocks to do the same. With recent changes to the regulatory, consumer, data and technology environment we believe the opportunity in Australia for this capability is now even greater than other Western markets. Aside from it being an advanced wealthy market, with an increasingly digitally savvy consumer base and high penetration of digital services, the Australian Government’s introduction of Open Data legislation under the Consumer Data Right (CDR) is a SuperApp accelerator.

CDR is designed to give consumers control over how their data can be accessed and shared securely through digital channels. To date, it has been rolled out to the banking industry (starting with authorised deposit-taking institutions). Unique to Australia, the CDR regime will be extended to include multiple non-bank sectors, starting with major energy retailers in late 2022, and followed by telecommunications and ‘open finance’ which includes general insurance, superannuation, merchant acquiring and non-bank lending. Major financial institutions are already working hard to move past compliance obligations and focus on how the CDR data environment can streamline existing services and operations, and even transform the way in which financial products are provided to consumers. With the extension to different industry sectors, the barriers between data collection and service provision cross sector could be materially reduced, opening the door for integrated solutions and the rapid emergence of a SuperApp capability.

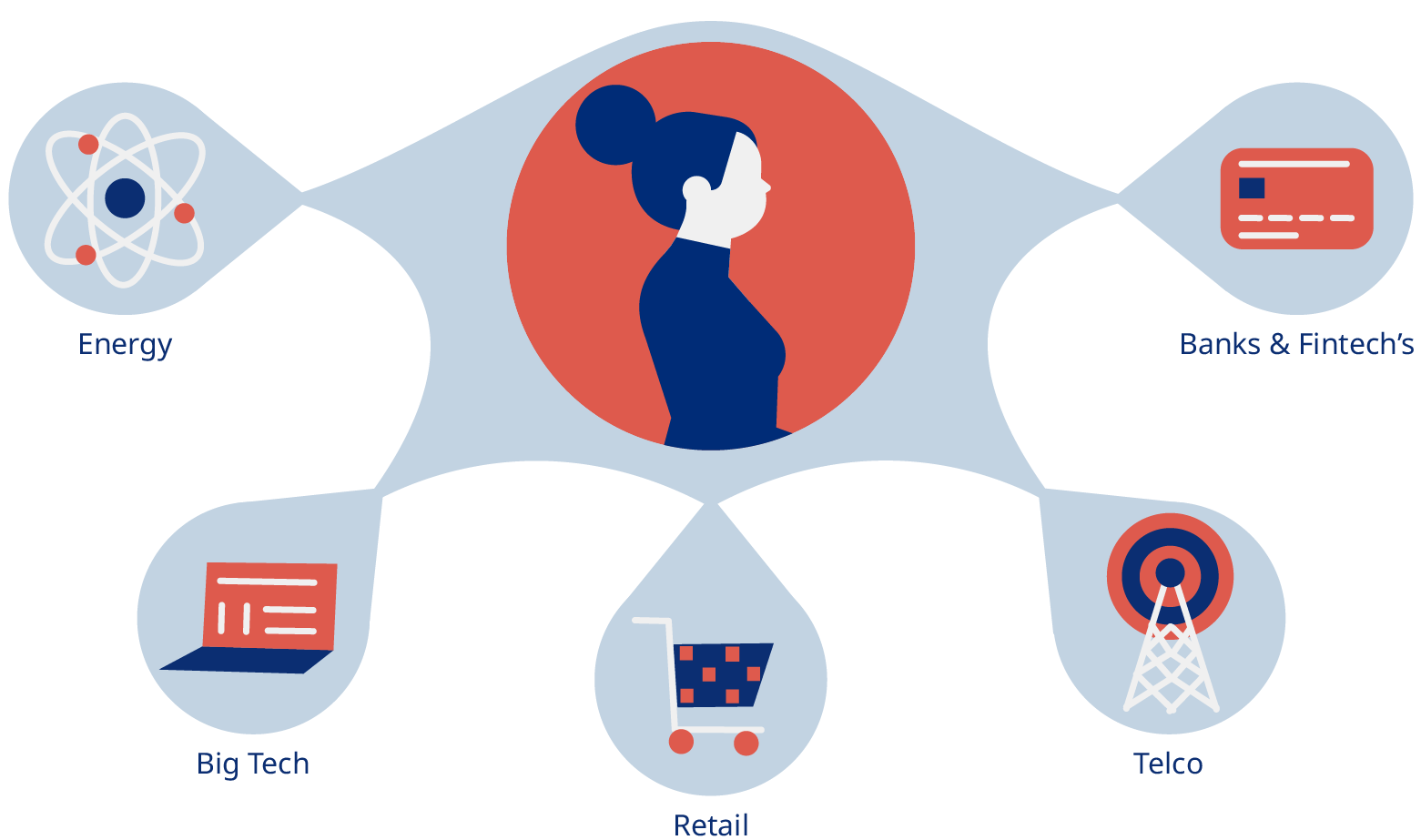

We expect that the front runners in the race for a SuperApp will be big tech seeking to grow through their payment services, the major players in banking, telecommunications, and energy seeking to consolidate their role as a one-stop shop for consumer utilities, and innovative startups hoping to steal a march on the former by building a consolidated services interface through which specialist utility providers can distribute their services at scale.

In Australia, the big banks have a head start due to their large customer bases, high app engagement scores and first access to the CDR ecosystem. A number of recent fintech partnerships and moves by internal venture arms to acquire tangential sector businesses are already resulting in more products and services being embedded in their apps which could be considered as the preliminary building blocks for a SuperApp. On the other hand, CDR opens up new areas for innovation, benefiting other industries such as telcos which already have valuable capabilities in trust, personal device connection and reach into customer’s homes.

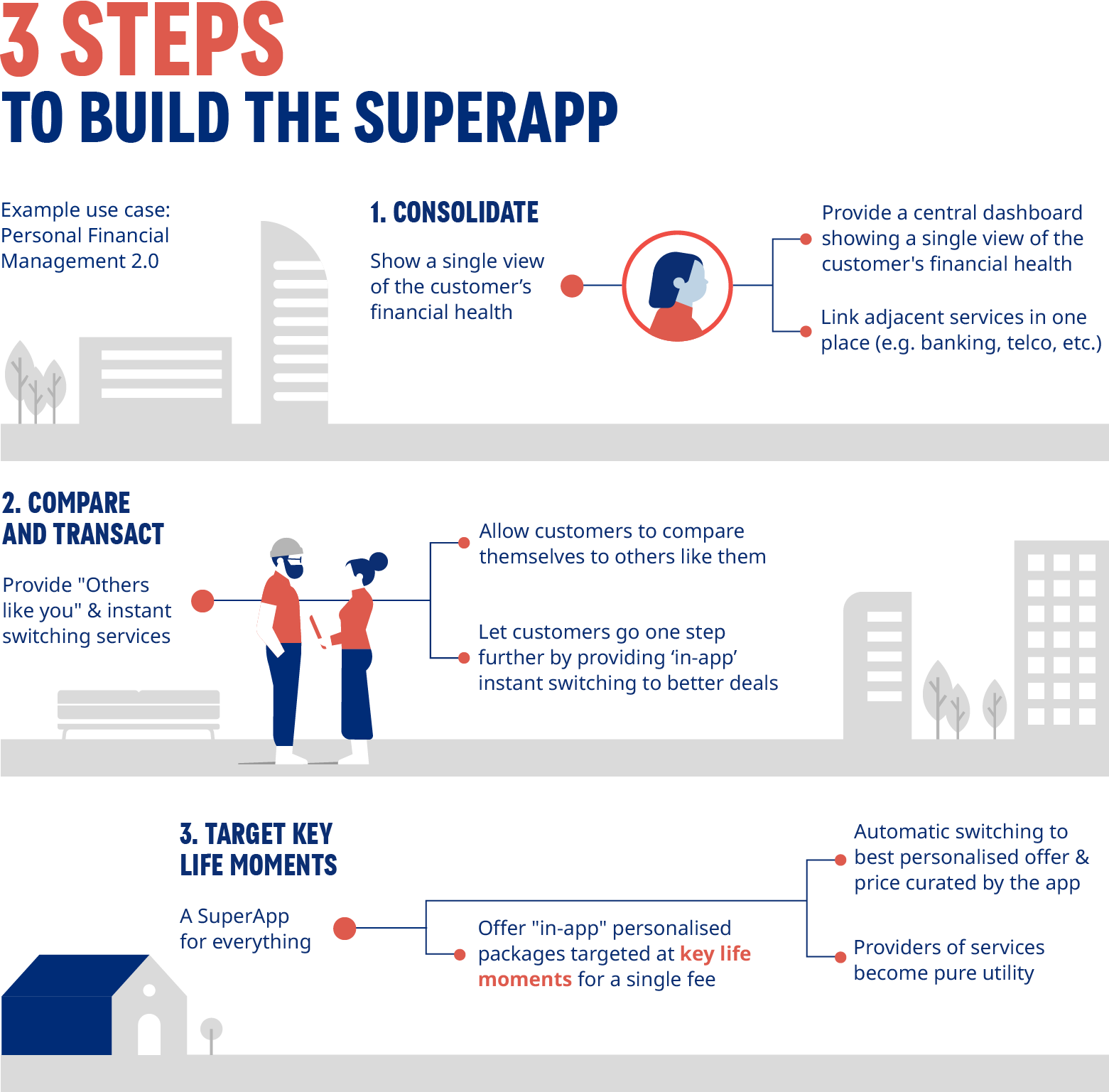

On this pathway, the successful SuperApp in Australia would start by consolidating the customer's data from their multiple services and products in one place, e.g. providing a single view of the customer’s financial health through customer-entered data initially, and through open data. Imagine a banking app that would quickly and easily show a consumer not just their banking products (across all banking service providers), but the dates, amounts, provider details, and T&Cs (where applicable) for your energy, telecommunications, insurance (health, home and contents, life, car etc.), super, and all other subscriptions services in one place.

Once this view is provided, the next step would be to allow customers to compare these services to ‘customers like you’ based on the detailed digital transaction data that would allow in depth comparison from their specific consumption habits – previously the domain of entities only within those sectors. With this in place, instant switching would be enabled through API interfaces to service providers to enable real time quotes, application and service activation based on the customer usage data in the already authenticated environment. This would allow customers to move to better deals with a click of a button, all within the SuperApp.

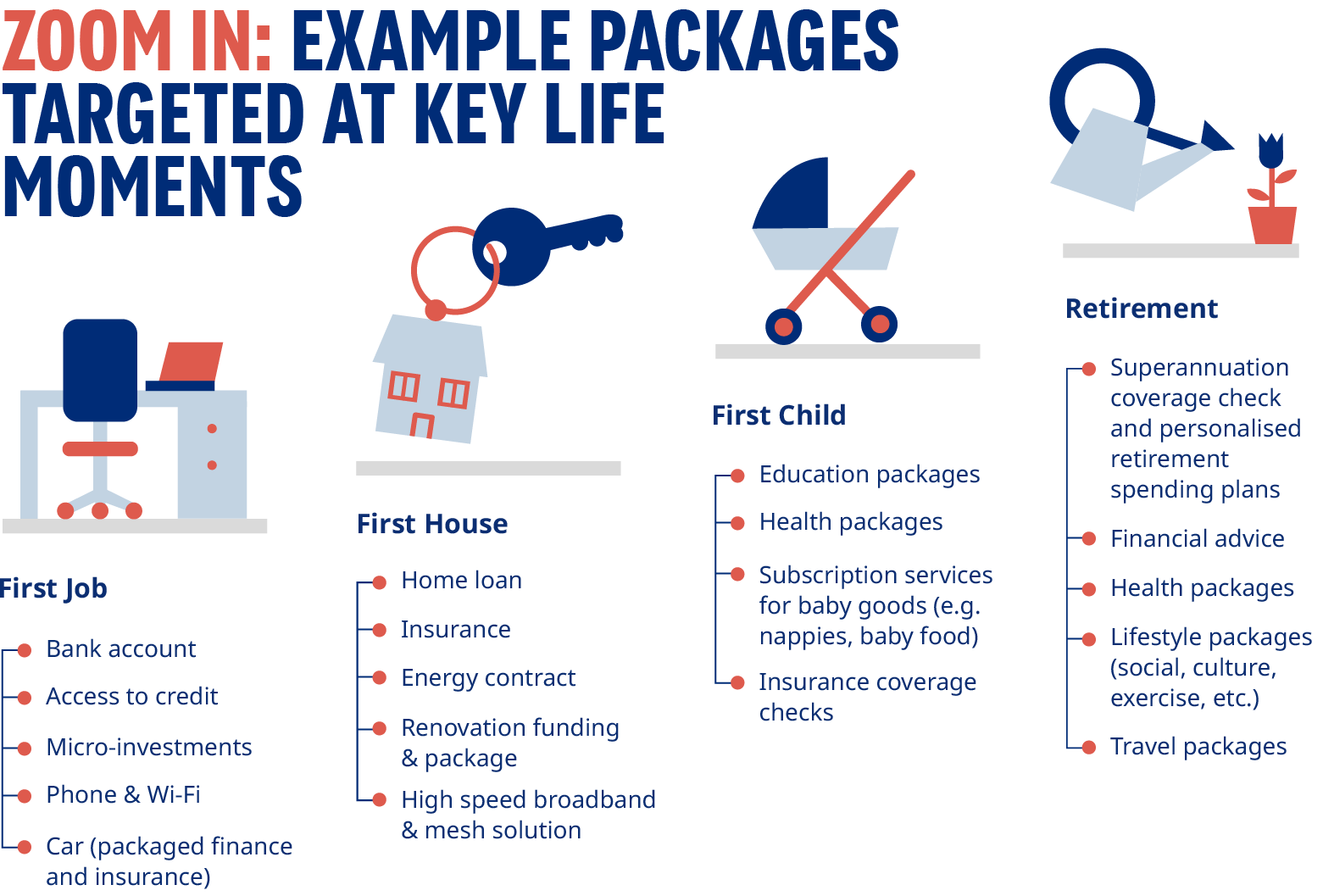

The final step would then be to bundle packages of services to target key life (and service switching) moments – first job, first house, first child, retirement etc. In this scenario where the bank plays the primary contact, your new house and mortgage will come fully loaded with an energy plan, telecommunications bundle, installed Wi-Fi, home & contents insurance tailored uniquely to your personal circumstances and provided through the app based on “customers like you”. This bundle has zero application requirements, full transparency on how each service compares, and instant “on” as all the data and authentication are already handled via the app. Here the bank owns the consumer relationship, and all other services become pass through utilities, continuously reviewed to allow “one click” switching based on changes to life moment requirements or new service updates. As SuperApps emerge in Australia, it will have significant implications to the financial service, telecommunications and energy landscape presenting new risks and opportunities. It is time for the market participants to respond.

Below we explore an example use case for the next generation of Personal Financial Management, how it could expand into an Australian SuperApp and evolve to serve key life moments.