Globally, the pandemic has negatively impacted businesses, and small and medium-sized enterprises (SMEs) have been especially vulnerable due to their smaller balance sheets. In many countries in the Asia Pacific region, SMEs are the largest employment and tax revenue source. They account for between 52% and 97% of total employment in the ten ASEAN Member States. The fallout of SMEs struggling to survive could endanger the whole economy.

Banks can play a crucial role in minimizing the negative impacts on SMEs. They can also use this opportunity to revamp their SME offerings and thus capture new revenue streams, improve client servicing efficiency, and improve their risk exposure and asset base for the SME segment.

Oliver Wyman conducted a survey and social listening analysis on over 10,000 SME customer interviews and online posts. The research unveiled that there are significant underserved areas in the SME banking market. Moreover, a growing number of non-bank competitors and new digital banks have been providing SME-specific financial services offerings, which lead to the erosion of pricing power typically enjoyed by banks.

SMEs appear ready to switch providers, and are open to a digital-only offer

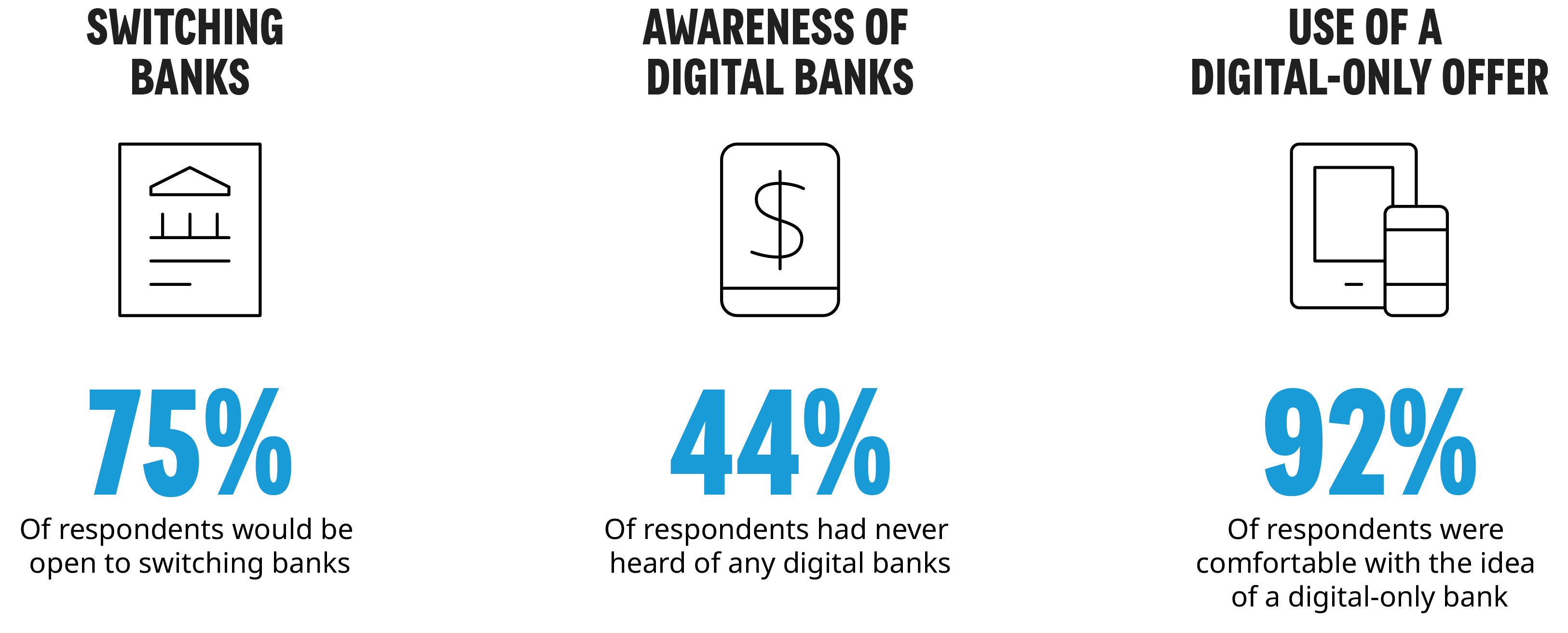

Our survey shows that SMEs have been reasonably predictable, with 75% of them expressing little to no loyalty to existing banking relationships. They are quite price-sensitive and will switch if lower-cost options provide a similar level of service. SMEs also welcome self-service digital channels, with more than 90% indicating they are comfortable with them. What they value is the ease of accessing information and quick turnaround times to queries and applications.

Perhaps one silver lining for traditional banks is the lack of awareness of pure-play digital bank propositions among SMEs. Nearly half of the respondents have not heard of any digital banks. However, this is unlikely to continue as new entrants scale up commercially and raise capital to acquire customers.

Reimagining the SME Banking Experience

Banks need to consider four areas to reinvent their SME banking proposition. Firstly, banks need to move beyond a product and service mindset to one that aims to address the needs of SMEs. This would require banks to develop propositions that are not just banking products but also digital solutions and advisory offerings, each with their own unique commercial models.

Secondly, as banks move towards solution-driven propositions, there will undoubtedly be services, features, or communities that banks will need to source from partners or vendors. Unlike technology companies, this ecosystem-building approach is unnatural for most banks due to concerns over sharing economics, data privacy, risk management, and client retention. While these issues have not disappeared, banks will need to find ways to rapidly launch and evolve these propositions with third parties as it is cost-prohibitive for banks to build these capabilities in-house. Instead, banks must develop commercial, operating, and technology models that allow partners to be brought in to address specific SME needs.

Thirdly, bringing non-traditional banking solutions and third-party solutions together would require a thoughtful approach to how banks engineer customer touch points, service efficiency, and service resiliency. While there has been a lot of attention in building better interfaces and building customer journeys that support multiple channels, banks also need to build or source technology infrastructure that provides interconnectivity between a variety of third-party data producing and data consuming applications.

Finally, banks can make use of new data sources made available through these digital propositions to launch new banking products, make decisions on portfolio management, facilitate loan origination, and improve RM coverage among their respective SME client bases.

This report was also authored by Keat Lai, Independent Consultant.