Asia Health Ecosystem Series, Part 1: Digital Partnerships for Health Insurance

Editor's Note: Originally published on Oliver Wyman Insights, this is the first in a series of articles on emerging health ecosystem partnerships in Asia.

WHAT IS HAPPENING GLOBALLY – AND HOW SHOULD ASIA PREPARE?

In the past, healthcare incumbents – traditional health insurers, hospital providers, and pharmaceuticals and device manufacturers – negotiated costs and fees in a black box, and consumers had little say. Like many industries, however, healthcare has been disrupted by the introduction of digital technology, which is enabling the use of advanced analytics for many applications such as increasing cost and care quality transparency and greater access and choice, for both clinicians and consumers. A 2018 Oliver Wyman survey of healthcare consumers in the United States showed that:

- 35 percent of respondents would accept receiving care through telehealth, an increase of 12 percentage points since 2015

- 45 percent of respondents trust their primary-care physician to monitor their health and wellness through wearable technology

- 63 percent of respondents would be willing to share personal health information to ensure their medical care is of the highest quality possible

In Asia, the digital health ecosystem is likewise thriving, inspired by these global trends. Many new startups and disruptors have entered the game, with 294 Asian healthtech funding deals closed in 2018 alone, according to Galen Growth Asia. The balance of power, decision-making and transparency has started to shift from physicians to consumers, creating new sites of care in the home and in the cloud. In this new environment, healthcare incumbents must now defend their relevance and compete with digital players for a share of the growing consumer health spend. Health insurers are not only paying for sick care in the hospital setting but are also increasingly funding non-conventional methods of care – virtual, home-based, and even simple machine learning/artificial intelligence, such as AI “doctors” and symptom checkers.

In Asia, this greater availability of digital health solutions may also have implications for the future supply and demand of health insurance. There are three major market forces that we believe will reshape the role of health insurance in the near future:

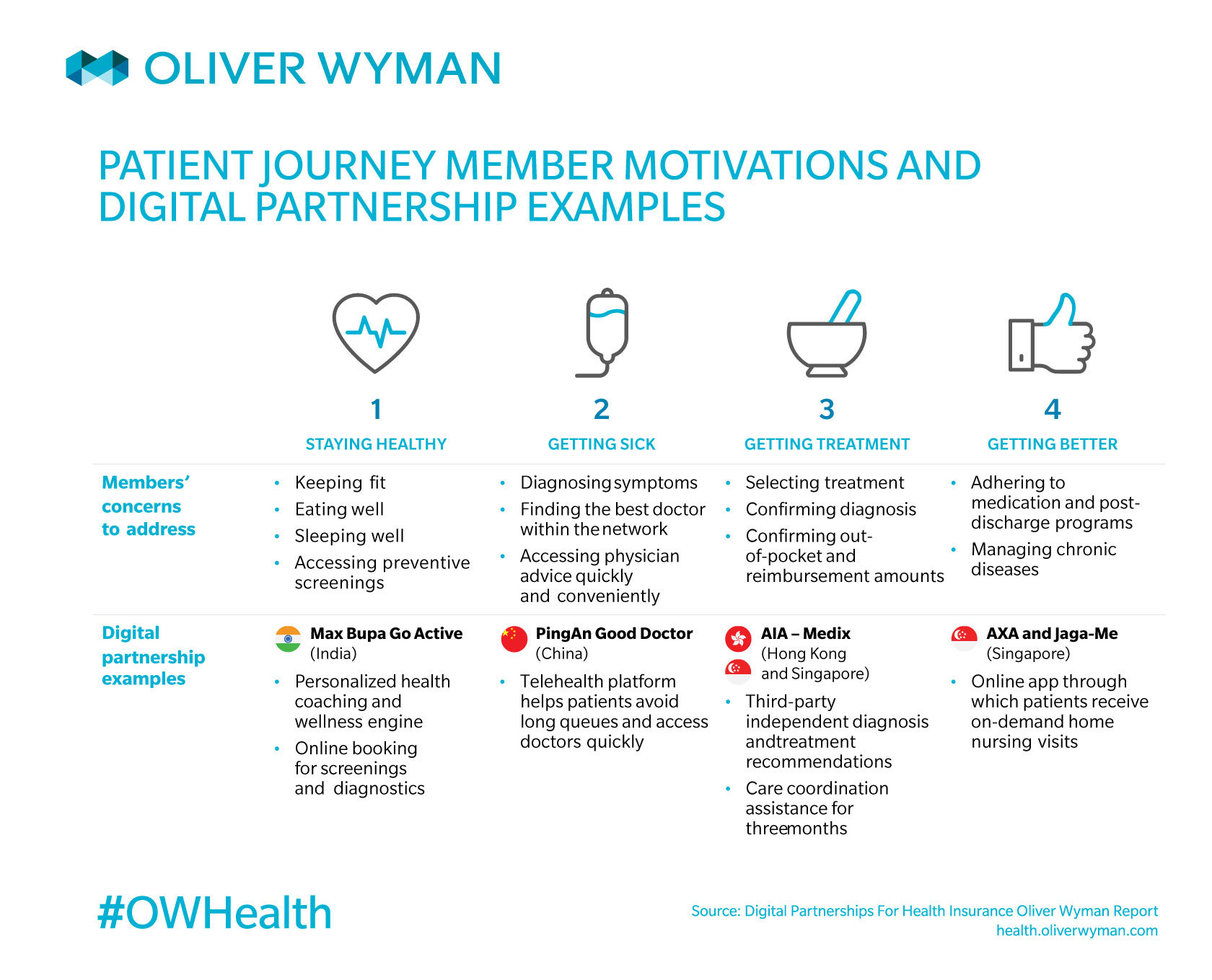

From products to services. Insurance products have traditionally reimbursed medical expenses and procedures. Today, insurers are seeking to extract more value along the patient journey by intervening long before a claim is incurred and offering integrated services alongside their core products. These services range from lifestyle-related benefits to condition management.

From one-size-fits-all to customized. Legacy products seemed to cover many services and treatments a member would likely never utilize and not enough of their most common or most likely needs. Insurers have opened new customer segments by offering more personalized products and features tailored to different member needs and specific membership bases.

From clinical to consumerized. Across industries, products and services are shifting towards consumerization, and healthcare is no different. We expect this trend to accelerate with the democratization of data through greater access to health records, provider ratings, and self-diagnosis tools. Governments may play the role of catalysts here, as pricing transparency can help to level out costs between public and private facilities.

Health insurers risk losing market share if they fail to adapt.

WHAT ARE THE IMPLICATIONS FOR INSURERS IN ASIA?

Amid such market forces, health insurers risk losing market share if they fail to adapt. At the same time, the rapidly changing landscape provides an opportunity for insurers in Asia to break down traditional boundaries and adopt new roles and business models.

In the United States, indemnity products have largely been replaced by an alphabet soup of new plan models: health maintenance organizations (HMO), preferred provider organizations (PPO), consumer-driven health plans (CDHP) – and, now, accountable care organizations (ACO). In contrast, the health insurance offering in Asia has not changed dramatically for decades. Basic programs usually cover inpatient services only and exclude preventive services and screenings, outpatient medicines, and holistic care. Member coinsurance and co-payment are not standard, and health records and many processes, from eligibility to claim submission, are still paper-based.

The relatively large gap between health insurance in Asia and mature markets presents significant growth opportunities for insurers to do the following:

- Expand the portfolio: Offer completely new health products or features beyond basic indemnity and deliver more value for members

- Broaden the market: Access untapped, previously uninsured members, especially as digital channels and partnerships create new introductory touchpoints

- Differentiate to compete: Offer exclusive services and privileges, which can help gain market share

Consumer appetite for innovation is also growing. Private health insurance customers in Asia are looking for services, such as wellness benefits, that are differentiated from public (or universal) healthcare, which is often associated with poor user experiences. Insurers can instead focus on the long game and build loyalty from early on with new members. For example, Asia’s Millennials will increasingly associate brands like Manulife and AIA with their wellness platforms, which present opportunities to foster trust and associate the brand with delightful experiences and rewards while they are healthy, rather than being exclusively associated with often unpleasant claims interactions. Insurers can also collect data on behavior and life event signals, enabling them to approach members at appropriate times for considering new insurance products, such as starting a family.

There are also some broader environmental characteristics in Asia that could enable the region’s insurance industry to “leapfrog” into the digital health age. Many of the world’s leading health technology companies are now based in Asia. Some insurers have benefitted from this proximity, as has happened in China’s rapidly digitizing healthcare market. In the same vein, investment in health technology is growing rapidly: Asia Pacific investment grew at a compound rate of 50.9 percent between 2014 and 2018, compared to only 17.8 percent in the US, according to Galen Growth Asia. Furthermore, many countries in Asia have regulatory environments that enable digital proliferation. Japan and China, for example, have comprehensive AI national strategy plans. Singapore has introduced a fintech regulatory sandbox to drive innovation, including in the insurance sector.

At the same time, incumbents face competitive pressure from big global and Asian technology players, as well as from other industries. Technology companies are building digital platforms in order to rapidly offer integrated healthcare services like telemedicine and smart devices to their large membership bases, and telecom operators have even entered healthcare by providing privileged access to digital health services. However, insurers have assets they can leverage – particularly their scale and large membership bases – to fight off some of these threats and extend their role in the patient journey. However, doing this alone would be challenging, given the significant investment required to develop new capabilities and attract the right talent.

The pairing of insurers with these solutions, many of which are digital start-ups, makes sense. Insurers provide scale and access to a captive membership base, while the startups provide new capabilities and services beyond the insurer’s core competencies. They can make this new value available to their members without having to shoulder significant investment to build it in-house.

Furthermore, combining various partnerships into one integrated user experience forms the beginning of an important business-to-consumer health ecosystem, which provides opportunities for more member touchpoints and paths to influence or enable better care. Building their own health ecosystem redefines the role of the insurer with the goal to:

- Integrate services with core insurance products

- Leverage data and analytics across services

- Create one, seamless user experience

- Coordinate care between each step of the journey

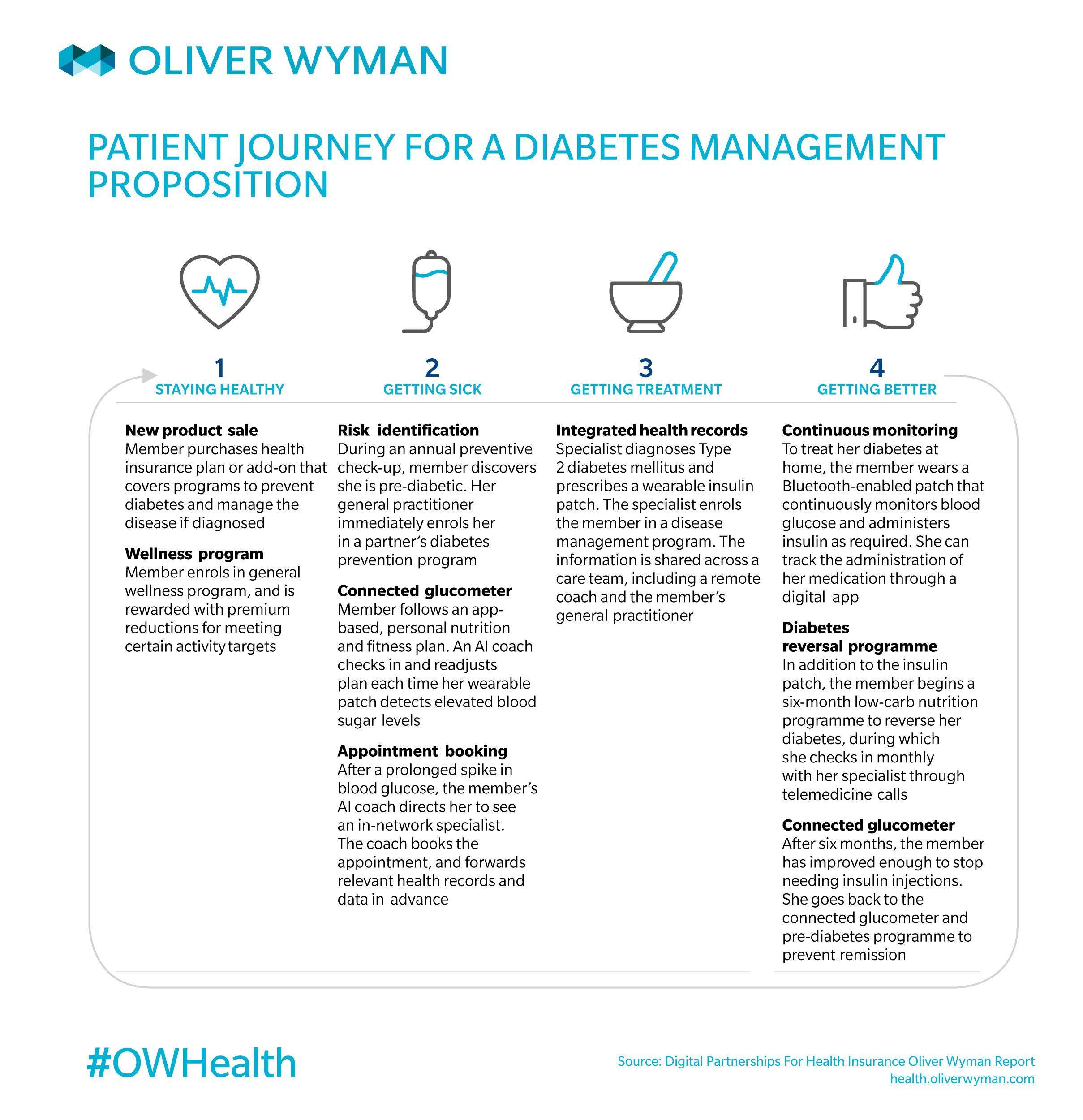

For example, Exhibit 2 shows how an Asian health insurer could offer a new diabetes ecosystem proposition across the patient journey. Whereas in the old model, the insurer would intervene in step 4 when the disease has progressed and cost has been incurred, the integrated partnerships can enable earlier action (and thus preventing steps 3 and 4, if steps 1 and 2 are successful). This proposition effectively integrates these point solutions to serve a greater purpose and keeps overall lifetime cost per diabetic patient lower than without any intervention at all.

The other advantage in this model is that the health insurer becomes the control center. Firstly, it gatekeeps the member’s access to solutions and can collects data along the way. This can be used later in predictive analytics to intervene early and reduce the need for future, costly spending on treatment. As an additional bonus, the insurer can potentially earn transaction and hosting fees by facilitating the revenue flow from the member to the solution providers.

WHAT ARE THE OPPORTUNITIES?

To develop these new consumer-focused health ecosystems, insurers will first need to design their ecosystem objectives and ambitions; then select the right partners to offer the component services; and finally integrate those partnerships through a go-tomarket approach.

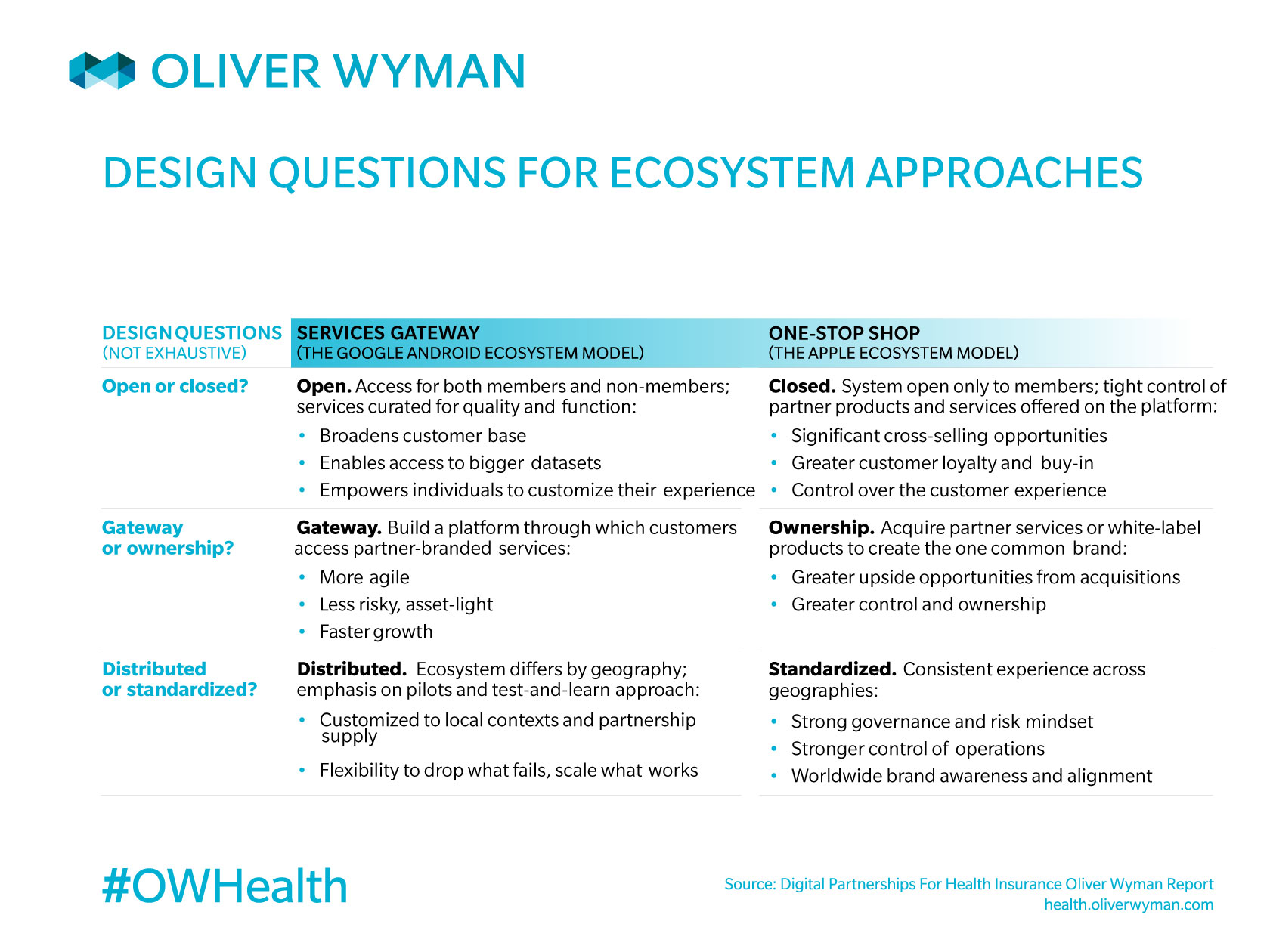

1. ECOSYSTEM DESIGN

As Asian health insurers consider the many opportunities ahead, they should first set their potential ambitions in the spectrum of ecosystem approaches:

The above options represent two ends of a spectrum. In reality, most approaches will fall somewhere in the middle. However, by defining an ecosystem ambition and strategy early on, an insurer will avoid an ad-hoc approach to partner selection and ensure that all partners integrate into a whole that is greater than the sum of its parts.

2. PARTNER SELECTION

There are many partnership opportunities across the patient journey, and insurers will need to focus on their objectives for each partnership – such as the particular ecosystem needs it will solve. Some insurers, such as Zhong An, have a gateway model partnering with a large number of companies and iterating rapidly to quickly improve products and understand what works best in the market. Other insurers pursue longer-term, exclusive partnerships to develop a one-stop-shop model, such as Prudential’s recent partnership with Babylon Health.

Key partnership selection considerations include the following:

- Competitive advantage or differentiation

- Contribution to the existing ecosystem

- Customer segments served

- Expected return on investment and timing

- Clinical, reputational, cost, and regulatory risks

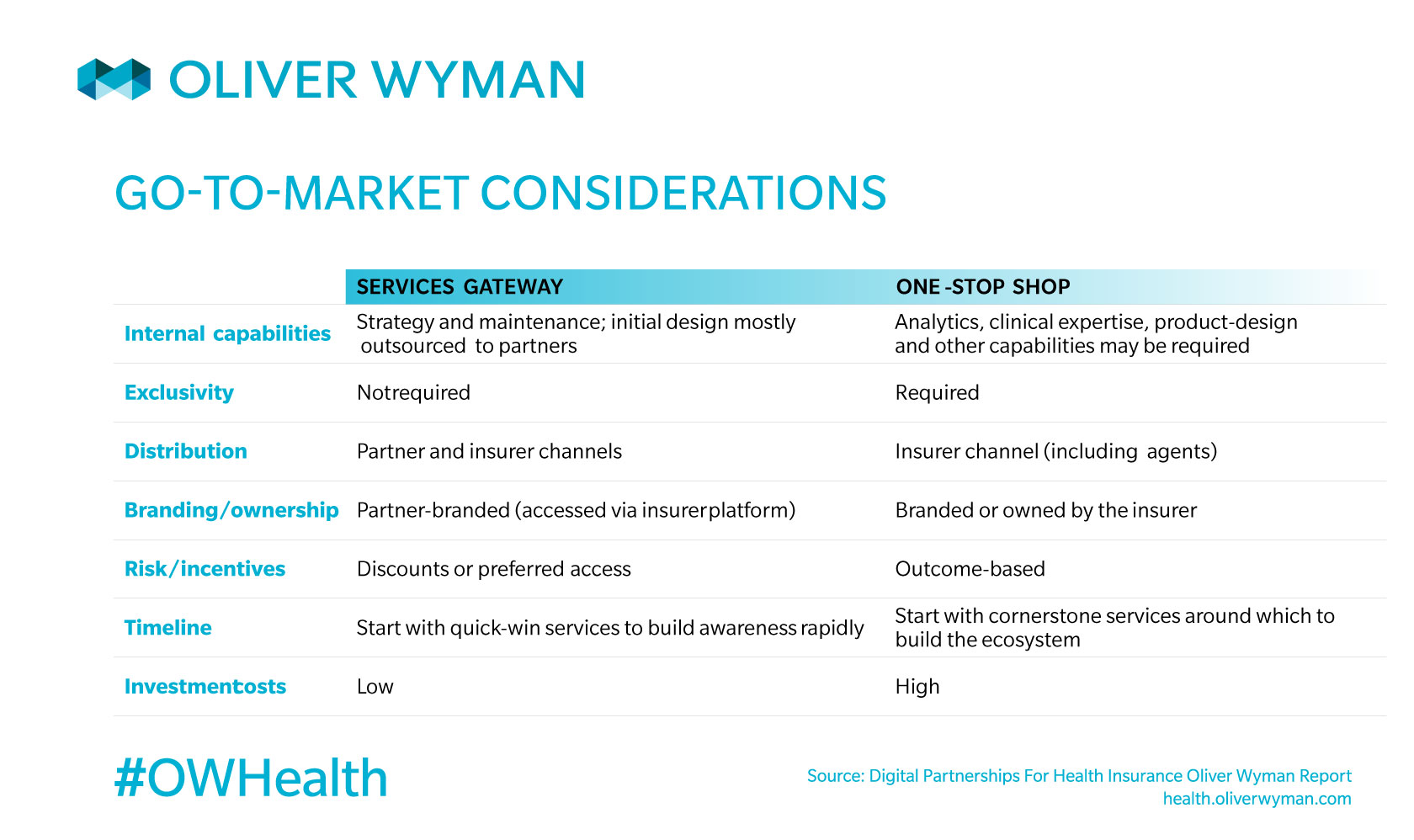

3. GO-TO-MARKET IMPLEMENTATION

Finally, after selecting partners, an insurer must consider what go-to-market approaches best fit both the specific partnerships and the model for the overall ecosystem:

CONCLUSION

Digitization and consumerization themes have already penetrated the healthcare industry in Asia, and many new insurer-digital health partnerships have emerged. While partly defensive, these collaborations also present new opportunities for value creation for both consumers and the insurers. However, Asia’s insurers will also need to temper their ambitions with an understanding of both risk and investment required in such a strategy.