As a result of China’s unprecedented commodity chemical capacity expansions in recent years, the futures of Europe’s biggest producers are now inextricably intertwined with the direction by the Chinese economy and the Chinese government's policy decisions over the next decade.

While the short-term outlook is weak for European producers — driven by high energy prices, strict regulation, significant oversupply of ethylene and other basic chemicals, and low utilisation rates — the mid‑term looks brighter.

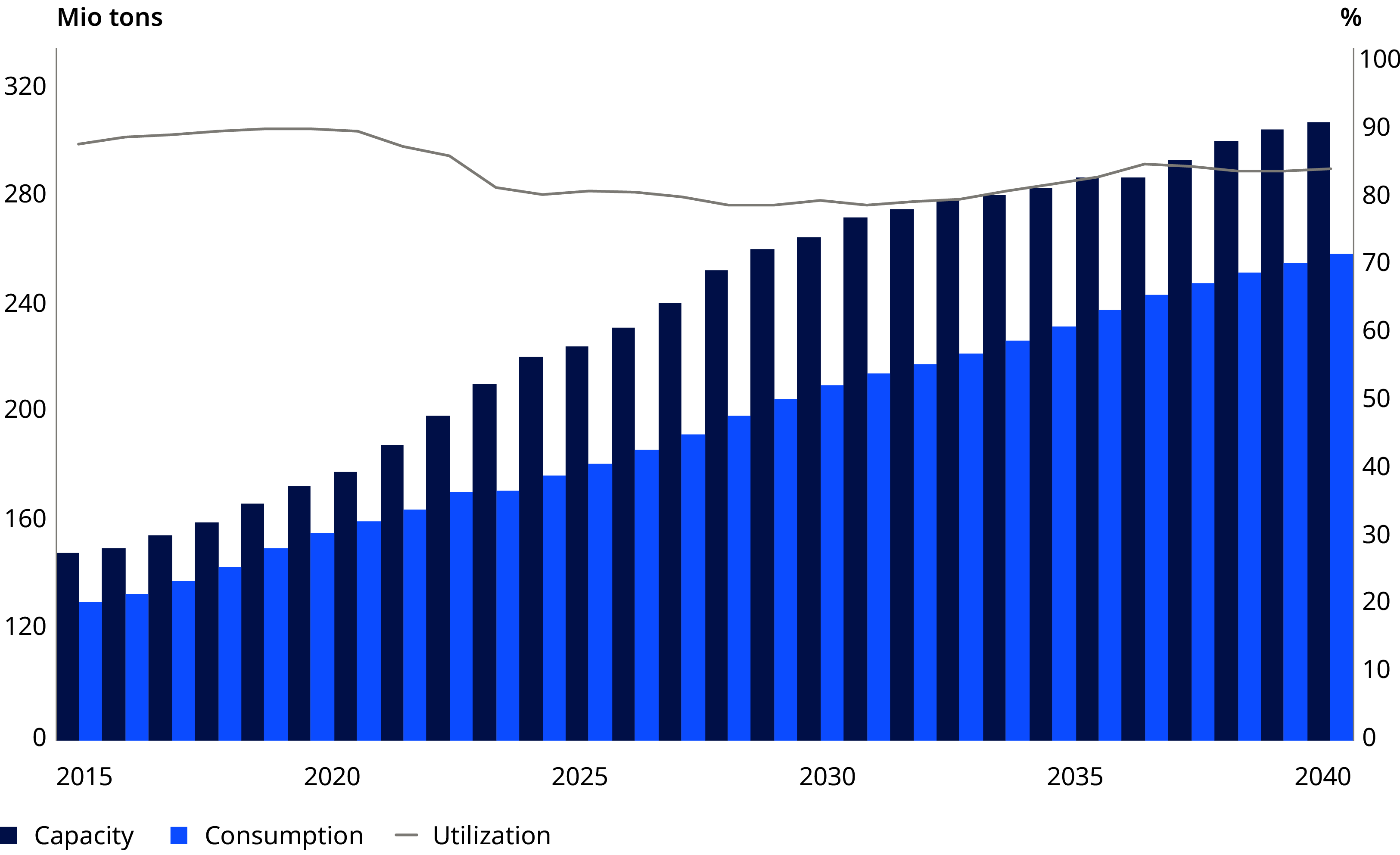

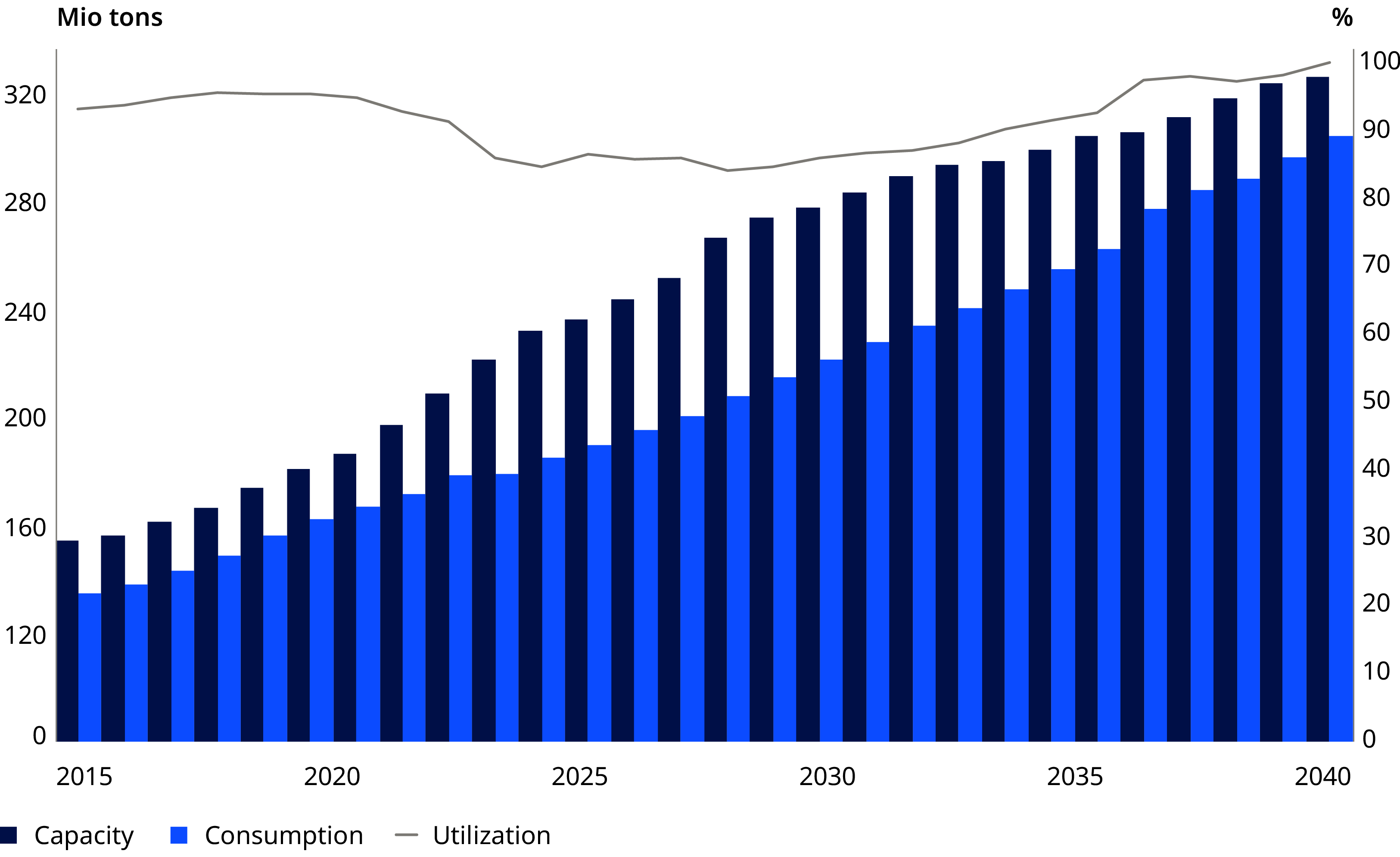

Take ethylene, the largest-volume commodity chemical, as an example. Our latest modeling for ethylene production projects that utilization rates could sustainably return to around 85% levels by 2035 — a level that would make it financially viable for more costly European production to compete. This turnaround assumes China’s stimulative economic policies get its industrial sectors growing faster and it stops adding net new chemicals capacity.

That’s why our model is more optimistic than the consensus forecast. We expect demand for ethylene in China to return, with growth rates potentially above 5% after 2030 because of Chinese policies and goals. If this were to happen Europe might even see investment in new ethylene capacity after 2035 when we expect utilization rates to remain over 85%.

But a European rebound will also depend on how aggressive industry and governments are about making the region’s capacity more cost competitive, our analysis shows. This will mean a re-examination of regulation and new policies to help bring down the cost of energy and carbon prices in the region.

How the Middle East conflict is changing the immediate outlook for commodity chemicals

That said, the fundamentals in the market are currently overshadowed by hostilities in the Middle East, shifting the immediate focus to the risk of feedstock supply disruptions — at least for the short run. The Strait of Hormuz, which is currently impassable for most vessels because of the conflict, represents a critical feedstock transportation route for Asian chemicals producers, accounting for roughly 60% of naphtha imports in 2025, as one example.

China has higher feedstock flexibility, compared with either Japan or South Korea, given China’s domestic supply of oil, its oil and gas trade with Russia, and alternative coal-to-olefin routes. However, many steam crackers rely on imported naphtha for ethylene production, with around 40% of naphtha coming from the Middle East. With widespread bombing in the region, several producers have had to cease operations as assets and infrastructure are damaged or destroyed in bombings.

If the crisis and blockade of the Strait continue, the likelihood of further reductions in run rates due to feedstock supply shortages will increase. The supply disruption is also pushing up market prices for key feedstock such as naphtha and natural gas. Even with the reopening of the Strait, these prices are likely to remain elevated for months because of the challenges repairing assets, rebalancing supply chain and logistic networks, and ultimately normalizing trade. Producers, suppliers, and consumers also face higher freight and insurance costs because of the elevated risks.

In the face of this crisis, producers may adjust strategies regarding feedstock supply, inventory, and production. As of March, there was no end date or easy resolution in sight for unblocking the Strait or an end to the bombing of the region’s oil and gas facilities.

How European producers lost their competitive edge amid China’s rapid expansion

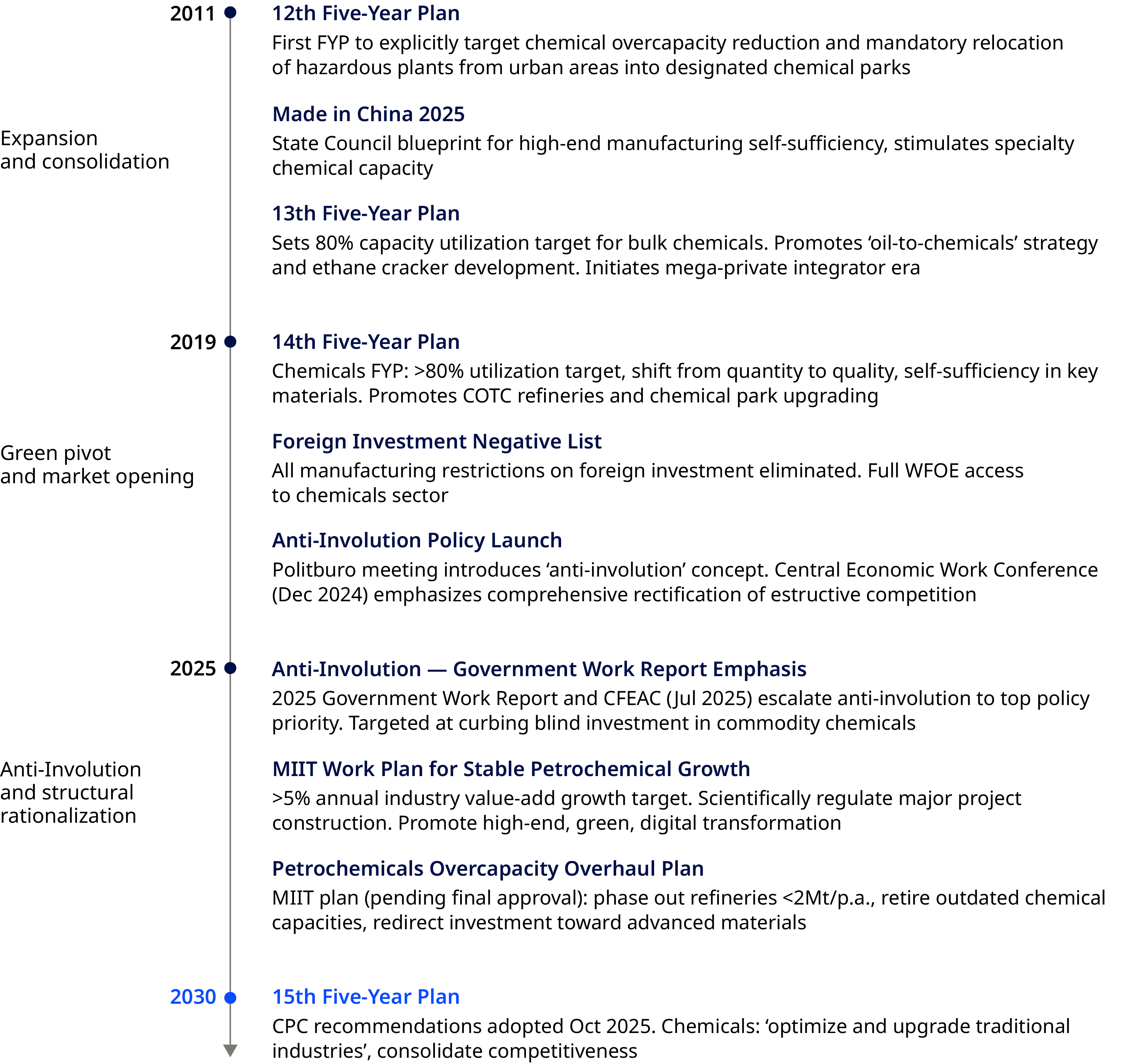

While the Middle East conflict is shaping the immediate outlook, the current downturn in commodity chemicals is a global phenomenon — structural, not cyclical. It reflects several major market realities converging simultaneously to create a stifling oversupply and particular problems for European producers. The number one disruptor of that marketplace has been China and its efforts in recent years to become not only self-sufficient in commodity chemicals but also a global leader — two goals it has accomplished.

Between 2019 and 2024, China installed more new ethylene and propylene capacity than the entire existing base of Europe, Japan, and South Korea combined. China now commands roughly 23% of global ethylene capacity — making it the world's largest producer — with further expansions planned for 2030 and beyond. Where Europe once led the world in ethylene production, it currently accounts for roughly 10% of global capacity.

Complicating the outlook is a second important trend — a major slowdown in demand, particularly within the Chinese market. Chinese demand for ethylene — the building block for more than 50% of all polyethylene as well as ethylene oxide, ethylene glycol, and polyethylene terephthalate (PET) — decelerated to about 2% per annum versus growth rates of around 9% per annum between 2010 and 2020. This reflects the weakening of traditional demand drivers in China, such as construction materials, which slowed when China’s property sector experienced prolonged softness.

Global weakness, market forecasts, and Chinese consolidation and dominance

Globally, demand also softened, growing at about 2.4% between 2020 and 2025. Not surprisingly, this slowdown, combined with oversupply of product, hurt pricing across chemicals and created prolonged low profitability throughout the value chain.

Despite the market’s bleakness, current market forecasts do not yet fully account for the potential impact of China's governmental "anti-involution " campaign, which aims to push older, unproductive assets out of the market. This could allow Chinese producers to expand without adding significant net new capacity.

In this regard, Chinese policy has been very deliberate in positioning the country as the leading global supplier of commodity chemicals, similar to its successful efforts to dominate solar panel manufacturing.

Chinese market archetypes and the impact of consolidation policies

Our analysis of four distinct player archetypes in the Chinese market shows the impact of Chinese consolidation policy and underscores Beijing’s determination to reshape the nation’s petrochemical demand landscape. The four archetypes are:

- National oil majors: pursuing selective expansion,shifting fuel higher-value chemicals and materials, and upgrading legacy assets. With between 40% and 45% of China’s ethylene capacity and cash costs per ton between $650 and $750, these giants prioritize domestic supply security and employment and are resilient to downcycles, as state balance sheets can absorb losses. But their capacity discipline is often diluted by provincial resistance to closures.

- Mega-private integrators: aggressively expanding and building world-scale crude-oil-to-chemicals capacity and integrated complexes.They enjoy the strongest cost position, with maximum integration and cash costs.

- Coal-to-olefins and methanal-to-olefins independents: are the weakest archetype, with negative margins. They are considered prime targets for governmental “antiinvolution” rationalization. Representing 10% to 15% of total capacity, many are operating at reduced rates or have already shuttered. They have the weakest cost position, with cash costs between $750 and $950 per ton.

- International producers: Investors that have committed over $25 billion toward the construction of capacity aimed at supplying high-performance downstream production. They operate modern coastal naphtha crackers with flexible feedstock, mid-range costs between $650 and $750 per ton, and about 8% to 10% of the country’s capacity. Their resilience to market fluctuations is relatively low as China returns must compete with alternative deployments in the US and Middle East.

Why Europe’s chemical sector is falling behind — and the fixes required

European producers face another significant market pressure because of persistent energy and feedstock cost disadvantages — with operating expenses two to five times higher than those of US and Middle Eastern competitors. Energy costs alone run four to five times higher than in competing regions and are expected to stay two to three times higher even in optimistic scenarios. This represents a structural cost disadvantage in commodity chemicals that makes the regional industry uncompetitive on the global stage.

As a result, legacy Western players have had to give up market leadership in several major markets to Chinese state-owned and private enterprises. In response, European chemicals makers are cutting production, particularly at high-cost, low-return assets. But the reductions are too small to meaningfully alter the global dynamic.

Path forward for European commodity chemicals

No doubt, Europe's chemical industry is battling a deep crisis, but the most pressing challenges require urgent reforms at home. Other major market realities, runaway energy and carbon prices, are undermining competitiveness for European producers, making investments in affordable, low-carbon energy and smarter regulation crucial to level the playing field.

European industry also needs robust safeguards against unfair competition, while simultaneously making the region more attractive for research and development and innovation. As the president of CEFIC (European Chemical Industry Council) recently noted, Europe's current playbook is not working — with site closures and job losses reaching concerning levels. The path forward requires political resolve, strategic investment, and a commitment to align climate ambition with economic reality.

The chemical industry has reinvented itself through disruptions before. But this time, the forces are converging from multiple directions simultaneously — overcapacity, demand deceleration, geopolitical fragmentation, and the energy transition. Leaders who understand the structural nature of this shift will be best positioned to act rather than wait for a cyclical recovery.