For the first time, global passenger revenues for the airline industry are expected to top $1 trillion in 2025. Demand reached a new high, with a record 5.2 billion people traveling by air, and revenue passenger kilometers (RPK) rose 9% above its pre-pandemic peak in 2019.

Those passengers, however, flew on increasingly aging aircraft as manufacturing capacity could not keep up with this robust demand. At the start of 2026, about 17,000 unfilled aircraft orders were on the books, a backlog that is expected to take more than 12 years to clear at current rates of production.

The gap between supply and demand leaves the industry unable to fully capture the benefits of soaring interest in air travel. The production lag is also jeopardizing sustainability targets as the industry misses out on the improved fuel efficiency of newer aircraft. In 2026, fuel efficiency will increase by 1% according to the International Air Transport Association (IATA) — an improvement over 2024 and 2025 but short of the annual 1.5% to 2% gains of prior years.

In our “Global Fleet and MRO Market Forecast 2026-2036” — Oliver Wyman’s 26th annual assessment of the 10-year-outlook for the commercial airline fleet and the maintenance repair and overhaul (MRO) market — we detail the record-setting year of 2025 and the status of the fleet in a time of global and industry turmoil.

Why the aviation industry can’t keep up with soaring demand

With record-setting demand, particularly in Asia and on transatlantic routes, the aviation industry’s global net profits reached $39.5 billion in 2025 — a 3.9% net profit margin, up from the 2.9% margin in 2024. An assist from a 16% decline in jet fuel prices helped it overcome rising costs to reach profitability in all regions other than North America, where growth was flat.

At the same time, supply chain, labor, and structural constraints continued to limit manufacturing output. By the end of 2025, global aircraft production was 24% below 2019 levels. With deliveries stalling, airlines are dependent on an increasingly aging fleet. Aircraft are flying more hours, and both utilization and passenger load factors reached new highs in 2025.

The average age of the global fleet approached thirteen years in 2025, roughly a year and a half older than in 2024. Average flight hours per aircraft rose 2% year-over-year, and utilization is projected to continue to grow until deliveries catch up later in our forecast period.

In North America, the world’s largest market, the US government shutdown, disruptions in staffing of air traffic controllers, weather and technology-related delays, and labor unrest among flight attendants, pilots, and other workers created additional headwinds.

While global economic growth is expected at 3.2% in 2025 and 3.1% in 2026, ongoing geopolitical and supply chain tensions add uncertainty to the forecast. RPK growth is expected to track more closely to global GDP than in recent decades and is projected to grow 4.3% in 2026.

How supply chain tensions are throttling aviation industry expansion

A thriving aviation industry depends on a robust supply chain, but tensions through the system have slowed the industry’s post-pandemic recovery. Raw material shortages, geopolitical volatility, ramp-up challenges, and growing demand for military and defense aircraft led to delays in production and deliveries of commercial planes.The fragile supply chain was not the only disruptor last year. Weather and technology-related delays, labor unrest in several markets, the US government shutdown and shortages of air traffic controllers impacted schedules and costs.

Another factor affecting fleet expansion was a wave of retirements of skilled workers. As the last of the Baby Boom generation leaves the workforce, taking their expertise with them, the industry is struggling to attract and retain younger generations of well-trained workers. About 41% of certified mechanics in the US are over 60 years old, and about 45,000 mechanics will retire in the next decade. Air traffic staffing is also a concern, with the pace of hiring unable to close the retirement gap. In 2025, both North America and Europe experienced flight delays and cancellations because of air controller shortages.

Retirements are affecting management as well, and the leadership gap is an emerging concern. A slowdown in hiring in the 2000s and 2010s has resulted in fewer middle managers who have the expertise and industry knowledge to take over from the older generation.

Production lags are forcing the aviation industry to rely on aging fleets

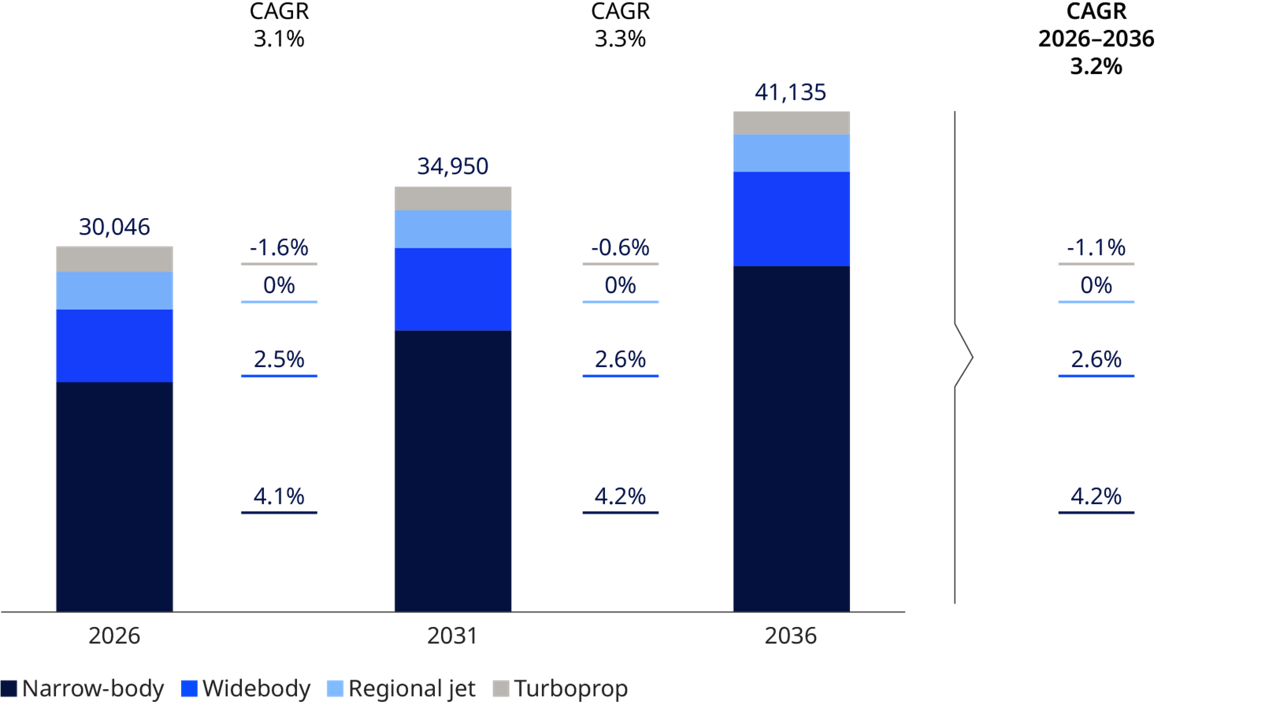

As of early 2026, the global commercial in-service aircraft fleet (excluding Russia) totaled about 30,000 aircraft. By the end of our forecast period, we expect the fleet to reach roughly 41,000 aircraft – a compound annual growth rate (CAGR) of 3.2%. That growth lags our pre-pandemic forecast by six years.

Supply chain issues will limit annual aircraft production worldwide until at least 2030, representing more than 6,000 new aircraft that would have been produced otherwise. In the second half of the forecast period, a faster pace of deliveries will bring retirement ages back to their historical norms.

Both Airbus and Boeing, the industry’s leading manufacturers, have been unable to meet their ambitious production targets. Airbus holds 49% of the order book, with Boeing at 38%. Narrowbody aircraft orders dominate new orders, reflecting the desire to increase efficiency. Airbus aims to reach a monthly rate of 75 A320 aircraft by 2027, but that seems unlikely as it produced 54 per month at the end of 2025. Boeing faces a similar shortfall: it targeted 57 monthly 737 units in 2026, but at the end of 2025 the FAA approved a production rate increase to 42 a month.

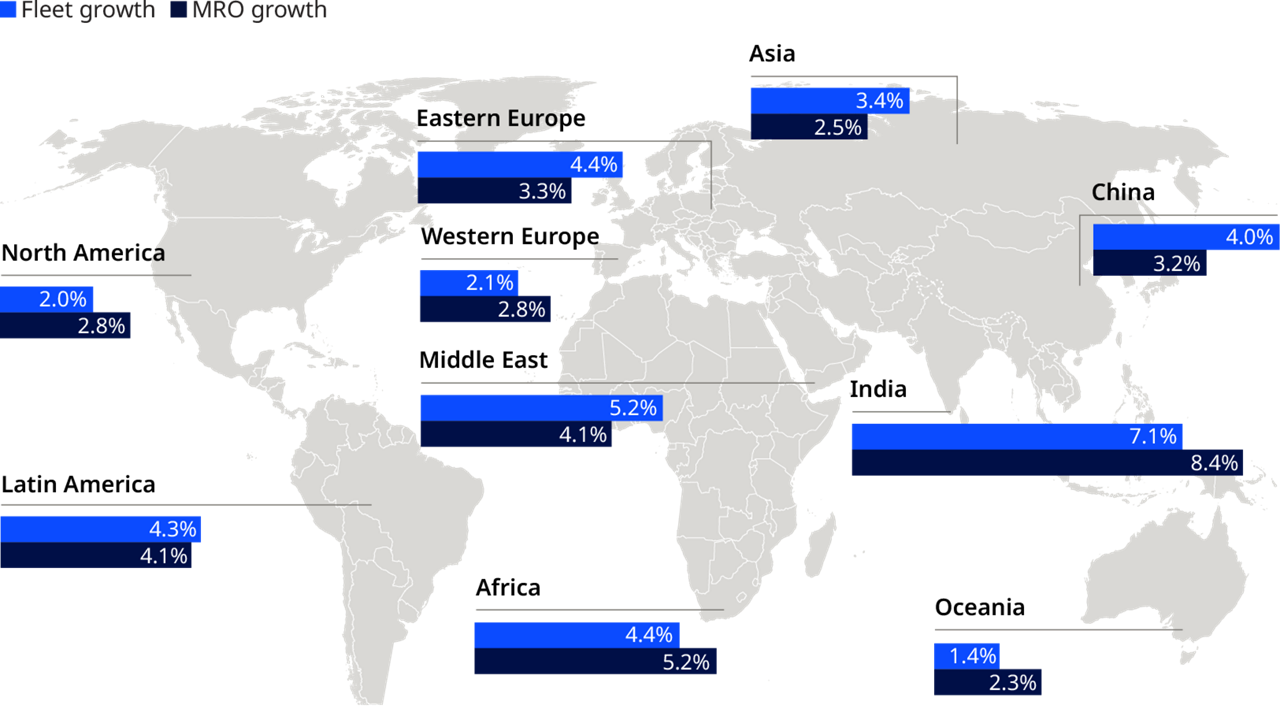

Looking across the globe, China will add the most aircraft over the next decade. India will experience the highest growth rate, with a 7.1% CAGR, followed by the Middle East at 5%.

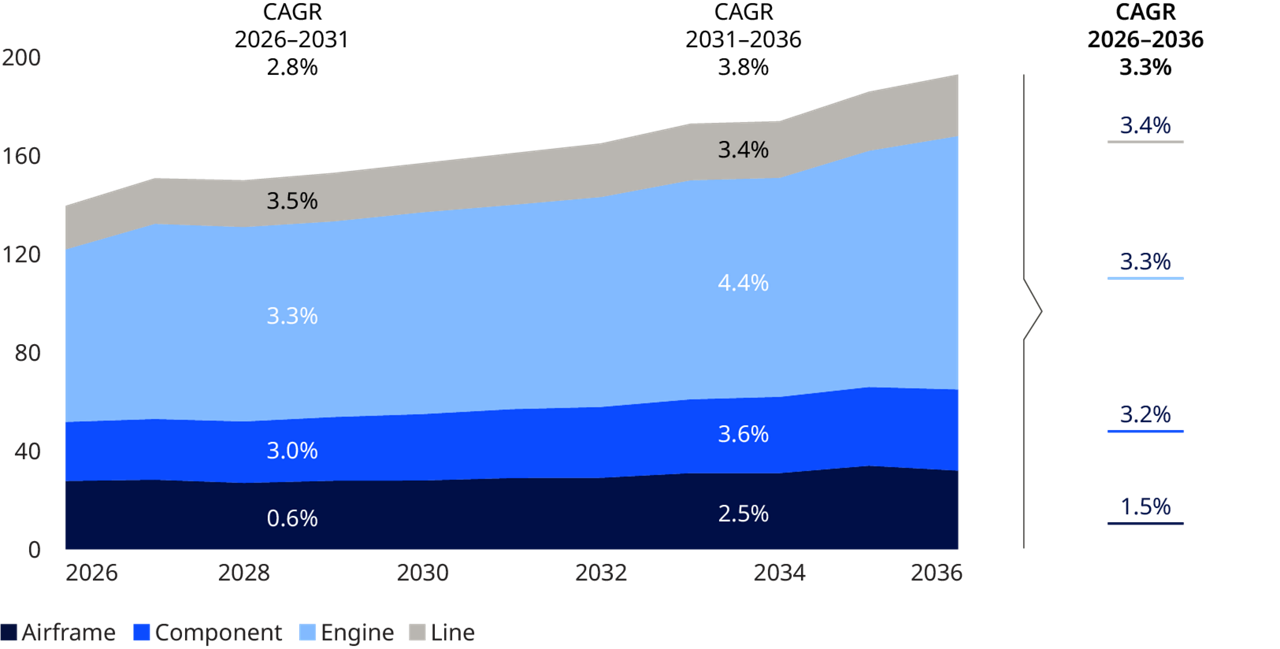

Aging fleets are rising MRO revenues,costs, and delays

An aging fleet is one that requires more maintenance and more replacement parts. That demand has pumped up prices for both parts and labor, extending the supercycle that began following the pandemic in the MRO segment of the market.

Global MRO demand reached $136 billion in 2025, up 8% from $126 billion in 2024. By the end of the decade, spending is expected to approach $193 billion — nearly double the 2019 level. In regions with older fleets — North America, Western Europe, and Africa — maintenance spend will outpace fleet growth.

Not all the news is positive for the MRO market. Technical challenges with engines and broader supply chain constraints, including shortages of raw materials such as composites and titanium, are tying up schedules. Delayed maintenance from the pandemic and the 737 grounding between 2019 and 2023 has created a “bow wave” effect, contributing to capacity bottlenecks, longer turnaround times, and fluctuating pricing. Large component systems have been hit hardest, especially engines, which represent the biggest segment of the MRO market.

Efficiency and renewed investment will drive a stronger airline future

To counter these ongoing headwinds, airlines are strategically managing their fleets and searching for operational efficiency. With cost containment essential, we expect more partnerships and acquisitions between operators and maintenance providers.

Consumers will also see higher ticket prices resulting from higher overall costs through the system as well as supply and demand trends. Without question, meaningful investment — from upgrading technology to hiring a replacement workforce to strategic capital investments in parts — is required to ensure the aviation industry can capture growth while manufacturing efficient aircraft.