Worsening climate conditions have begun to elicit a response from governments and corporates, increasing the demand for alternative clean fuels. Biofuels produced today, which entail the efficient use of biomass and waste products, can reduce greenhouse gas (GHG) emissions by up to 90%. As a drop-in fuel, biofuels are currently the main alternative fuel being relied upon by hard-to-abate sectors.

In our previous biofuels publication, we explained the development of tiered markets – with Western regulatory markets leading sector growth and Asia gradually following a similar trajectory. We also discussed the importance of collaboration across players in the value chain, from energy majors to policymakers and feed producers. These forces are shaping a nascent sector where price discovery, supply chain, and demand growth are still underway.

Uncertainties like these dominate many of the conversations we have with industry leaders and policymakers. The aim of this article is to address a key question facing the sector: How do biofuel producers strategically position themselves in an environment where the impetus to act is pressing, but the challenges are many?

The crucial role of feedstock in biofuel expansion

Biofuels demand is expected to maintain its momentum as aggressive clean energy policies are implemented globally. Industry estimates suggest 5% per annum growth up through 2050. Sustainable aviation fuel (SAF) has been and continues to be a major growth driver, supported by policies enabling net-zero targets in aviation. For example, the EU announced the ReFuel EU policy, where SAF blending targets are expected to grow from 2% in 2025 to 70% in 2050 . Similarly, policies in the United States are directed at stimulating supply via tax credits, enabling SAF prices to be more competitive vis-à-vis petroleum-based jet fuel.

Traditionally, first generation feeds used for biodiesel production are derived from edible crops such as wheat and palm. Concerns around “Food versus Fuel” and carbon intensity have shifted focus towards more sustainable feedstock for new generation biofuel production such as SAF. Most SAF today is produced via the Hydroprocessed Esters and Fatty Acids (HEFA) process, and regulated markets require biofuels to be produced with advanced feedstocks.

Advanced feedstocks are those that do not compete directly with land use for food crops and typically have low carbon intensity. These are mostly derived from lignocellulosic feed such as agricultural, forestry residues as well as industrial or municipal wastes. Examples include tallow, used cooking oil (UCO), palm oil mill effluent (POME), and other animal fats wastes. To meet growing demand, biofuel producers must secure a supply of low-cost and low-carbon intensity feedstock.

Regulations have been the main catalyst for shifts in feedstock acceptance: For example, Europe’s RED II (Renewable Energy Directive) was introduced in 2018 and provides strict guidance on acceptable feedstocks — excluding crude palm oil and its byproducts. Consequently, such restrictions act as a limiting factor for feedstock supply.

Even as feed supply continues to grow in relatively untapped markets like Asia, it may not be sufficient to supply the about 24 million tonnes SAF production expected by 2030, as estimated by the International Air Transport Association (IATA). This is especially so if local demand in Asian market ramps up faster than local collection. China has set the goal to be carbon neutral by 2060, promoting biofuels production from non-food biomass. As the chasm between SAF production capacity and availability of feed widens, the landgrab for sustainable feed intensifies.

Amidst limited availability, feed prices have been very volatile. The preference for UCO over other feed types, given its lower carbon intensity, has driven up prices significantly between 2019 and 2022. Price of UCO almost doubled in this period but have quickly returned to 2019 levels this year. Feed availability and procurement costs are now the main considerations for HEFA production approvals and have a direct impact on the pace of substitution of conventional jet with SAF. Therefore, a key priority for producers is to ensure the security of a stable and traceable supply of sustainable feed.

Asia is the rising star in global biofuel feedstock supply

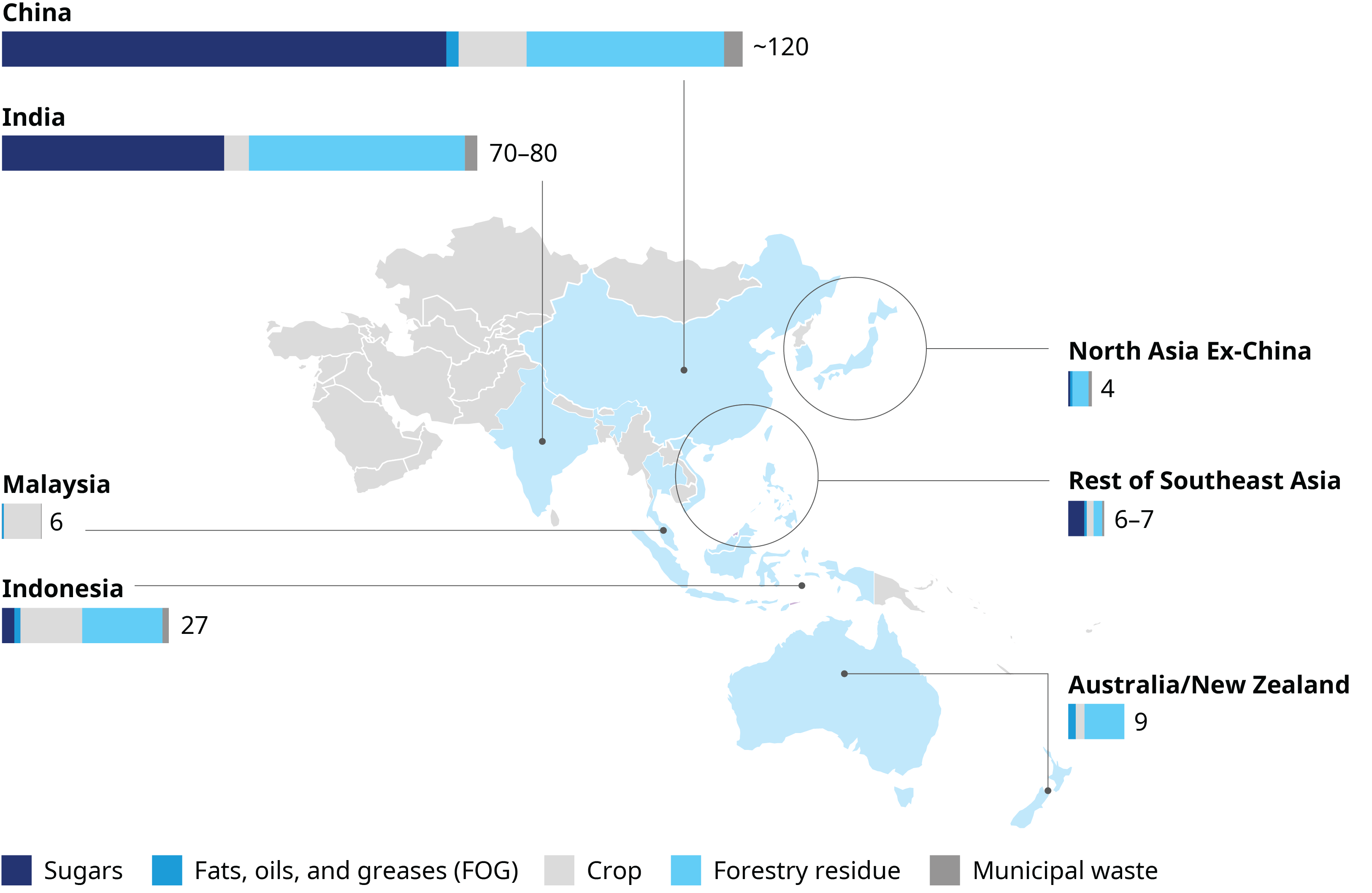

Focus on feedstock has now shifted to Asia, given that waste-based feed collection has largely plateaued in Western markets. Asia’s population size and established agricultural sectors position the region as a prime feedstock hub.

Globally, there are around 800 million metric tons of potential biofuel feedstock supply, ranging from agriculture and forestry wastes to sugars and oils. These include volumes either currently treated as wastes or used for other purposes such as animal feed. About 40% of this global volume can be derived from Asia. Within the fats, oils, and greases category, Asia contributes more than half of the feedstock. Indonesia and Malaysia account for more than 95% of global palm oil production, and most sustainable palm-based wastes.

We estimate the annual global production of UCO to be between 13 million and 15 million metric tons, with UCO collection in developed Western markets plateauing. Europe has been importing two-thirds of its UCO supply to feed its local biorefineries, with China as its main source. Currently, three million metric tons of UCO are collected within China annually, and industry estimates suggest that this volume potential could be doubled going forward.

Asia plays a key role as an alternate hub for feed with low collection rates in markets like China and Indonesia. This gives existing and new SAF production plants such as Neste in Singapore, or the Qantas-Airbus JV in Australia access to a proximal, cost advantaged supply of feed.

Despite Asia’s potential in offering new feedstock sources, scaling supply in nascent markets comes with its challenges:

Less developed feedstock collection methods

Methods for feedstock collection of UCO and agri wastes are less developed in these markets and collection rates are still below peak. Nascency of these sectors means that collection infrastructure, standards, and supply chain are still underdeveloped. Players in these segments are relatively new and many are still navigating through challenges around local operations and regulatory volatilities.

opaqueness of local biofuel production operations

Traceability of feedstock sources have become a challenge for local operations, such as UCO collection in Indonesia. For example, adulteration of feedstock, such as mixing of virgin oil into UCO, is prevalent in certain regions. This, coupled with lack of regulatory oversight, has resulted in several scandals around local feedstock aggregators. This puts further pressure on the acquisition process and cost of feedstocks, amid a tightening market.

lack of strong local presence for global biofuel giants

Supply chain capabilities also play a critical role. Aggregating UCO from factories across countries like Indonesia and Malaysia, as well as palm-based wastes from mills or refineries around Kalimantan and Sumatra, requires scale and an effective supply chain to aggregate and pre-treat collected feedstock. With a sizable portion of volume collected from small, independent sources or collectors, a strong local presence is required to maintain a direct relationship with feedstock sources. For most international biofuels producers, local presence in these markets is limited, leading to heavy reliance on local partners.

Strategic partnerships power biofuel sector evolution

Given the difficulties in accessing feedstock supply from Asia, we are starting to see new types of strategic relationships develop between biofuel producers and feedstock suppliers, which are reshaping how value is created in this sector. For example, Bangchak and Thanachok Oil Light, a local UCO aggregator in Thailand, is partnering to build a SAF plant in Thailand. Similarly, BP has plans to purchase NuSeed Carinata Oil for feedstock processing and trading.

Beyond this, biofuels players are moving vertically across the value chain to capture higher value in biofuel production and to acquire strategic control of feedstock supply. On the back of this move, major integrated agribusinesses such as Wilmar, Cargill, and Bunge also are actively diversifying into feedstock aggregation and processing.

Implications for biofuel producers

Different pathways of demand developments and varying feedstock regulatory acceptance across markets are further reinforcing the tiering of the biofuel sector. Biofuel demand from regulated markets like Europe and US are faced with stricter feed requirements, while markets in Asia are less stringent in terms of biofuel blend mandates or feed requirements, and demand is largely voluntary.

Therefore, a number of biofuel producers are focused on Europe and US where there is a firm and growing demand driven by mandates. However, sustaining a market participation in the biofuel space is a global play – demand across markets is evolving and producers have to respond in a timely manner to new pockets of demand. In so doing, biofuel players need to consider their realities, such as access to quality feed or processing technology, and devise a careful expansion across geographies and scale up of operations. For example, biofuel plants set up in Asia may offer close proximity to high value feeds but may require players to serve regulated markets in the shorter term until demand in the region picks up.

Exploring horizons for alternate biofuel production pathways

Given that the availability of feedstock will be a limiting factor in the growth of HEFA production, biofuels producers will need to consider alternative production pathways as demand for SAF and other biofuels continue to grow.

Other viable but less prevalent production pathways at present include AtJ (alcohol-to-jet), where alcohol from sugar or starch (such as corn, sugarcane, and switchgrass) is converted into drop-in fuel. Currently, AtJ is perceived as less cost competitive than HEFA due to the higher cost of alcohol production (via fermentation). Despite having the potential to reduce up to 95% of carbon emissions, the prohibitive cost of AtJ production limits the extent of commercialization.

Existing and new players are betting on this technology, however. As an example, LanzaJet’s unique AtJ technology has the potential to scale up in the longer term with its flagship facility – Freedom Pines Fuels – producing around 30,000 metric tons of SAF per annum from ethanol derived from sugarcane.

Another alternative technology is the Gasification Fisher-Tropsch (FT) process. This first converts biomass to syngas via gasification. The syngas is then converted into liquid transportation fuels through the FT process. Newer pathways are also being explored as well for synthetic fuels, which also can be produced by the FT process, by combining a clean CO2 stream with green hydrogen, or alternatively, from methanol into synthetic fuels. Thus far synthetic fuels production has been challenging, however, given the combination of high capex requirements and high raw materials prices.

Setting strategic priorities for the biofuel industry

Despite uncertainties around feedstock and technological pathways, there are several strategic priorities that stakeholders need to address to make progress on the path to net zero.

For producers, an effective feedstock sourcing strategy at the portfolio level is crucial, so as to provide flexibility in production output to meet evolving biofuel market demands. With limited feedstock availability for HEFA production, players will need to place early bets on alternative technological pathways.

For buyers, strategically sourcing biofuels is critical amid the changing regulatory environment. In addition to ensuring a long-term reliable supply, buyers need to ensure that decarbonization is driven by cost-effective initiatives, which has been a key challenge in scaling up adoption. But this is quickly changing across two key fronts: First, players are now enhancing internal procurement capabilities to manage SAF costs, such as via hedging. Second, they are better managing the pass-through cost of SAF to end customers. For example, book and claim systems are being piloted to manage and share with end customers the supply chain costs of procuring SAF.

Finally, for policy makers, effective regulations need to be in place to ensure alternative fuel needs are met for decarbonization. In this respect, infrastructure development and adequate incentives are critical to attracting and building a scalable ecosystem of biofuel producers and feedstock suppliers.