Our recent research on potential 2030 scenarios for North American Class I railroads shows that focusing on growth — backed by a cost efficient and reliable operation — is the only strategy likely to lead to long-term value creation.

The railroads are a critical part of the North American economy and supply chain infrastructure. A growing rail industry would be aligned with diverse stakeholder goals and provide the most credible path forward to improve returns. This will require at a minimum maintaining market share but more preferably shifting mode-flexible freight from truck to rail. Without a pivot to growth, the railroads face volume and profitability stagnation and further market share erosion.

Railroad's future — fold, hold, or all in

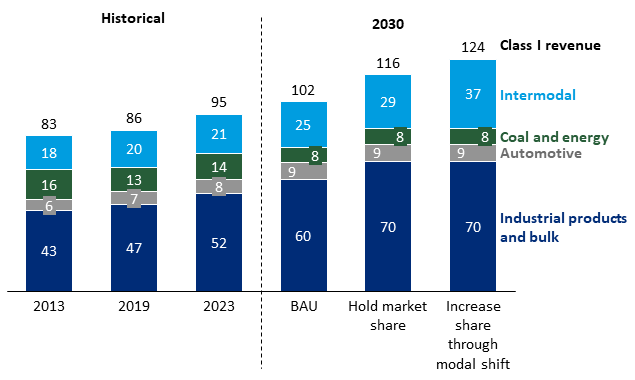

We believe that railroads are at a decision point in terms of their future financial outlook and must soon choose one of three paths: Business As Usual (BAU) — leading to managed decline, hold market share, or take immediate action to grow. Our projection of estimated 2030 revenues for each scenario are shown in Exhibit 1.

Note: Includes BSNF, CN, CP, CSX, KCS, NS, and UP

In a BAU scenario, the railroads continue to do what many are doing now: cut costs, attempt to raise prices, and fail to materially improve service or the customer experience. The result will be continued market share loss to trucks; price-driven revenue growth will barely offset declining coal volumes. Ultimately, the railroads would become more like utilities: maximizing financial returns while shrinking back to regulated, rail-centric commodities and the network required to support these.

The other options require varying degrees of a growth strategy focus. To simply hold market share vis-à-vis trucks, the railroads will need to improve service (including transit time and reliability and the customer experience in the areas of intermodal and industrial products. But to actually increase market share and shift mode-flexible freight back to rail, they will need to go a step beyond: achieving a level of service and customer experience that is much more competitive with truck on the dimensions of reliability and ease of doing business. They will also need to expand by offering new lanes and product enhancements.

Last gasp for margin focus

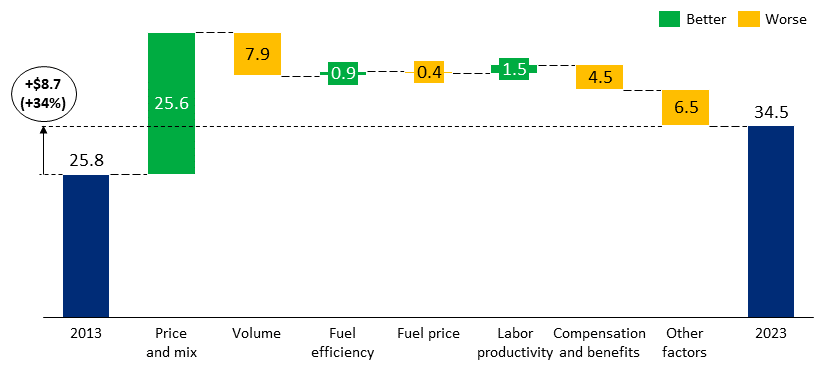

With some exceptions, railroads, their owners, and analysts have focused on maximizing margins, not earnings, for the past 10 years. Railroads have consistently improved their operating ratio (by 7.5 percentage points from 2013 to 2022) — while losing volume (9.5% decline in revenue ton-miles). Lost volume has largely been coal (which will decline 35-40% by 2040), with flat volumes in intermodal and industrial products. This strategy has paid off – but only up to a point.

A deeper look at operating ratio (OR) shows that price and mix shifts have been the most important levers in financial improvements since 2013. Much has been attributed to enhanced operational efficiency from the adoption of precision scheduled railroading (PSR), but the data shows that while there have been some material productivity improvements, operating gains have been more than offset by operating cost increases.

Note: No adjustment for extraordinary items

It is clear that railroad commercial teams have had a large role in OR improvement, managing impressive market price and beneficial mix shifts increases on a flat to declining base of business. While trucking prices also increased over the same period, they were far below the 30% achieved by the railroads. Spiking truck prices on the back of COVID have since closed some of the gap between rail and truck, but the railroads have not sufficiently sustained service improvements to recover share.

The growth imperative

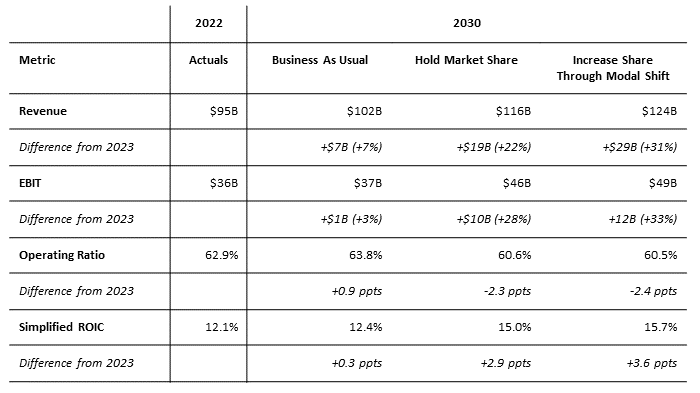

We believe the BAU strategy has run its course. As shown in Exhibit 3, continuing on this path will lead to $37 billion EBIT in 2030 — nearly the same as in 2023 — and an OR of 63.8%, about 0.9 percentage points above 2023. This is because fixed costs will have to be spread across less freight. Management may believe they can improve on this, but attempting to increase prices further risks market share loss and regulatory action. To sustain today’s OR without coal will require deep cost cutting above and beyond prior efficiency improvements.

Looking at key financial metrics (EBIT, operating ratio, ROIC), a strategy that holds or increases market share will outperform a strategy of continued cost cutting and low to no growth. Growing industries also generally attract higher earnings multiples. And only growth will maximize shareholder returns: The railroads could leave some $120 billion to $180 billion in market capitalization on the table without growth.

Either holding market share or shifting more flexible freight back to rail would earn the railroads an extra $9 billion to $13 billion in EBIT, increasing market capitalization by 25-34% at the current multiple. Either scenario also would improve OR, by 2.3 to 2.4 percentage points compared to today, due to more revenue against a largely fixed-cost base.

Note: Simplified ROIC calculation uses [EBIT] / [Property, Plant and Equipment Book Value] to approximate ROIC (which is a non-GAAP measure with methodologies that vary by company

What it will take to achieve growth for rail

To grow volumes, railroads will need to deliver sustained service quality and a customer experience that is consistent and more competitive with truck. Today, shippers universally prefer truck because of its superior flexibility, reliability, and customer-centricity, and are willing to pay more for truck as a result. Shippers we have spoken with and surveyed have repeatedly told us that they want to do more with rail because of its advantages, but that the product and experience simply are not meeting their supply chain needs.

Key to growth for rail will be specific strategies focused around their top revenue earners: industrial products and intermodal.

Industrial products are attractive to rail because these commodities are generally more rail-centric and higher margin than intermodal. By improving their service offering, railroads can ensure that new investment in manufacturing — supercharged by the Inflation Reduction Act and government incentives — is rail served. Railroads also must find new ways to access shippers that do not have rail access. Holding share in industrial products alone would add approximately $10 billion to industry revenue by 2030.

Intermodal offers the potential for higher growth through modal shift. Our analysis shows that there is sufficient flexible freight for the railroads to achieve revenue growth in line with GDP (of 3.9%). This will require expanding beyond long-haul, however, since intermodal already has a 65% market share for lanes over 1,500 miles (served by a single railroad). There is more headroom for share shift in lanes under 750 miles, where intermodal accounts for just 13% of volume and the market is larger: 23 million truckloads in high-volume lanes alone.

Achieving $37 billion in intermodal revenue by 2030 would require railroads to win back 5-6 million of these truckloads. To do this would mean holding share on the existing network, capturing truck share from new transborder lanes to Mexico, and launching more interline and short-haul products.

Continuing to cut costs and raise prices is not a long game, extracting value and diminishing the reach of a rail network that served this continent for more than a century. Focusing on service and growth instead would give shippers the business case they need to switch to rail. And by doing so, railroads would build a foundation that rewards long-term shareholders, enables investment in new technology, and helps ensure a North American freight transportation future that is safer, greener, lower cost, and more energy efficient for everyone.